Taxing Tuesday: Taxes on the Ballot, Revenue Challenges, and the French Wealth Tax Impact

A short round-up of current tax issues

Three tax-related topics for this Tuesday.

Taxes on the Ballot: State Referenda

This is from the Tax Foundation: State Tax Ballot Measures to Watch in 2024

Taxes are on the ballot this November—not just in the sense that candidates at all levels are offering their visions for tax policy, but also in the literal sense that voters in some states will get to decide important questions about how their states raise revenue. North Dakotans will decide whether to abolish the property tax; Washingtonians will determine the fate of the state’s relatively new tax on capital gains income; Oregonians will rule on whether to implement the nation’s highest gross receipts tax rate; Utahns will resolve whether to keep income taxes fully earmarked for education; South Dakotans will choose whether to exempt groceries from the sales tax—and on it goes.

Some measures are modest; others are monumental. Below, we highlight eight of the most significant measures (often with links to further analysis), then briefly summarize all 21 tax-related measures on state ballots this fall. On Election Day, this page will be updated regularly with live results for the eight featured measures.

You can go to the link for all the 8 featured items and the table of 21 state-level tax items.

I’m picking two specific items, from Illinois and Washington state, to comment on.

Illinois

Illinois Income Tax Advisory Question

[emphasis added]

Illinois’ Income Tax Advisory Question is a non-binding question that would not change Illinois law but is designed to gauge public opinion. This advisory question asks voters if the state constitution should be amended to create an additional 3 percent tax on income exceeding $1 million to generate new revenue for property tax relief. Illinois’ constitution requires a single-rate individual income tax, and the rate is currently statutorily set at 4.95 percent.

Notably, the advisory question does not specify exactly how the language of the state constitution would be amended, nor does it specify how the property tax relief would be distributed. If a 3 percent surtax on income exceeding $1 million were enshrined in the language of the constitution itself—similar to the surtax adopted in Massachusetts in 2022—a future constitutional amendment would be needed for that rate to ever be reduced or eliminated, requiring a three-fifths vote in both houses of the Illinois legislature followed by approval from a majority of Illinois voters in a general election. With an additional income tax rate of 3 percent, Illinois’ top marginal individual income tax rate would be 7.95 percent, making it the 10th highest in the country. Pass-through businesses, which face an existing surcharge, would have a new top rate of 9.45 percent. If the constitution were amended to simply remove the flat tax requirement without prescribing new rates within the constitution, legislators could change Illinois’ income tax rate schedule in a manner that raises taxes on many Illinoisans. In 2020, a proposed constitutional amendment to remove the flat tax requirement was soundly rejected by Illinois voters.

Here is the deal.

Why are they wasting everybody’s time and money?

If they want to take an opinion poll, they can just take an opinion poll.

They were slapped down before in trying to get rid of the flat income tax requirement, to amend the constitution.

Fine, they say, but we only want to raise taxes on millionaires, like our governor J.B. Pritzker! You know, the guy who tried to avoid paying property taxes by disabling toilets in his fancy house while it was being renovated. I’m sure it will get us loads of money, because millionaires are known for straightforwardly paying taxes!

I guess we’ll see how this vote goes (“Sure, as long as it’s only millionaires!”), because Illinois politicians are too cowardly to just go forward and do the votes to try to amend the constitution without a non-binding vote as cover.

Washington

Washington Initiative 2109, Repeal Capital Gains Tax Initiative

[emphasis added]

Initiative 2109 would repeal a controversial tax on capital gains income. Despite constitutional restrictions on income taxation, Washington lawmakers implemented—and the state supreme court affirmed—a tax on high earners’ net capital gains income, with the court concluding that the tax is on the privilege of earning income, not on the income itself, even if it is levied according to net capital gains income. While the tax only applies to capital gains income of $250,000 or more, opponents have pointed to the tax’s volatility, as it is uniquely sensitive to stock market swings, as well as its vulnerability to the outmigration of high-net-worth individuals. Additionally, while regular year-to-year payers of the tax are certainly wealthy, most people who pay the tax at some point in their lives will be ordinary taxpayers who have just sold a home or business. And the logic employed by the court in approving the tax despite constitutional constraints could just as easily apply to wage income (a tax on the privilege of employment, or of earning wage income), and lawmakers have already begun considering lowering the capital gains income threshold to capture far more taxpayers. For more on the existing tax, click here. Additional analysis of the ballot measure is forthcoming.

