Ohio STRS Drama Continues: Subpoenas Filed Against Some Board Members

There may be less there, on both sides, than people think... and the solution would be very unpopular

The following showed up in my pensions news alert this morning:

Pensions & Investments: State attorney general subpoenas Ohio State Teachers' pension fund board members

The Attorney General of Ohio, Dave Yost, filed subpoenas on August 23 in the Court of Common Pleas, Franklin County, Ohio, in connection with the ongoing turmoil at the $95.3 billion Ohio State Teachers' Retirement System, Columbus.

In the subpoena, Yost said some individuals, including current SRTS board members Wade Steen and Rudy Fichtenbaum, should be removed from the board for failing their fiduciary duties. Specifically, the subpoenas allege that Steen and Fichtenbaum sought to invest up to 70% of STRS assets with a private investment firm called QED, which Yost described as a “shell company that lacks any indicia of legitimacy and has backdoor ties to Steen and Fichtenbaum themselves.”

There is a lot more to the P&I article, but it primarily covers the ground we’ve seen in prior posts. There is no new information on the investment firm QED, which is why there are subpoenas, I suppose. Gotta dig for more info.

Let’s look at some other media coverage, from local sources:

Ohio Capital Journal: Ohio AG Yost files subpoenas in teachers pension scandal; investment firm responds

Ohio Attorney General Dave Yost has filed a slew of subpoenas against individuals he has accused of bribery as a major scandal brews inside the retired teachers’ pension fund. The investment firm at the center of the controversy is now speaking out.

….

QED was started by former Deputy Treasurer Seth Metcalf and Jonathan (JD) Tremmel. Metcalf worked under Josh Mandel in multiple capacities, including as deputy treasurer and general counsel. In 2020, they set their eyes on STRS, according to the main 14-page memo.

The documents claim that they — despite having no clients and no track record — tried to convince STRS members to partner with them.

They couldn’t impress the board members, mainly because of their lack of experience and also because QED was not registered as a broker-dealer or investment adviser. The men also didn’t own the technology to “facilitate the strategy,” the documents say.

Steen and Fichtenbaum had allegedly been bidding continuously, pitching QED’s direct documents to board members and proclaiming the company’s talking points to other staff.

The AG states that the pair should be removed because they broke their fiduciary duties of care, loyalty and trust when “colluding” with QED.

This fight began from a debate on how STRS should invest money — through the current system of actively managed funds versus an index fund. Active funds try to outperform the stock market, have more advisors and typically cost more. Index funds perform with the stock market, are seen as more passive, and typically cost less.

In short, “reformers” want to switch to index funding, while “status quo” individuals want to keep actively managing the funds. Recent elections have allowed the “reform-minded” members to have a majority of the board.

Reformers want a cost-of-living adjustment, or COLA. The COLAs were suspended for more than 150,000 retired Ohio teachers for five years starting in 2017. They were reinstated, but there has been a suspension of increases, significant for retirees who need this money and are dealing with inflation.

….

I’ve obtained his eight newly filed subpoenas. They went to QED’s three separate entities, a business called OhioAI, STRS, Metcalf, Tremmel and former STRS board member Bob Stein.

For his first time talking about the civil suit, Metcalf answered some of our questions over email. We were not able to have a back-and-forth but may be able to in the future.

“QED is surprised and disappointed that the Attorney General’s office did not reach out to QED during the three years the office has been aware of the anonymous accusations,” Metcalf said. “Allowing QED to illuminate the truth could have saved taxpayer money.”

Metcalf is referencing prior allegations of concerns from STRS staff about the relationship between QED and several board members.

There is more at the link; the piece's author is Morgan Trau. Lots of interesting detail there, and Morgan Trau has had good coverage of the Ohio STRS saga. This piece was originally published at News5Cleveland, which has a video in its coverage.

Let me provide a quick summary before a few comments.

