Social Security: Benefit Terminations and the Trust Fund Running out

The extra deaths didn't "help"

For this Labor Day, let me check out the latest Social Security news.

I will get to the “news” item in a moment — that is, the bit everybody covers in their annual bits on the Social Security Trustees Report.

There’s a statistical supplement that accompanies this report, and I’d like to share some graphs with you. They have downloadable spreadsheets right there on the page, so I have tables and tables of numbers, but it’s easy to see these trends. I have annual data going back to 1950 (it’s a bit muddier before that).

Increase in benefit terminations of retired workers

aka death (mostly)

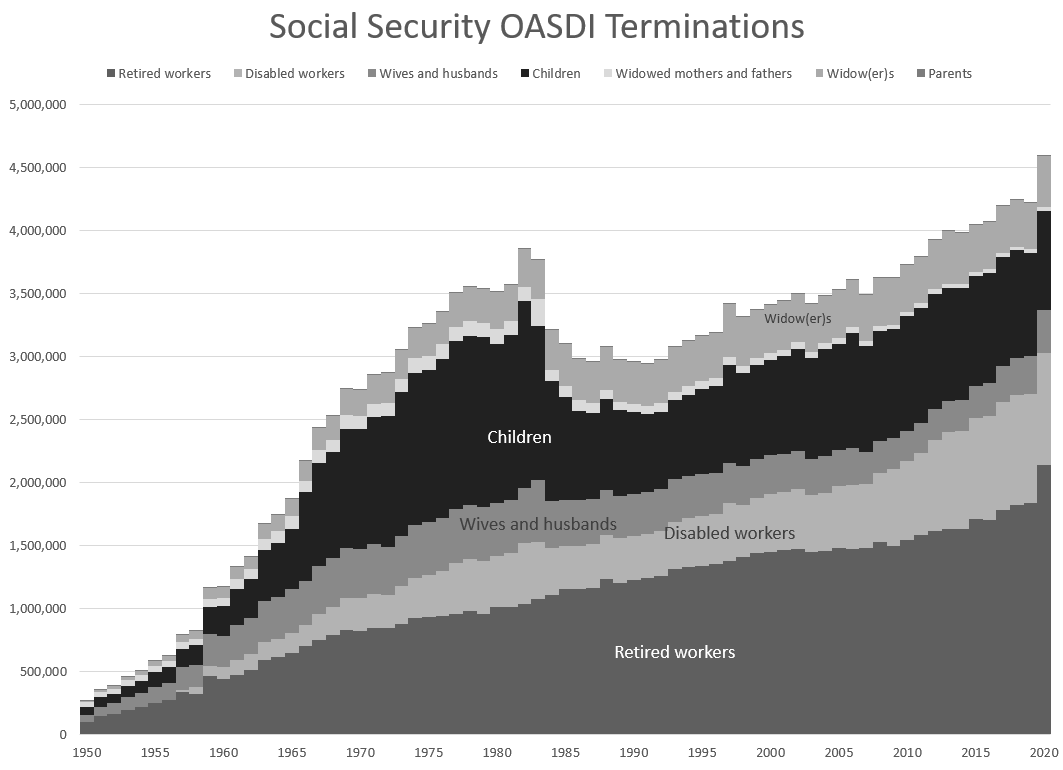

Terminations stats: OASDI Benefits Terminated — OASDI stands for old-age, survivors, and disability insurance.

This is by number of people, not benefit amounts. This covers not only the old-age portion of Social Security, but also Disability benefits (before full retirement age), and you can get disability benefit terminations because you achieve full retirement age and then get switched over to the old-age benefits.

So the plot doesn’t look quite right:

Something was up in 1979/1980, which I wonder about.

There are multiple types of components, so let me show you the same graph by component:

Now we can see that “anomaly” in 1979/1980 is related to child benefits. That particular trend could have a bunch of different causes… I have personal experience with the child benefit, as my dad died when I was 16. I didn’t get the benefits for very long (it stopped when I hit age 18), and besides, they went to my mother.

What we really want to look at is the increase in terminations of retired workers… because that’s usually because they died. It was 97% of the reason for retired worker terminations in 2020.

That’s quite a step up in 2020.

Here are the percentage changes, year-over-year for retired workers:

It seems to me the pre-1960 large changes probably relates to the ramping up of Social Security, as various things were a bit bumpy in the early years.

Since 1993, the termination changes have been less than 5%. Until 2020.

The 17% increase in terminations is close to the 17% excess mortality we saw in the U.S. in 2020.

So that’s that set of graphs. There will be more at the end of this post, but let us turn to the “news” right now.

