Chicago Is My Kind of Town To Beat Up On: 2018 edition

It was a sparse year -- I was busy with other stuff

I need to speed this up, as the Democratic Convention is just days away…. but I also found that I had very few Chicago posts in 2018 for a few reasons.

Namely, Stu had been going through infusion chemo, but also I was focusing on “Memory Monday” (looking back at 1918, to look at news from The Great War, and seeing the Spanish Flu pandemic hit… later in the year) and then the big news for 2018 were all the high-tax areas trying to figure out “clever” ways to avoid the SALT cap.

I focused more on Illinois than Chicago, as well as Kentucky pensions (there were doings there), and all sorts of divestment pushes in the funds.

Prior editions:

2014: Chicago Is My Kind of Town To Beat Up On: Previews for the DNC

2015: Chicago Is My Kind of Town To Beat Up On: 2015 edition

2016: Chicago Is My Kind of Town To Beat Up On: 2016 edition

2017: Chicago Is My Kind of Town To Beat Up On: 2017 edition

Taxes in or near Chicago - 2018

Recall that the SALT cap of $10,000 went into effect in tax year 2018. So a variety of high-tax locales were looking at ways to avoid this burden….

….but Illinois was looking at making it worse:

2 Feb 2018: Friday Foolery: Dumb Taxes in General

ANOTHER DUMBASS ILLINOIS IDEA: LET’S TAX THE RICH WHO HAVEN’T YET LEFT

It’s not trying to tax meat or porn, but this is an extremely bad idea…for Illinois. It’s a great idea for Connecticut or New York.

It’s Baaaaack: The Illinois ‘Privilege Tax’ Bill! – Wirepoints Original

Undeterred by national ridicule heaped on Illinois last year, statehouse Democrats are pushing again for passage of the “privilege tax” on investment managers.

HB 4293 would impose a 20% tax, in addition to all other taxes, on fees that are based on capital gains. Hedge funds, private equity and venture capital would all be hit — for as long as it took them to leave, that is.

It would push all those firms out immediately and decimate the financial and tech communities, which are among the few sectors thriving in Illinois. Just by seriously considering the bill Illinois is sending a plain message to the financial community: Leave. Expect this topic to earn national scorn once again.

Connecticut would be very happy for a new bevy of rich people to move in. It’s lost a lot of its old bevies.

New York would also be pleased to take Illinois refugees.

I have no idea why money people like to be in/near Chicago. I find it an appalling town (yes, I’m a New York bigot.) But some of the selling points, as I understand it, is that Chicago is cheaper than NYC. And… hmmm. Some people like their sports teams better?

More seriously, lots of the people have family in the area, and would like to be near them. It’s one of the reasons I stay on the east coast (ok, not really. I stay on the East Coast because I’m a natural East Coaster. Hell, when I was living in Manhattan, I lived on the east side. And then I moved to Queens. And now I’m in the northeast corner of Westchester. I’m all about east. I don’t get those weirdos who go west.)

There are various key markets in commodities and other things located in Chicago but, and here’s the thing: those markets can be moved. They don’t need to be in Chicago.

(Nor does much of anything need to be in New York or Connecticut.)

I find it amusing that Daniel Biss is one of the sponsors of the legislation, as Biss continues to show that just because one has a fancy math degree doesn’t mean one is smart. Sometimes, it’s just a case of him having different values than me, but in this case, he’s just a dumbass.

But hey, starve the beast by running away the rich people that feed it. Fine by me.

I will note that Ken Griffin and his fund Citadel ended up leaving Chicago and Illinois in 2022. They did not go to New York or Connecticut, to be sure.

17 April 2018: Taxing Tuesday: Trying to Escape Property Taxes, Follow-the-Leader, More Married Couple TCJA Scenarios

You can check in any time you like…

America’s new great migration in search of lower property taxes

Rich Harty, co-owner of Chicago-based Harty Realty Group, has an unusual business model. As an exclusive buyer’s agent, Harty has spent the past few years leading house hunters farther afield than many expected when they started to search in his metro area.

As Harty, a lifelong Chicagoan, puts it, “I’m trying to convince them, let me show you what Wisconsin has to offer.”

