Let’s consider a core principle of finance, as announced by fictional character Wilkins Micawber of David Copperfield, by Charles Dickens: “Annual income twenty pounds, annual expenditure nineteen pounds nineteen [shillings] and six [pence], result happiness.

Annual income twenty pounds, annual expenditure twenty pounds nought and six [pence], result misery.” In short: if you continually spend more than you bring in, you will surely come to grief. This core concept applies to public finance as it does to personal finance, and we will be seeing this in our journey during 2023. Come along with me!

“Annual income twenty pounds, annual expenditure nineteen pounds nineteen and six, result happiness.

Annual income twenty pounds, annual expenditure twenty pounds nought and six, result misery.” — Mr. Micawber, from the novel David Copperfield

Episode links

Prior STUMP posts

Jan 2023: Back to Basics on Public Finance

Feb 2016: Living Beyond Your Means Kills: Debt is Just the Killing Weapon

OVERSPENDING IS THE CAUSE

The point is the problem doesn’t come from the debt per se, but from the overspending all these years. One can overspend a little bit, take on a little bit of debt… but if that debt is never paid off, if one just keeps accruing more debt, and some of that new debt is just rolling over the old debt… there is trouble.

There is appropriate use of debt: 30-year bonds to cover the construction of a building that will last 30 years. A 1-year note to cover liquidity needs, due to lumpiness of tax receipts.

Not appropriate use of debt: 30-year bonds to pay for that 1-year note.

But if you keep overspending your income, that’s where you end up.

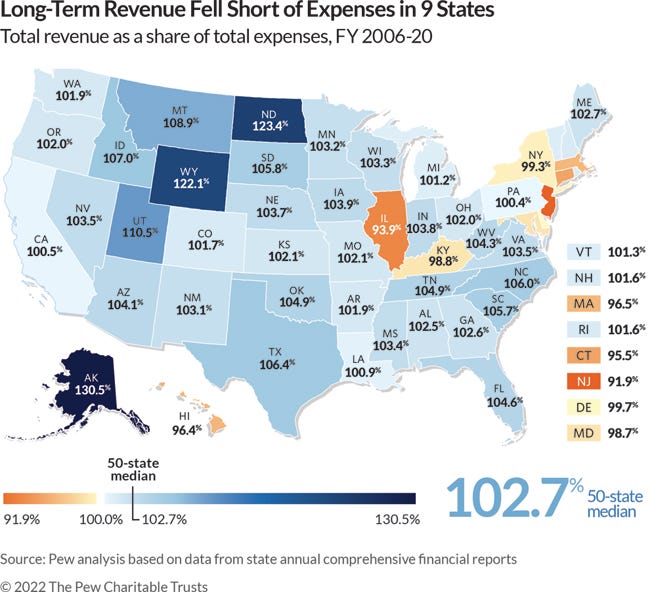

State Long-Term Revenue vs. Expenses

Dec 2022: Nine States Began the Pandemic With Long-Term Deficits

Twenty states recorded annual shortfalls in fiscal year 2020, when the coronavirus pandemic triggered a public health crisis, a two-month recession, and substantial volatility in states’ balance sheets. States can withstand periodic deficits, but long-running imbalances—such as those carried by nine states—can create an unsustainable fiscal situation by pushing off some past costs for operating government and providing services onto future taxpayers.

States are expected to balance their budgets every year. But that’s only part of the picture of how well revenue—composed predominantly of tax dollars and federal funds—matches spending across all state activities. A look beyond states’ budgets at their own financial reports provides a more comprehensive view of how public dollars are managed. In fiscal 2020, a historic plunge in tax revenue collections and a spike in spending demands were met with an initial influx of federal aid to combat the pandemic. The typical state’s total expenses and revenues grew faster than at any time since at least fiscal 2002, largely thanks to the unprecedented federal aid. But spending growth outpaced revenue growth in all but five states (Idaho, Maryland, Missouri, South Dakota, and Virginia). And 20 states recorded annual shortfalls—the most since 2010 and four times more than in fiscal 2019.

Share this post