Choices Have Consequences: Public Pension Investments in Alternative Assets

Oversight and transparency lacks

This is the culmination of the “choices have consequences” series.

The prior posts:

I’m linking the prior posts as a starter because I’m arguing with others over the direction of a cause-effect chain on this one.

Core arguments

The opposing argument notes that public pensions have been getting into riskier investments with higher asset management fees.

I agree with this starting point.

The question is why pension funds are making these allocation decisions and the results of these allocation results.

One argument goes: these higher asset management fees are eating into investment returns, and also these assets are more volatile and have performed poorly, leading to losses, and then leading to pension benefit cuts.

The motive for shifting into these alternative asset classes, the argument goes, is the decision makers are buddy-buddies with the asset managers or get a cut of the take themselves, and follow-the-money. If only cheaper investment choices were made, such as broad market indices, say, the returns would have been there to support the pension funds and the benefit cuts would not have been made.

My argument is that the move into alternative assets is primarily so that pension systems can hang onto absurd valuation discount rates, and not have to ask for higher contribution amounts from taxpayers.

Basically, the pension promises were initially made, assuming that the systems could get “guaranteed” returns of 8%, as per the valuation rates being used… but that was becoming more and more clear such returns would not be achievable with boring old publicly-traded stocks and bonds.

Thus, the shift into alternative asset classes.

Their choices were to keep the vanilla portfolios, have to reflect reality (or financial economics) and reduce the valuation discount rate, which would then tell them they would have to contribute a hell of a lot more money to the pensions…. which they did not want to do or they could hang on tight to that valuation rate and shift into a riskier mix of investments.

What do you think public pensions did?

Example: New York Looking to Increase Allocations to Alternatives

David Sirota, February 2, 2023: US pension funds are on the brink of implosion – and Wall Street is ignoring it

Earlier this month, PitchBook – the go-to news outlet of the private equity industry – declared that “private equity returns are a major threat to pension plans’ ability to pay retirees in 2023”.

With more than one in 10 public pension dollars invested in private equity assets – and with states continuing to keep their private equity contracts secret – PitchBook cited a new study finding that losses from the investments may be on the horizon for retirement systems that support millions of teachers, firefighters, first responders and other government employees.

….

In general, private equity firms use pension money to buy up and restructure companies to then sell them at a higher price than they were purchased. In between buying and selling, there are no transparent metrics for valuing the purchased asset – private equity firms can manufacture an alleged value to tell pension investors (and there’s evidence they inflate valuations when seeking new investments).In a story about an investor receiving two different valuations for the same company, Institutional Investor underscored the absurdity: “Everyone Wants to Know What Private Assets Are Really Worth. The Truth: It’s Complicated.”

Meanwhile, valuation and fee terms in contracts between private equity firms and public pensions are kept secret, exempt from open records laws.

….

“The desire for alternatives remains very strong,” the president of Blackstone, Jon Gray, said in an investor call last week. “New York’s state legislature actually increased the allocation for the big three pension funds here by roughly a third.”Gray was referring to New York Democratic lawmakers passing legislation significantly increasing the amount of retiree money that pension officials can deliver to Wall Street. The bill was championed by the New York City comptroller, Brad Lander, just weeks after the Democrat won office promising he would be “reviewing the funds’ positions with risky and speculative assets including hedge funds, private equity, and private real estate funds”.

The New York governor, Kathy Hochul, quietly signed the legislation on the Saturday before Christmas, just weeks after the Wall Street Journal reported that analysts have started warning pension funds of looming private equity losses. New York lawmakers simultaneously rejected separate legislation that would have allowed workers and retirees to see the contracts signed between state pension officials and Wall Street firms managing their money.

As a New York State taxpayer, that makes me feel great.

Weak oversight due to lack of knowledge and transparency

That said, it doesn’t really what the original motives were, when pension fund governance is lacking.

For all I might disagree with Edward Siedle and David Sirota about the motives behind the large shift into alternative assets by public pension funds, I do agree with the issues about lack of transparency and inadequate governance by public pension trustees.