Harty’s clients range from first-time buyers with sticker shock to people who’ve lived in and around Chicago all their lives. Each has a different story, but they share a common theme: many believe that Chicago-area property taxes are too high, and relief is just an hour away over the state line.

As a new report out Thursday demonstrates, Harty isn’t the only one realizing how big of an impact property taxes make on home-buying decisions.

Now, I didn’t have sticker shock with respect to my house or my taxes. I knew what I was getting into. I knew what I left back in North Carolina, too.

It was amusing when some of my New York City acquaintances relocated to North Carolina and were amazed how much house they could buy. I wasn’t amazed. Also, I told them, don’t expect some of the governmental services you get up here in Yankeeland (this is the case, for example, with my autistic son — we’re getting all sorts of education support for him through the school. I have friends with similarly developmentally disabled children, back in the south, and they are struggling. Even the ones who have money have trouble finding qualified help. Look, these sorts of services are expensive. I told them what we had up here… and you will be paying for it.)

There’s a nice interactive graphic at the link. They split it up by Trump or Clinton counties, but that’s misleading — California property taxes may be low (Prop. 13 result), but they aren’t a low tax state overall. You see high property taxes in Texas… but they don’t have a state income tax. It’s a trade-off.

Here’s a takeaway:

Cook County, where Chicago is located, had the biggest number of people leaving, but given a bigger starting population, those 45,360 leavers only made up 0.9% of the total.

Blomquist’s analysis of Census data showed that among all counties that had at least a 1% population increase, the average tax bill was $2,706, while in all counties with a least a 1% decline in population, the average was $3,900.

So. Can’t impose property taxes on the people not there.

The change, of course, came from the SALT cap in the 2017 tax bill. At least when you could deduct those property taxes from your income in your federal income tax filing, it took out some of the sting.

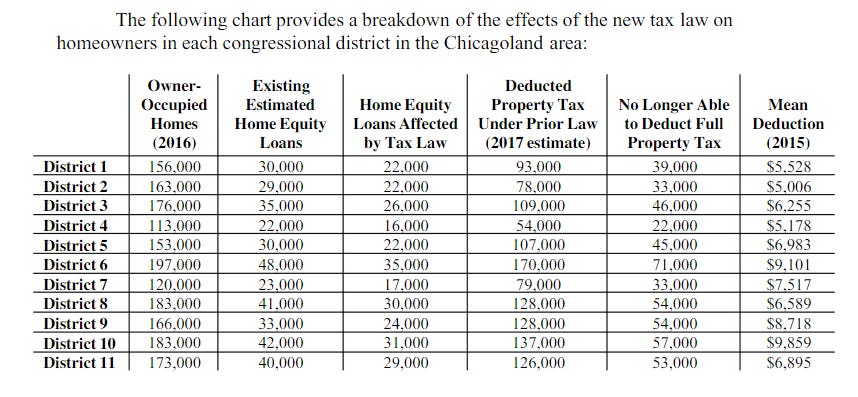

30 Oct 2018: Taxing Tuesday: Pity the Poor High-Income Highly-Taxed Chicagoans

A “study” (which turns out to be 4 pages of actual content, less than half of a 9-page document) on who gets to fully deduct property taxes has been put out for the benefit of Democratic politicians in the Chicago area. It turns out, some fairly rich people with high property tax bills (and probably high state income tax bills) are going to hit the SALT cap.

Which they already knew.

But hey, here’s a quantification!

Can you tell which of the 11 districts had a Republican representative at the time?

That Republican did lose the 2018 election. It was a kind of strangely shaped district at the time.

Divestment in Chicago Operating Funds?

2 March 2018: More on Divestment: Your Money? Go For It. Other People's Money? Be Careful.

CHICAGO: LET’S PLAY POLITICS WITH OUR MILK MONEY!

Chicago treasurer: Use city’s investment portfolio to fight climate change, promote social progress

As New York City sues oil companies and plans to dump investments in fossil fuel production, Chicago Treasurer Kurt Summers is pushing to go even further and use the $7 billion portfolio of the nation’s third-largest city to help fight climate change and promote social progress.