When will the Social Security Trust Fund run out?

Within 15 years.

No, not enough people among the retired (and disabled) died last year to make up for the reduced income via payroll taxes.

That “news” ran recently in multiple places. I will pull a couple items.

WSJ editorial: The Entitlement State’s Bankruptcy Dates

We interrupt the campaign to pass new entitlements with news that the existing programs will soon go broke. That’s the word from the annual Social Security and Medicare Trustees reports released Tuesday.

Don’t shoot the messenger, but the Trustees project that the Medicare hospital trust fund will run dry in 2026. The two Social Security trust funds for disabled individuals and seniors won’t be exhausted until 2034, and let’s hope Congress’s retirement benefits will be among the first to be cut.

Most in the political class won’t even mention the problem. When the trust funds become insolvent, the government will have to sustain the entitlements by tapping general revenue. This will squeeze defense and discretionary programs even as taxes soar.

The editorial mostly focuses on Medicare, and the attempt to add even more benefits to the program, and extending the program to more people.

I ran this editorial first, as opposed to the more standard news coverage, because I wanted to address the “Reality” of the Trust Fund. As I have said to fellow finance folks, the Trust Fund is like writing an IOU to yourself when you spend money on item A, when you need to cover purchase B later. It is a fraud.

But what it really is, more than anything else, is a political tool. Through the mechanism of the Trust Fund, Congress can put off having to act on the fundamental demographic problem that they can’t do much about. They hope they can run the Magic Money Machine to cover all the goodies they want, and in 2034, the Boomers will mostly be over age 80. Maybe another pandemic will deal with them….

(and nobody cares about us Gen Xers. In 2034, I won’t even be eligible for Social Security old age benefits.)

Nobody expects the Social Security benefits to be cut in 2034, or whatever other magic date when the Trust Fund runs out. The only thing the current Trust Fund mechanism requires is cuts… only if Congress doesn’t actually pass legislation to “fix” the issue.

They have been doing ad hoc “fixes” to Medicare and other parts for years so as to avoid massive cuts.

Given current Congressional behavior, I assume half-assed ad hockery in the early 2030s. So I have that fun to look forward to.

More coverage of the Social Security Trustees report

Additional coverage:

Elizabeth Bauer at Forbes: More Than An Insolvency Date: What Else To Know About The Social Security And Medicare Trustees’ Reports

This year, Social Security’s deficit is unusually high due to lower revenues and higher benefits: 1.75%. In 2040, the deficit climbs to 3.70% rather than 3.54%. In 2080, the deficit stands at 4.87% rather than 4.59%.

Put another way, if there were no Trust Fund accounting mechanism now, the OASI program would have been able to pay 93% of benefits. This would drop to 76% in 2035 – 2040 – 2045, then drop further to being able to pay 70% of benefits.

…..

Also consider that, at the moment, there are 2.7 workers for each Social Security recipient (2.8 in 2020). This is forecast to drop to 2.2 in 2040 and ultimately down to 2.1. But if the population trends are those of the pessimistic scenario, then that 2.1 would drop to 1.5 by the year 2080.

Well, I’d be over 100 years old by then (if still alive). I do not assume Social Security will be in the same form by then. There are loads of changes that could happen, depending on changes in longevity, fertility, and morbidity.

The Social Security trust fund most Americans rely on for their retirement will run out of money in 12 years, one year sooner than expected, according to an annual government report published Tuesday.

The outlook, aggravated by the Covid pandemic, also threatens to shrink retirement payments and increase health-care costs for older Americans.

….

Senior administration officials said in a press briefing Tuesday afternoon that a spike in deaths among retirement-age Americans in 2020 helped keep the programs’ costs lower than projected. They added that the ultimate, long-term impact of the coronavirus is less clear as costs and revenues return to their extended forecasts.

…..

But the future of that model is now in the middle of a slow-moving crisis: Within the past two years, the program has started to draw down its assets in order to pay retirees all benefits promised.In other words, Social Security’s costs in the form of monthly payments to retirees now exceed the income it takes in from U.S. workers. Projected to soon consistently operate in the red, the program’s reserve fund would be depleted around 2033.

Yup, the OASDI Trust Fund is very close to “topping out”.