This capital gains income tax is relatively new, having been enacted in 2021 and went into effect for tax year 2022.

More from Washington State Standard:

The capital gains tax levies a 7% tax on the sale or exchange of long-term capital assets, such as stocks, bonds, and business interests. It doesn’t apply to real estate sales and only covers gains above $262,000 (up from $250,000 for the 2022 tax year, as the floor is tied to inflation). So if someone has $263,000 in taxable capital gains, they would only pay the 7% tax on the $1,000 above that $262,000 threshold.

Lawmakers approved the tax in 2021. It took effect after the state Supreme Court upheld it in a ruling last year. The first payments were due in April 2023.

Each year, up to $500 million from the tax is deposited into a state account for schools, early learning, and child care programs. Any tax collections beyond that amount go to an account that helps pay for school construction and renovations.

Okay, let’s see the claims around the impact of the current tax and a repeal:

If the initiative passes, what would the consequences be?

The capital gains tax generated about $786 million in its first year and, as of May 15, collections in 2024 totaled $433 million. To put those numbers into perspective, the state’s current two-year operating budget is nearly $72 billion.

If the tax is repealed, it’ll mean a “big hole in the budget,” Sen. June Robinson, D-Everett, who chairs the Senate Ways and Means Committee and authored the capital gains tax bill, said earlier this year.

Okay, I understand that $786 million would be difficult to replace with another revenue source (see below).

But if I halve the $72 billion of a two-year budget to make for $36 billion annual budget, then that’s a 2% budget hole that needs to be filled.

That’s if I counted all $786 million, which I shouldn’t, as only $500 million is to be to the operating budget and the overage is supposed to go to capital improvements.

In which case — rejoice! Only 1.3% of the budget would need to be replaced!

That’s not a big hole.

I wrote about Washington’s capital gains tax in 2023:

State Revenue Challenges

Before I get into this, I want to point out Liz Farmer’s Long Story Short posts will be free for everybody for the next 12 weeks, so check it out. This is related to this section, as in the post in which she announces she has this teaser:

…because Liz Farmer is now working at Pew, and the graph comes from a recent piece:

How a Pandemic-Era Surge in Tax Collections Drove a Revenue Wave—and What It Means for Future State Budgets

Key findings

This analysis contextualizes recent revenue growth patterns within historic trends and is intended to complement more common approaches that states use to consider whether revenue collections are sustainable, such as the forward-looking analyses that typically underpin long-term budget assessments and budget stress tests. Pew’s analysis also adds a long-term lens to the picture and demonstrates ways states can better understand and manage revenue growth spurts in this context. See Appendix for detailed methodology.

Pew’s examination of the revenue wave found that:

Approximately 38% of tax revenue growth over three years—or $152 billion—exceeded pre-pandemic growth trends and may have been temporary in nature. From calendar year 2020 through 2022, 35 states collected more tax revenue than they were on pace for based on pre-pandemic growth trends. The portion of new growth that was above trend varied widely across states, ranging from more than 90% in Mississippi and New Mexico to less than 20% in Pennsylvania and Virginia. States with a higher portion of above-trend revenue benefited from having a greater influx of new funds, but they also deviated more from their pre-pandemic trends and thus had a higher risk of seeing those new funds disappear.

Cumulative collections in 15 states performed below their pre-pandemic trend line during the revenue wave, though most of them still had positive revenue gains after the brief recession. The states that underperformed compared with their pre-COVID-19 growth trends did so for a variety of reasons, and they should consider the possibility that inflation may have masked relatively tepid revenue growth. The breaking of the revenue wave may signal future fiscal strain for these states.

Infusions of federal aid during the pandemic and new state-level tax cuts complicated states’ efforts to identify temporary tax revenue. States received more than $800 billion from the federal government to help combat the pandemic’s negative economic impacts.3 Individuals also received stimulus funds that temporarily bolstered consumer spending and associated sales tax revenue. As the increased aid helped lift the economy, 48 states passed tax cuts or one-time rebates.4 Both the record-setting level of federal aid and the sheer volume of tax relief ultimately hindered states’ ability to identify the full scope of the revenue wave.