Summers is proposing to overhaul the city’s investment strategy to ensure taxpayer dollars are directed to financially sound companies that make it a priority to protect the environment, encourage gender and racial diversity, uphold labor standards and operate ethically.

Instead of just divesting from fossil fuel interests, Summers said, the city should phase out those investments and ensure the portfolio is carbon-neutral by 2020, meaning any money still tied up in oil and gas funds would be offset by investments in clean energy.

“We should be rewarding good behavior,” Summers said in an interview with the Tribune. “With the rapidly expanding use of analytics, we can promote change and avoid companies doing things that are harmful to consumers or to workers, things that ultimately put the city at risk.”

….

“Divestment is about taking money out of something,” said Arena, who acknowledged it will take time to educate colleagues and the public about the proposed social investment strategy. “It doesn’t address the question about where we want to go moving forward.”If the proposal is adopted, Summers said, Chicago would be the largest city in the world to invest based on environmental, social and governance, or ESG, factors in addition to the traditional focus on financial returns.

What are these $7 billion in assets that Chicago has to spend? It can’t be the pensions, because Chicago pensions are much more than $7 billion.

ESG for public pensions and other public money was a big theme for my 2018 posts.

Looking at the 2017Q4 investments earnings call, I see that it’s mainly fixed income stuff, of short duration — so these are assets intended to fund operations. Okay, that I can understand – taxes come in and payments go out, and they are not necessarily at the same timing.

So this is what I call the “milk money”. Most of this needs to be short-term (one year or less) “paper” – aka fixed income. This isn’t investing in stocks. The Investment Policy I see as of 1 March 2018 seem pretty standard to me, given what these funds are.

There is no business playing around like this. You are simply making the investment process more expensive by getting this picky. You care about credit worthiness. That’s it. This ain’t long-term investing. That’s the whole point.

It doesn’t make a lot of sense to talk about long-term impacts about these short-term investments. It would make far more sense with respect to public pensions.

Chicago tried a different way to use their supposed political muscle by saying they wouldn’t do business with banks that would do business with gun-related firms… and, well:

10 May 2018: Banning All Things Gun: It's a Poor Weapon That Points Only One Way

CHICAGO CAN’T DROP THEIR GUNS

So while increasingly-desperate-to-get-re-elected Cuomo thrashes about, we find that Chicago can’t make it stick:

Even in Chicago, Plan to Push Gun Control on Wall Street Stalls – Bloomberg:

Few places know the toll of gun violence as well as Chicago. But even the city that saw more than 2,700 shootings last year is finding out that using economic muscle to push Wall Street into enforcing gun control is easier said than done.

On Monday [April 16], the Chicago City Council’s finance committee put on hold an ordinance that would have barred the city from working with banks whose clients failed to adhere to certain policies, such as not selling firearms to anyone under 21 or dealing in high-capacity magazines. Mayor Rahm Emanuel introduced the proposal three weeks ago in the wake of the school shooting in Florida, saying “when it comes to fighting for stronger, smarter gun laws Chicago is putting our money where our mouth is.”

The plan stalled in the face of opposition from the entities it seeks to police. The Illinois Bankers Association called the measure “overly broad.”

If enacted, a financial institution couldn’t win or renew city contracts unless it “adopted a safe gun sales policy applicable to its retailer clients, partners or customers.” The result was a proposal that could have hampered Chicago’s ability to deposit or borrow money — especially given that the city already has a junk rating from Moody’s Investors Service, making it more difficult to float bonds.

Yeaaaaahh, it’s more to the point that Chicago can keep borrowing money. For now.

If Chicago was finding it tough to find banks willing to do business with it, it may have been the case that the banks had the leverage, not Chicago.

Panoply of Chicago Stupidity

Unlike prior years, you had to wait until August to get a Chicago-centric post. It touches on divestment as above, but also has two other items: UBI and POBs.

(I love my TLAs)

19 August 2018: Chicago Stupidity: Universal Basic Income, Pension Obligation Bonds, and Divestment

SURE, LET’S DO UNIVERSAL BASIC INCOME IN CHICAGO

Even though they can’t pay for their pensions. But hey, another town trying out UBI, Stockton, California, can’t really pay for pensions, either. So nothing new.