Edward Siedle, April 11, 2023: State Pensioners Can Learn Lots From Rhode Island And Ohio Teachers

If you are a participant in a state or local government-sponsored pension fund, then a portion of your hard-earned retirement savings is likely invested in cryptocurrency or a cryptocurrency-adjacent enterprise. According to a 2022 study published by the CFA Institute, a staggering 94% of state and government-sponsored pension funds are invested in one or more cryptocurrencies despite the obvious risks. The attraction to this high-risk asset class is largely driven by the perception that cryptocurrencies have delivered spectacular returns over the last 12 years. Never mind that legendary investor Warren Buffett says “cryptocurrencies basically have no value and don’t produce anything,” America’s public pensions—often regarded as the dumbest institutional investors in the world by Wall Street—think they’re smarter than Buffett and are eager to gamble on cryptocurrencies. (Likewise, Buffett’s repeated warnings about private equity and hedge funds have long been ignored by public pensions.)

….

The lesson here, says Santos, is that pension fund managers must take extreme care to understand the properties of each digital asset at the time of the investment, and they must continue to monitor that asset for potential programming changes that could render the investment unlawful per one or more applicable regulatory frameworks. Consequently, unless the current regulatory framework is changed by an act of Congress, she believes no pension fund can in good faith invest in any of these crypto-products.

As I point out in my book, Who Stole My Pension? public pensions are overseen by lay boards which lack even rudimentary investment knowledge. Further, the lavishly-compensated, bloated investment staffs at the even the largest state funds are no match for Wall Street hucksters. Will public pensions will be able to fully understand the extreme risks related to rapidly-evolving digital assets, as well as continuously monitor for potential changes? Not likely. When asked, public pension officials admit they don’t even know the full extent of their direct and indirect (through funds) cryptocurrency holdings. For good reason, they’re not asking and their Wall Street money managers aren’t telling.

Public pension funds are chasing returns, but those who are supposed to be providing oversight have a questionable level of ability to provide adequate oversight.

And unlike with public securities, which has plenty of publicly-reported values for taxpayers, retirees, public employee unions, and other interested parties to check, these private assets have no values one can really check until they are actually turned into cash.

It’s a matter of “trust us”… and there has been plenty of reasons not to trust based simply on assertion, don’t you think?

Update to public pension fund assumptions vs performance reality

Back in August 2022, I took a look at how public pension funds really fared against their long-term return assumptions. Data are from the Public Plans Database, and I just updated this right now.

It only went up to fiscal year 2021, then. This is what it looks like with fiscal year 2022 added:

Isn’t that pleasant?

The dots are the actual 10-year average returns at each fiscal year, and the lines show the 25th percentile, median (50th percentile), and 75 percentile of the assumed rate of return on assets. Yes, those percentiles are often exactly the same… and yet the actual 10-year average returns vary quite a bit more.

These are the time-weighted geometric averages, by the way. The dollar-weighted averages will likely differ.