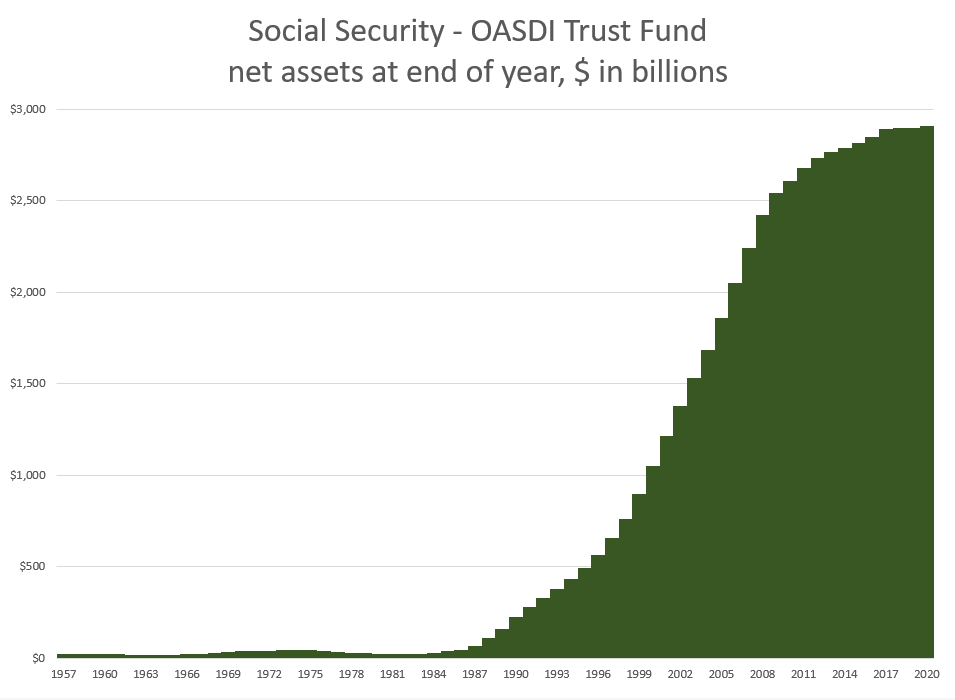

Graph of the OASDI Trust Fund

The status of the OASDI (old-age, survivors, and disability insurance) Trust Fund can be seen in table 4.A.3 from the data supplement, and you can also see the data here.

Here’s the plot:

You can see that the OASDI Trust Fund has barely been increasing for many years now.

But don’t try to eyeball that – let’s look at the year-over-year percentage changes:

The big spike in the early 1980s is related to not only a big spike of boomers hitting the workforce then, but also an increase in FICA taxes. There was comprehensive legislation passed in 1983 that made multiple changes, such as taxation of Social Security benefits (under certain conditions). During the Clinton administration, changes were made to increase the full retirement age, so that most Boomers have an FRA of 66 years old (approximately), and post-Boomer people have an FRA of 67 years old (as opposed to the old FRA of 65). Benefits are reduced if you start old-age benefits before your FRA.

We break into this post for an update

CORRECTION: The FRA increase was in the 1983 amendments. From the Social Security Administration:

SUMMARY of

P.L. 98-21, (H.R. 1900)

Social Security Amendments of 1983-Signed on April 20, 1983

…..

Raises the age of eligibility for unreduced retirement benefits in two stages to 67 by the year 2027. Workers born in 1938 will be the first group affected by the gradual increase. Benefits will still be available at age 62, but with greater reduction.

Thanks to Marc Joffe of the Reason Foundation for correcting me!

There were reforms in the 1990s, but they weren’t as far-reaching as the 1983 one.

Back to your original programming

But there haven’t been any substantive changes in Social Security benefits or taxes since the 1990s, and the peak Boomer birth years of the late 1950s (specifically 1957/1958) are eligible to take old-age benefits in 2021. The oldest boomers hit age 62 in 2008.

2008 was when the over-5% growth rate of the Trust Fund stopped.

Pretty soon, the growth rate will be negative for every year until the Fund is fully depleted. That means more benefits will be going out compared to the taxes and interest payments coming in. That will strain the federal budget well before the Trust Fund fully runs out, because General Fund cash has to cover the “bond” redemptions in the Trust Fund as it cashes out. It has already been a problem.

That said, I have no expectation that the current Congress will do anything, and if Republicans take over the House (and maybe the Senate) in 2023, expect even more nothing. Maybe we’ll have to wait for the next Presidential election before this is dealt with at all.

Prior posts on Social Security

In no particular order:

June 2018: Social Security and Medicare Trust Funds – What’s Real? – lots of graphs!

July 2017: Social Security: The Annual Trustee Report – Cash Flows, Tardiness, and Other Views – more graphs! [I like graphs]

May 2018: A Modest Social Security Proposal – spoiler: move the minimum eligibility age up from 62 to 65.

January 2017: Actuaries on Social Security: Bruce Schobel on Reforms, Robert Myers on History, and Richard Foster on Medicare/ACA