Nutshell review:

Let me make this very simple:

The driving force is the Ohio teachers, especially current retirees, being unhappy about not getting cost-of-living increases on their pensions since 2017 (yes, some COLAs are coming back, but let’s push that to one side)

Ohio STRS has the feature of the pension plan participants being able to vote in most of board of their pension plan, and thus if enough plan participants are angry enough, they can take control of said board. They have taken control of the board. (There are complications — see news items above or my links to old posts below)

Some on the angry teacher/retiree side think that what led to COLA cuts were asset-side troubles (high expenses, fees, underperformance, etc.)

Some have championed this QED group, which do not have an investment track record, and rumors have popped up about nefarious doings….

AG Yost filed a complaint in May, over a supposed board takeover, and legal doings are afoot in Ohio.

Blast from the past: Calpers Pay-for-Play Scandal

When a big pot of public money sits there, there is an enticement for all sorts of corruption.

Ohio STRS had $84 billion in assets for fiscal year 2023. That’s a sizable draw for any asset manager, if they got to manage all of those assets. That is legit business, but also, there has been less-than-legit ways of acquiring business involving public corruption.

So let us go back to a public pension asset management scandal from California, involving a huge chunk of change and public corruption:

Oct 15, 2009, WSJ: Calpers Rocked by 'Pay to Play'

America's largest public-pension fund, Calpers, revealed that a former board member had reaped more than $50 million in fees for arranging investments that could saddle state taxpayers with hundreds of millions of dollars in losses.

The disclosure deepens concerns that alleged conflicts of interest are undermining state retirement funds.

The California Public Employees' Retirement System said it is launching a "special review" into payments by money managers -- including billionaire Leon Black's Apollo Management LP -- to firms including Arvco Financial Ventures LLC. Arvco is headed by Al Villalobos, who served on Calpers's board from 1993 to 1995.

That was just the initial disclosure.

It took years for the legal issues to work through.

Ed Mendel at Calpensions.com was my preferred source:

20 Jan 2015: Sad end for CalPERS private equity ‘golden years’

The apparent suicide last week of Alfred Villalobos, who faced a bribery trial next month, is a sad end for a former CalPERS board member paid more than $50 million by firms seeking money from the big pension fund.

Most of his fees came from private equity firms during the years leading up to the financial crisis in 2008. Some call the period private equity’s “golden years,” when leveraged buyouts of corporations yielded huge profits.

Villalobos flourished as a “placement agent” offering help for firms seeking investments or contracts from CalPERS, particularly after another former board member, Fred Buenrostro, became chief executive of the pension fund in 2002.

Now Buenrostro, who pled guilty to accepting Villalobos bribes, awaits sentencing in May. Pushed out of CalPERS in 2008 amid complaints of investment meddling, he received a $300,000 salary from Villalobos and possibly a Lake Tahoe condo.

6 June 2016: CalPERS ex-CEO sentenced, but probe continues

A former CalPERS chief executive officer, Fred Buenrostro, was sentenced to 4½ years in prison last week for taking bribes, including $200,000 in cash, from a former CalPERS board member, Alfred Villalobos, who collected about $50 million in fees from private equity firms for helping them get investments from the big pension fund.

Villalobos died from a pistol shot to the head at a Reno gun range in January last year, an apparent suicide on the day before a scheduled court appearance. His inside man at CalPERS, Buenrostro, pleaded guilty on the eve of his trial in July 2014 and has been cooperating since then with state and federal prosecutors.

Again, the Calpers example is just the worst one known (thus far).

Nobody wants to be the next horrific example.

Other legal matters with Ohio STRS

Back in 2023, I noticed Ed Seidle was trying to pry investment records out of Ohio STRS.

A lawsuit over private equity investments in Ohio

Yesterday, I saw this post from Edward Siedle:

Let me pull out the bits I want to discuss:

A decision is expected soon regarding a lawsuit filed over two years ago on behalf of tens of thousands of members of the Ohio Retired Teachers Association demanding that the $100 billion State Teachers Retirement System of Ohio disclose information about its private equity holdings—information which the SEC considers vital to protecting workers’ retirement savings. In complete disregard for regulatory concerns, STRS Ohio and its Wall Street money managers have long been committed to maintaining secrecy regarding tens of billions of state pension assets invested in over a hundred of these costly, high-risk private funds.

….