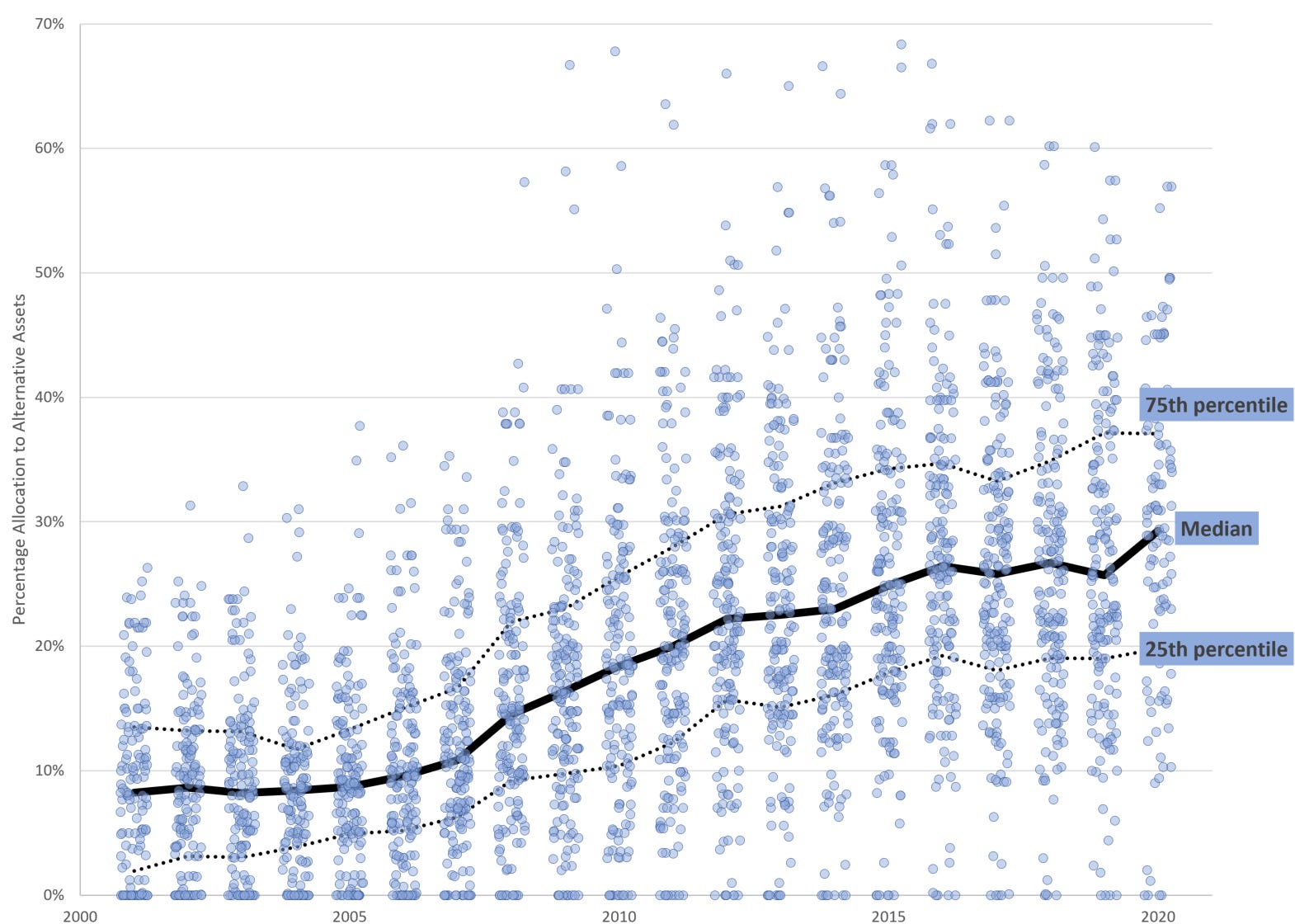

Performance and allocations to alternative assets

I’ve also done comparisons of how those with higher allocations to alternative assets have fared.