So let’s check the arguments. First up, Dan Hemel, the tax law professor with the New York could disclose Trump’s tax returns! theory.

Why Chicago should test a ‘basic income’ program

….

“Third, a basic income pilot in Chicago would bolster the city’s reputation as an innovation hub for social policy. Ever since Jane Addams and Ellen Gates Starr co-founded Hull House in 1889, Chicago has attracted activists, philanthropists and social scientists seeking solutions to the problem of poverty and its consequences. A pilot here could re-establish Chicago as a city to which others look for policies that work.”

HA HA HA HA HA HA. Jeez. No.

Chicago’s track record on policy (as a city):

Public finance: failure

Funding pensions: failure

Homicide: failure

Education: failureTo be sure, there are some great universities in/around Chicago, but I’m talking about policy re: the city itself. I really don’t see anything that smells of success, other than they’ve not totally run away all their business. So yay for that.

The second item was pension obligation bonds. I don’t need to get into the details, but some folks were proposing POBs as a solution to the deeply-underfunded pension situation for Chicago.

I am not going to copy over my full rant, but just get to the end:

I mainly want to know: who the hell does Chicago think will buy these bonds? And what will happen when Chicago has to default on these bonds because they’re overextended on their credit everywhere?

Seeing the stories about the Puerto Rican bonds, and digging into that ownership info, made for really ugly reading — too many retired people had a piece of that disaster because they were desperate for yield… and government doesn’t go out of business…. right? right? Then they get pennies on the dollar from the vulture hedge funds who can afford to sit around and try to wangle a bigger settlement in court, whereas the retired investor really needs that cash flow that they thought was guaranteed. When it wasn’t.

That’s an extremely ugly dynamic.

Even though interest rates have been going up, the rates are still very low and there are many bond-heavy entities desperate for yield. Also, it looks like a calm-before-the-perfect-storm for these POB deals: try to lock in the lower rates before rates go up… and dump all that $$$ in equities and other volatile assets after years of positive returns. And after years of no credit slump…. We won’t get something worse than 2008 again, right?

I just want to know who they think will buy, and who would actually buy if this horrid idea gets off the ground. That’s the first thing I would ask.

It’s all moot (and I didn’t even talk about the idiotic $100 billion super-duper Illinois POB idea that was floating around). Thank goodness increasing interest rates really killed off these “great” ideas.

Third item was divestment.

CHICAGO TEACHERS: LET’S DIVEST!

Chicago Teachers to Ban Pension’s Private Prison Investments

The Chicago Teachers’ Pension Fund added immigration detention centers to its list of prohibited investments Aug. 16.

Companies such as GEO Group Inc., CoreCivic Inc., and General Dynamics Corp. are among those that own or operate the private prisons that have come under fire lately amid allegations of abuse of immigrant detainees.

A spokeswoman told Bloomberg Law that pension trustees want investment managers to also “prudently liquidate public market holdings in private prison companies as soon as reasonably practical and in accordance with the managers’ fiduciary duties.”

Right, so they’ll acknowledge fiduciary duty enough that they don’t want to take a (big) loss on liquidation, but the reason they’re divesting has nothing to do with the actual returns on investment.

….

Here’s one big piece of info that was not included in this short piece: how well-funded the Chicago Teachers Fund is.

The funded ratio has been going down and the contributions have been skyrocketing. Fiscal year 2017 was the closest they came to making full contributions… and those aren’t real full contributions if the funded ratio goes down. It means the unfunded liability was being negatively amortized.

In short, they are messing around with trivia. Don’t give me a HOW DARE YOU THIS IS IMPORTANT!

I would like to know what %age of the Chicago Teachers portfolio was exposed to private prisons. That would also have been a useful piece of information.

Also, they have a list of prohibited investments — I want to see this list.

I looked at their investment policy, and other policies, and they all looked pretty standard. I couldn’t find the list of prohibited investments, but I did find this recent press release re: “yeah, we’re still divested from guns”.