The SEC warns that because of their long-term investment horizon, an investment in a private equity fund is often illiquid and it may be necessary to hold the investment for several years before any return is realized. Private equity funds typically impose limitations on investors’ ability to withdraw their investment—often 10 or more years.

….

When investing in a private equity fund, the SEC notes that an investor usually receives offering documents detailing material information about the investment and enters into various agreements as a limited partner of the fund. These offering documents and agreements should disclose and govern the terms of the investor’s investment throughout the fund’s life, including the fees and expenses to be incurred by funds and their investors. These materials, which the SEC advises all investors (including participants in public pensions) read carefully, are the very same documents which members of the Ohio Retired Teachers Association have long demanded to see and STRS Ohio and its Wall Street money managers have steadfastly refused to disclose.

….

Last year, it was reported that the $440 billion CalPERS state pension sold a record $6 billion in private equity stakes to Wall Street at a 10 percent discount. That amounts to a $600 million transfer of workers’ wealth to Wall Street, in my opinion. Discounts on private equity secondary sales can be far greater, as much as 50 percent. In short, private equity assets may be grossly inflated, thus making public pensions appear better funded, i.e., less underfunded, than they really are. For their protection, pension stakeholders need access to information regarding private equity portfolios and corresponding values—they very information STRS Ohio and Wall Street are fighting to keep secret.

So, I will get into a few things here.

The main reason the private equity managers and funds don’t want this stuff public is because it’s PRIVATE equity.

If they wanted to go into public asset management, with all the SEC disclosures and requirements that entails (with the dangers of those sorts of lawsuits), they would have structured their fees (and priced them) accordingly. They do not want to set a precedent.

It doesn’t require anything nefarious to understand that.

That said, these are institutional funds involving private pensions. I have argued before that while illiquid assets are fine for public pension funds, at least for a portion of the portfolio, opaque assets may not be fine. There may not be appropriate oversight, and that’s what Siedle is arguing here. I agree.

Well, there has been some movement:

27 July 2024: Magistrate Orders Ohio Teacher Pension To Release Investment Documents--Finally

zzz

In 2021, I was retained by the Ohio Retired Teachers Assocation to conduct a forensic investigation of the State Teachers Retirement System of Ohio—the pension system ORTA’s members rely upon for their retirement security. In connection with my investigation, on February 19, 2021, I filed a request pursuant to Ohio law for an opportunity to inspect or obtain copies of public records related to the pension’s investment managers, investment consultants, performance compliance auditor, investment cost monitor, financial auditor, and custodians, as well as board and staff.

…..

Just yesterday the magistrate assigned the case found:

Siedle has established a clear legal right to the production of public records sought in the first investment managers request and the first Panda Investments request. STRS was under a clear legal duty to comply with these public records requests. Accordingly, it is the decision and recommendation of the magistrate that this court issue a writ of mandamus ordering STRS to comply with Siedle's first investment managers request in the February 19, 2021 letter.

Now that the magistrate has confirmed that I (and the public) has a “clear legal right” to the pension investment contracts, I trust that STRS Ohio will comply with its “clear legal duty” to provide them. The time has come for its members and taxpayers to see what the pension has been hiding for so many years.

I look forward to learning the secrets STRS Ohio has fought so hard for so long to keep from the public.

Further, these documents will confirm whether the alternative funds STRS Ohio has invested in are plagued with the same industry abuses that were identified in my High Cost of Secrecy report, as well as whether the pension may be able to recover any monies pilfered— funds that could be used to pay benefits promised.

I don’t think he’s going to find much.

It will certainly be paltry compared to the amount of benefits being paid out.

That may give a hint of the problems Ohio STRS has.

What if there’s no “there” there?

All that said…

…what if there’s nothing there? On either side?

For those seeking the answer on the COLA cuts:

What if the expense levels aren’t particularly high?

And the investment performance has been pretty good overall… and the only way you can make it look suboptimal is by cherry-picking the period?

What if, any investment losses that can be found, are the normal vicissitudes of investment and puny compared to the shortfalls in the pension?

For the AG Yost:

What if there is no conflict-of-interest/corruption/etc. with the proposed new strategies?