The new pace of growth was not sustainable and revenue collections have subsided. In early 2023, the revenue wave crested. Now, in fiscal 2025 and looking ahead, budget pressures are increasing as revenue begins to dip below pre-pandemic trends. If states do not have a way to identify how much of their tax revenue is temporary, fissures created during the pandemic will continue to grow.

Although policymakers understood that the revenue wave was temporary, states’ practices for measuring potentially one-time revenue vary and formal adoption of leading practices is limited. States can better understand revenue swings by creating formal definitions of above-trend revenue and recording what portion of revenue may be temporary versus ongoing in official estimates and budget documents. Forward-looking analytical tools such as long-term budget assessments also allow states to estimate the revenue outlook and can help them determine what level of collections are sustainable for the future.5

I am going to address the last bullet point intro “Although policymakers understood that the revenue wave was temporary”

There are two versions of politicians who inspire this cynical response. One type is the politicians who think numbers are magic and they can just ask pretty please for more money, no matter how brazen the request:

[from April 2020, when Illinois asked for money that had nothing to do with COVID… to be sure, they did get this… ish]

Illinois Asks for $10B(+) for Pensions -- Most Disgusting COVID-19 Bailout Yet?

Earlier this year, I said I would lay off Illinois for this year, and focus on states/localities closer to home.

The other type is the politicians who do understand that the revenue was temporary, but have to deal with large, growing expenses…. like pension contributions… and they don’t know where to cut.

Like in Chicago.

Good luck!

French Wealth Tax Post-Mortem

This is research into the net effect of the French wealth tax, which no longer exists. I do keep mentioning that every time Elizabeth Warren and crew keep trying to bring up their “clever” unrealized capital gains tax (aka wealth tax) idea.

I first noticed the paper due to Tyler Cowen’s post in Marginal Revolution: The Economic Consequences of the French Wealth Tax, where you can read some of Cowen’s readers’ comments.

But let us go to the paper directly.

Published in La Revue de Droit Fiscal, n° 14- 5 avril 2007

[emphasis added]

ABSTRACT

Despite attempts to “un-wind” the Impôt de Solidarité sur la Fortune (“Solidarity Wealth Tax”, the French wealth tax) during the last legislature (2002-2007), ISF yields had soared by 2006, jumping from €2.5 billion in 2002 to €3.6 billion.

Analysis of the economic consequences of this ISF wealth tax has raised the following conclusions:

- Tax collection costs remain low (around 1.6% of proceeds).

- Not raising the threshold in line with inflation between 1998 and 2004 created windfall revenues for the French State of €400 million in FY 2004 alone.

- ISF fraud mainly involving an under-assessment of property assets has stabilised over time at around 28% of total revenues, equivalent (had the legal framework remained unchanged) to a shortfall for the State of €700 million in 2004.

- Capital flight since the ISF wealth tax’s creation in 1988 amounts to ca. €200 billion.

- The ISF causes an annual fiscal shortfall of €7 billion, or about twice what it yields.

- The ISF wealth tax has probably reduced GDP growth by 0.2% per annum, or around 3.5 billion (roughly the same as it yields).

- In an open world, the ISF wealth tax impoverishes France, shifting the tax burden from wealthy taxpayers leaving the country onto other taxpayers.

Okay, this is a paper published in 2007. Given what I read, it seems to have been in English originally, and not French, but I could be incorrect.

A few items:

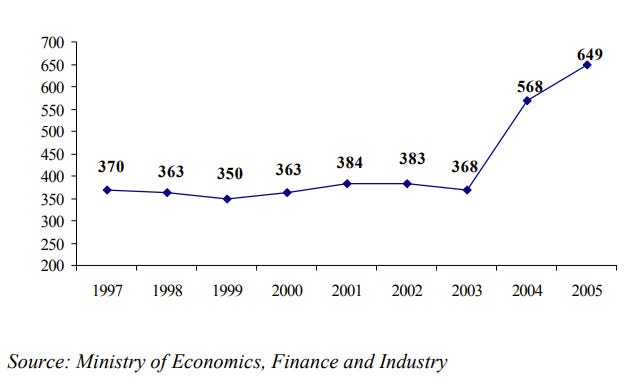

Estimated number of taxpayers and volume of capital to have left France since the ISF’s enactment in 1988.

