In this episode, I discuss the new version of Actuarial Standard of Practice 4, Measuring Pension Obligations, and its requirement of calculating and disclosing a low-default-risk obligation measure. This standard went into effect in February 2023, so these numbers will be coming out in reports to come, and will be most notable in disparities to the standard valuation of public pension obligations, which tend to use much higher discount rates, leading to much lower values. What may happen?

Episode Links

Actuarial Standard of Practice 4

3.11 LOW-DEFAULT-RISK OBLIGATION MEASURE

When performing a funding valuation, the actuary should calculate and disclose a low-default-risk obligation measure of the benefits earned (or costs accrued if appropriate under the actuarial cost method used for this purpose) as of the measurement date. The actuary need not calculate and disclose this obligation measure more than once per year.

When calculating this measure, the actuary should use an immediate gain actuarial cost method.

When calculating this measure, the actuary should select a discount rate or discount rates derived from low-default-risk fixed income securities whose cash flows are reasonably consistent with the pattern of benefits expected to be paid in the future. Examples of discount rates that may meet these requirements include, but are not limited to, the following:

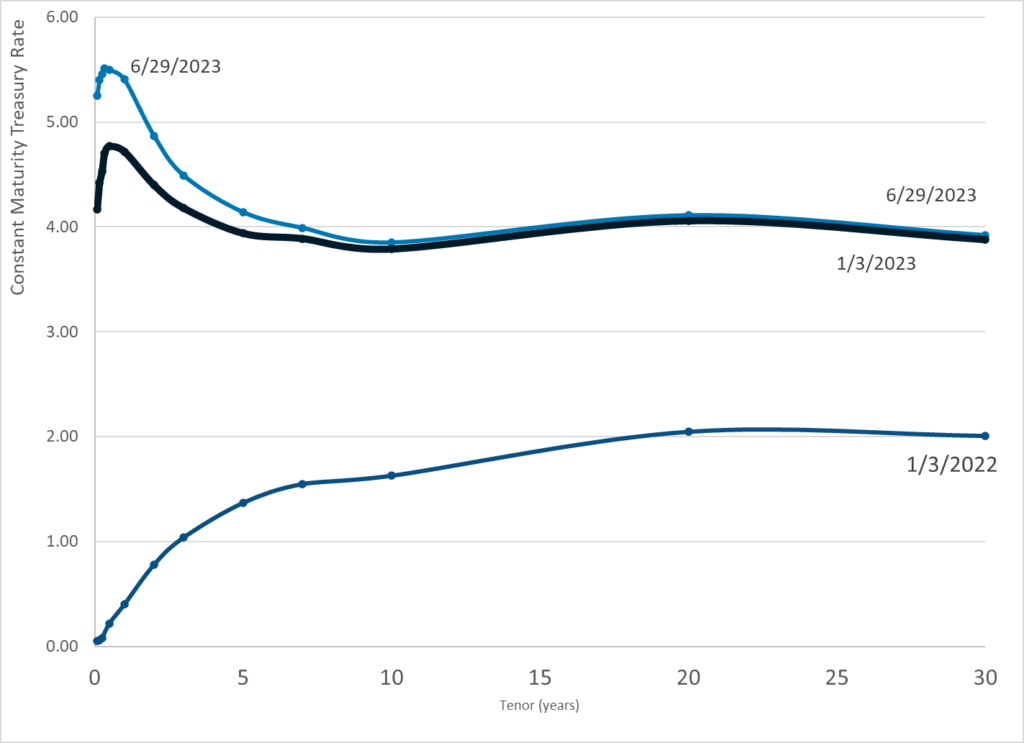

US Treasury yields;

rates implicit in settlement of pension obligations including payment of lump sums and purchases of annuities from insurance companies;

yields on corporate or tax-exempt general obligation municipal bonds that receive one of the two highest ratings given by a recognized ratings agency;

non-stabilized ERISA funding rates for single employer plans; and

multiemployer current liability rates.

When plan provisions create pension obligations that are difficult to appropriately measure using traditional valuation procedures, such as benefits affected by actual investment returns, movements in a market index, or other similar factors, the actuary should consider using alternative valuation procedures such as those described under section 3.5.3 to calculate the low-default-risk obligation measure of those benefits earned or costs accrued as of the measurement date.

For purposes of this obligation measure, the actuary should consider reflecting the impact, if any, of investing plan assets in low-default-risk fixed income securities on the pattern of benefits expected to be paid in the future, such as in a variable annuity plan.

When calculating this measure, the actuary should not reflect benefit payment default risk or the financial health of the plan sponsor.

Other than the discount rate or discount rates, the actuary may use the same assumptions used in the funding valuation for this measure. Alternatively, the actuary may select other assumptions that are consistent with the discount rate or discount rates and reasonable for the purpose of the measurement, in accordance with ASOP Nos. 27 and 35.

The actuary should provide commentary to help the intended user understand the significance of the low-default-risk obligation measure with respect to the funded status of the plan, plan contributions, and the security of participant benefits. The actuary should use professional judgment to determine the appropriate commentary for the intended user.

Actuarial News

Daily Treasury Par Yield Curve Rates – 29 Jun 2023

Prior STUMP Death & Taxes Episode

MBTA and Pension Obligation Bonds

Listen now (19 min) | STUMP - Meep on public finance, pensions, mortality and more is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Other STUMP posts

July 2014: Public Pensions Watch: Tell the Actuaries What You Want To Know

That’s when the revision began….

February 2017: Public Pensions: Actuarial Assumptions and Professional Ethics

July 2018: Actuarial Standards of Practice on Pensions: ASOP 4 - a Call for Comments

March 2019: An Ugly Interest Rate Environment and Public Pensions Chasing Returns

January 2020: Revisiting Actuarial Standards: ASOP 4 Has Second Exposure Draft

Share this post