To be sure, there is still a due-diligence issue before a pension fund invests with anybody, but that doesn’t rise to a pay-for-play corruption case situation.

There may be nothing substantial for either side to find.

What then?

Both sides still have good points

So, there may be nothing nefarious going on, per se.

But there can be hard decisions to be made.

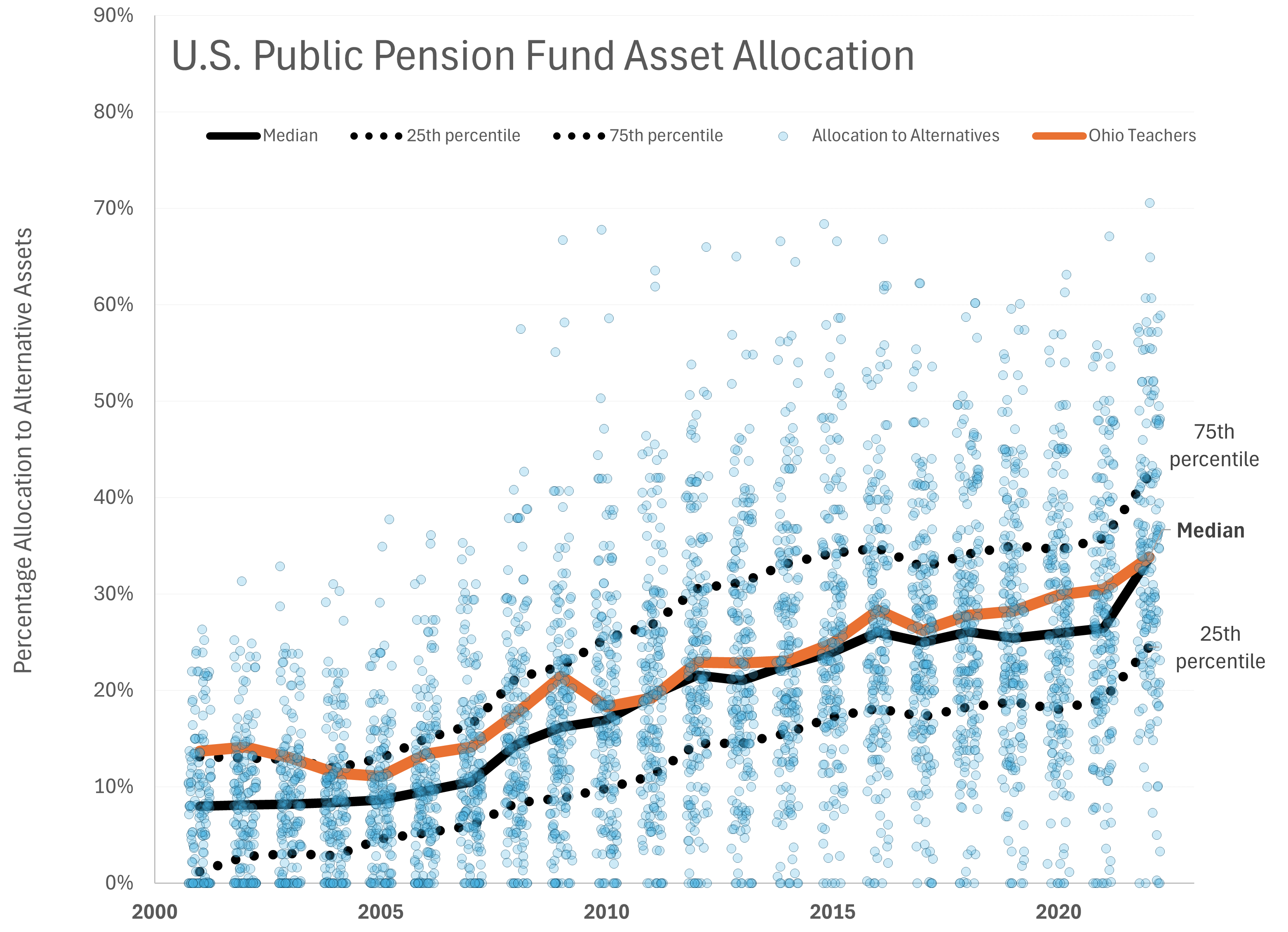

I made this plot in an earlier post:

Ohio STRS is middle-of-the-pack in allocations to alternative asset classes, among its fellow public pension plans.