That’s one of the problems with divestment from a political point of view: you can really only do it once. It has the impact of a wet noodle if some big issue comes around and you divested from that evil industry 5 years ago. You can try to crow “Look! We were pure before everybody else!” But some nasty person might ask how well that sector of assets did in the period you were divested.

And a tweet:

I prefer a different deal: they get to play SJW with their own pension money… and if returns fall short, their pension benefits are adjusted (as with Wisconsin). Only seems fair. Have to have skin in the game

— Mary Pat Campbell (@meepbobeep) August 18, 2018

I had more on the Chicago POB idea here:

27 Aug 2018: Chicago Pension Obligation Bond Idea: It's the Discount Rate, Stupid

It’s never the places that have handled their finances well that issue POBs.

I know Alicia Munnell et. al. have said that theoretically POBs can be good, but it is contingent on a bunch of behaviors that most POB issuers have not been following for decades. It’s like saying subprime mortgages have great features for prime borrowers.

Isn’t that a great catch, that Catch-22?

Bye Bye Rahm

5 Sept 2018: Pre-Mortem: Rahm Emanuel Bows Out of Mayoral Race

I may live in New York, but I like keeping up with Chicago politics (mainly because of its really bad public finance performance, more than anything else)

So, it was a little surprising to hear the following (but not overly surprising):

Wall Street Journal: Chicago Mayor Rahm Emanuel Won’t Seek Re-Election

….

While I wouldn’t call Rahm as bad as any Daley, I have been underwhelmed at his supposed problem-solving re: Chicago. That said, I’m not sure many people could do much better than the phony finance crap he’s been pulling.

I really doubt there will be any credible candidate for mayor who will be able to argue that Chicago needs to face facts that it is bankrupt, and then go onto getting elected. Too many political players out there still think there’s goodies to be had, which leads me to my next subject.

ONE GROUP TAKES CREDIT

There’s various theorizing (and I’ll have my own below), but The Chicago Teachers Union is trying to claim it was they who drove Rahm to this decision:

….

THE PARTY ENDS

I wrote this several times when Rahm first ran in 2011 — Daley left because the party was ending. Rahm did get to play with money a bit, but definitely did not have as much fun as Daley.

And the one after that?

Chicago is now onto mayor #2 after Rahm, and the CTU is also causing trouble for him, even though he wants to be buddy-buddy with them.

Isn’t that interesting.

The Litany of Bad Chicago Ideas

Post-Rahm’s announcement, I decided to run down the bad ideas being floated around Chicago, and how lame duck Emanuel had best avoid these as he was on his way out.

20 Sept 2018: Chicago is a Big Ball of Bad Ideas

BAD IDEA 1: UNIVERSAL BASIC INCOME

BAD IDEA 2: PENSION OBLIGATION BONDS

BAD IDEA 3: INVESTING PENSION FUNDS WITH DALEY CRONIES

I want to remind that the word nepotism originated in medieval clergy giving their nephews positions/business (of course, some of those “nephews” were actually sons) — maybe the city should not be doing business with the relatives of elected officials? I know it’s not the Chicago way, but ya gotta start somewhere.

BAD IDEA 4: ANOTHER DALEY AS MAYOR

BAD IDEA 5: EXPECT THE STATE TO BAIL OUT

MEANWHILE… FUNDS GRAB FOR CONTRIBUTIONS

This is not necessarily a bad idea. When the finances start going down, it helps to be the first pig to the trough:

CROWDING OUT: CHICAGO PENSION FUND DEMANDS INTERCEPT OF STATE GRANT MONEY

“The Chicago firefighters pension fund has filed claims with the Illinois comptroller for $3.3 million in shorted pension contributions, an action that could worsen city finances and service delivery.

“Chicago could be the latest municipality to face diversion of state money as a result of a pension intercept law that took full effect in 2018. Under that law, municipalities that fail to make full contributions to their police or fire pension funds can see state money meant for the local government diverted directly to the pension funds instead.”

….

My only main wonder is why there are so many people who think being the mayor of Chicago is at all an attractive position.

From an individual point of view, that’s the worst idea of all. But I guess somebody has got to be the loser to take all the pain.

And indeed, people did line up to battle for the position.

What suckers.

My kind of town, full of comic relief🤪🤪🤪!!