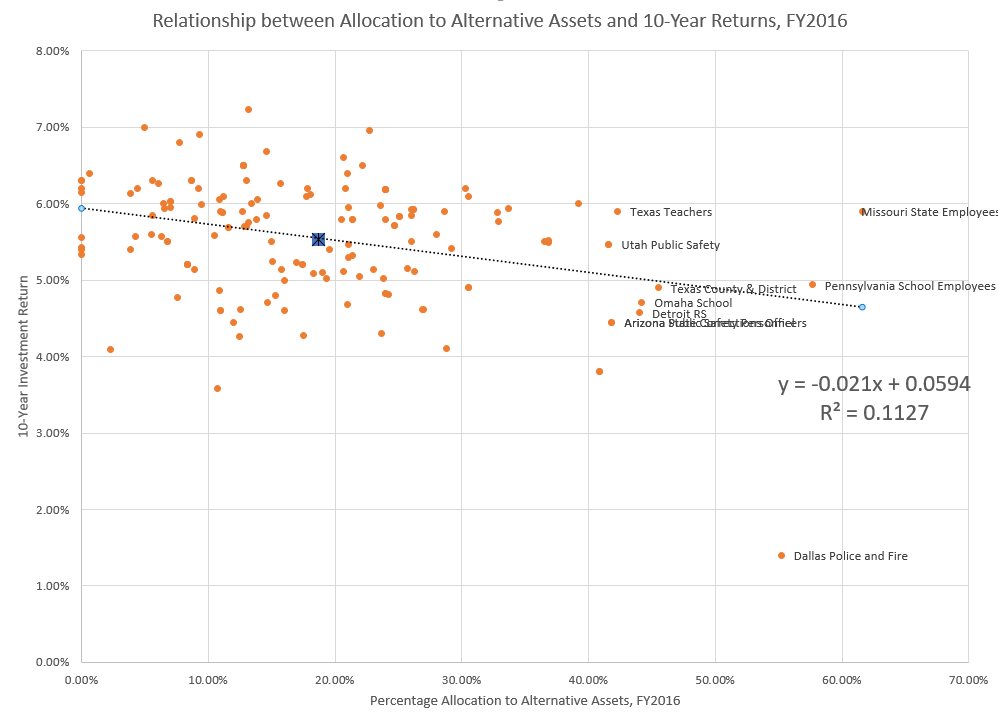

2018: Alternative Assets and Pension Performance: A Dive into Data

Observations: in each case, I end up with a negative sloping line, meaning higher allocations to alternatives are associated with lower returns. Part of this is due to the outlier of Dallas Police and Fire, with its super-high allocation to alternatives, and its disastrous investment history.

But even removing that point, I’d end up with a negatively sloping line….

….but that said, check out those R^2 stats.

Those are really low.

So, no, high use of alternatives definitely is not related to great investment returns….

….but it’s not really indicative of crappy investment returns, either.