All that said, even if the performance has been fine and the expenses have been moderate, are these appropriate investments for public pension funds?

Can the board provide appropriate oversight for this sort of investment approach? It does depend on what the “alternatives” are (some investments are much more exotic than others).

On the side of being skeptical of a total newbie investment group taking over a $84 billion fund… uh. Yeah. One may have some experience in investments in general, but $84 billion is quite a lot of money. It sounds like they’re lacking some simple operational capabilities. Maybe put things out to bid?

(That said, perhaps things are not being reported quite straightforwardly there, either.)

Even so, let us give these sides their good points.

….

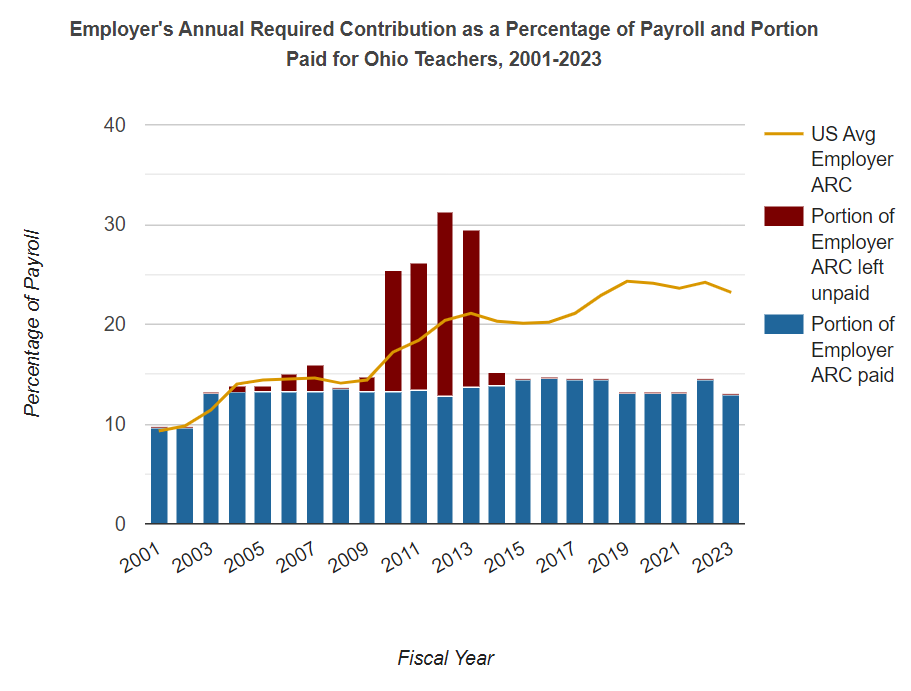

I don’t think the asset side is the problem at all.

If they want COLAs back, they need to increase contributions.

I know that’s not a popular solution, but that’s the one that would work better. Also, they could de-risk their portfolios some with a higher contribution pattern.

I have some other ideas, involving risk-sharing with the liabilities, but I know those would likely also be unpopular among those who want to argue over the assets.

Prior Posts on Ohio STRS

6 May 2024: Public Pension Governance Drama in Ohio

10 May 2024: Ohio Pension Drama Continues: Investigation Called on "Hostile Takeover"

16 May 2024: Ohio State Teachers Pension Drama Continues! Board Turmoil!

17 May 2024: More Ohio STRS Commentary: Alternative Assets in Pensions, Anonymous Memos, and Teachers Pensions in General [corrected/updated on May 22]

1 June 2024: Corrections and Clarifications on Ohio STRS: Audits and Investments

27 June 2024: Ohio STRS Drama Continues: No Bonuses and Board Member Resigns

15 July 2024: Ohio STRS Update for 15 July 2024: More Legislative Action, Advisor Resignation(s), Research on Public Pension Asset Returns

18 July 2024: Ohio STRS: Trade-Offs, Alternative Assets, and More