The Conclusion section was a fun read:

“The shortest mistakes are always the best.” MOLIERE, L’Etourdi, IV, 3.

Following this analysis, we will have learnt a few noteworthy lessons about the ISF wealth tax’ main faults.

The ISF’s much higher proceeds over the course of the past French legislature mainly translate rising property values since 1998 and are a consequence of the tax’s threshold not being index-linked over the period 1998-2004. One result is that a further 100,000 taxpayers now find themselves in the lower two brackets. Another is that the average tax levied has dropped. We may have to reject politicians’ occasional argument that the ISF wealth tax suffers from high collection costs (in reality, these are very reasonable at below 2%) but a detailed analysis of the ISF’s structure confirms that the strong concentration of taxpayers in the upper two brackets constitutes a strong fiscal incentive to leave France when one’s estate exceeds €10 million (a point at which the annual ISF wealth tax bill is around €100,000 euros, tantamount to a gross annual salary of €200,000 euros) and especially €15 million (with taxable holdings of €15 million, the annual levy is ca. €200,000, equivalent to gross annual wages of €400,000).

According to our estimates, the Ministry of Economics has very largely under-estimated the capital flight caused by this (I)ncentive to (S)cram from (F)rance. In all likelihood, something like €200 billion has already left the country. This means that the Treasury is losing ca. €7 billion annually or around twice total ISF proceeds. In addition, in terms of investment, job creation and consumption, the French economy is suffering losses that are hard to estimate but very certainly exceed the direct fiscal shortfall, substantiating ex-Prime Minister Raymond Barre’s statement that the ISF is like an economic leukaemia for France.

This symbolic, mythical and expiatory ISF wealth tax – accepted by 98% of the population, basically by people who do not pay it, complicates the life of small taxpayers because it creates the flight of large estates. The fact that it costs more than it yields engenders a paradoxical situation in which all of France’s other taxpayers, including its least wealthy citizens, must bear the brunt of its overall tax burden, notably by paying more in VAT.

The outcome of the next presidential and legislative elections is likely to have no effect on the alchemy of this tax and the strange potlatch in which our fellow citizens engage every 15 June will continue to produce its inevitable side effects. The tax exodus will continue, adding year in year out to the burden of France’s least affluent taxpayers, who will have to compensate for the absence of wealthier expatriates - the sad reality of an (I)diotic and (S)tupid (F)rench tax that other countries view with a hint of pity and a great deal of incomprehension.

The wealth tax in France was repealed in 2018:

WSJ, July 2024: France Rolls Out the Wealth-Tax Guillotine [emphasis added]

Never mind that France has already tried a wealth tax, most recently beginning in 1989. The threshold and rates varied by year, but at its worst it taxed wealth above €10 million at 1.5%. The gimmick was what one might call, in French, un failure.

The promised revenue never materialized. At most the tax raised 0.2% of GDP in any one year, says Cristina Enache of the Tax Foundation. Capital, talent and entrepreneurs left instead of paying it.

Between 2000 and 2014, France lost some 42,000 people with net assets of $1 million or more, according to New World Wealth, a South African global wealth-intelligence firm. The French economist Éric Pichet reported that between the wealth tax’s passage in 1988 and 2007 capital flight amounted to some €200 billion. Entrepreneurs were stung especially by the law’s treatment of paper gains and losses, which could leave them paying a wealth tax on holdings in their own companies after those stakes lost market value. It was safer to leave and start companies elsewhere.

There was a time not so long ago when Paris admitted this. Mr. Macron abolished the wealth tax in 2018, only partially replacing it with a complex real-estate tax. Between 2018 and 2021, an average of 370 people who would have been subject to the old wealth tax returned to France each year and 260 left. Between 2011 and 2016, some 950 of these wealthy individuals had left each year and only 370 moved in, according to France Stratégie, a government-funded policy advisory.

So, they lost a lot of wealthy people, and only a pittance came back after they got rid of their wealth tax. France is one of the highest-taxed countries in Europe (and it needs to be, what with their super-low retirement ages).

I guess the good thing about their failed wealth tax of the 20th century was that at least they had moved on from direct confiscation and decapitation. I suppose they learned some manners in a few centuries.