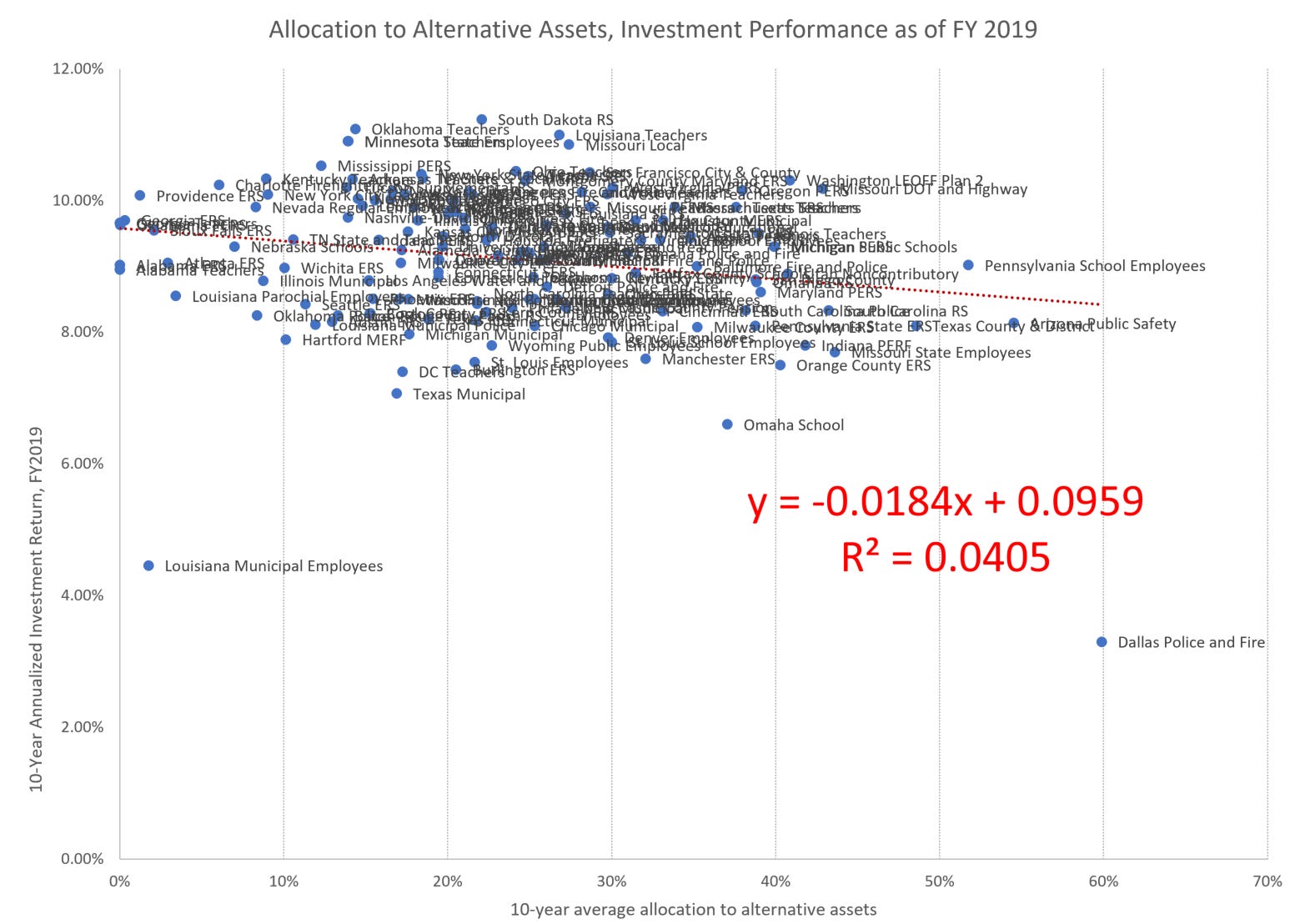

2021: Which Public Pension Funds Have the Highest Holdings of Alternative Assets? 2021 Edition

In both cases, there’s a slight negative correlation… but the fit is extremely poor (as measured by R^2).

Essentially, to the extent there are performance differences, the broad variable of allocation to alternative assets makes little difference.

I’m not going to even bother showing you the other scatterplots I made regarding funded ratios and allocation to alternative assets. They were also weakly negative.

My theory was that some pension funds are chasing investment returns via alternative assets, in order to make up for eroding funding status (as opposed to, ya know, increasing the contributions more.)

But if there is a measurable connection, I’d have to measure it some other way… and keeping changing what one measures in order to shoehorn it into a theory is just not how I roll.

Pretty much, every time I have looked, there is a slightly negative correlation between allocation to alternative assets and public pension fund returns (10-year), but it’s a weak correlation.

And that could simply show that these funds had poorer returns, and then increased allocations to alternatives as a result, because they were trying to chase yields.

Given none of these funds have static allocation percentages to alternative assets, it might be interesting (later) to see if the lower-returning or underfunded funds were more likely to increase allocations to alternative assets, meaning the negative returns were more tied to them already having a bad performance history to begin with.

Smart money or dumb money?

Some funds, I’m sure, do well with their alternative investments, but in many of these cases, it actually is hard to tell how the investments are doing until they actually cash out.

As David Sirota wrote above, it’s hard to get reliable valuations for private investments until they are actually liquidated. In many of these cases, the public disclosures are minimal, which can be of questionable appropriateness for public pension funds, though it may be appropriate for other types of investments.

The problem here is a big principal-agent problem (and it’s principal-agent problems all the way down).

Whether I’m right that the primary motive is to avoid needing higher contributions to the pension plans, or Siedle/Sirota are correct that it’s all about enriching asset managers [or maybe we’re all correct], we’re all in agreement that the agents intended to safeguard the pension plan participants’ interests, the pension fund trustees, cannot possibly provide adequate oversight of these assets given the lack of transparency and the lack of understanding they have of the risks involved.

It would have been one thing if it were small portions of the pension fund portfolio, but for many pension funds, especially the most underfunded, alternative assets have become a substantial portion. Market downturns can have an outsized effect, especially on the leveraged strategies behind many of these assets.

I had been hoping that there would be some pulling back from alternatives in the last few years, but the opacity means that there can be even more enticement as there is a “smoothing” to valuations. Until, all of a sudden, things are re-valued to a whole lot less.

Then… surely, that last alternative asset of all, the “taxpayer put”, will pay off… right?

Um, right?

Related posts

Nov 2022: Some Public Pensions Take (Small) Losses from FTX Disaster… But What About Other Alt Messes to Come?

May 2021: Which Public Pension Funds Have the Highest Holdings of Alternative Assets? 2021 Edition

2020: Public Pensions, Leverage, and Private Equity: Calpers Goes Bold

2018: Alternative Assets and Pension Performance: A Dive into Data

2014: Public Pensions Watch: Don’t Go Chasing Waterfalls….or Alternative Asset Classes, pt 1 of many

August 2014: Public Pensions Watch: Dallas Pension Learns About Concentration Risk

September 2014: Public Pensions and Alternative Assets: Dallas Shows How It Can End

2017: Public Pension Assets: Our Funds were in Alternatives, and All We Got Were These Lousy High Fees

2015: Reddit-Public Pension Connection: Alternative Assets and Risk

2014: Public Pensions Watch: More Reactions to Calpers Pulling Out of Hedge Funds

2014: Public Pensions Watch: Alternative Assets, pt 8 of many — New Jersey followup

Spreadsheet: