I’m not even being sarcastic, being a life-annuity actuary.

The Bobby Bonilla deal shows the value of annuities, even if only an annuity-certain. (That is, an annuity that pays out for a fixed number of years, no matter if you’re alive or dead.)

That said, there is so much more to the story than annuities — it has:

Bernie Madoff

too-high discount rates in valuation

less-than-optimal behavior in trying to avoid a “tax”

credit risk

deferred wages

principal-agent alignment (YAY!)

Seriously, congrats to Bobby and his agent, who negotiated the deal.

I have only 10 more years of these (and then it will be retrospectives), so let me enjoy this while I can!

Newest Bonilla Coverage!

The people who waited until July 1 to publish are out of luck, because I have to compose ahead of time (like most professionals).

Bobby Bonilla’s name resonates in the sportscard hobby not only for his on-field accomplishments but also for his financial legacy, making him one of baseball’s most talked-about players on and off the field. As a six-time All-Star and key contributor to the Pittsburgh Pirates and New York Mets, Bonilla was one of the premier hitters of his era.

His impact on the hobby, however, extends beyond his playing days due to his infamous contract deferment, which continues to spark collector interest every July 1st, now widely and infamously known as "Bobby Bonilla Day."

[Where’s the Pope’s card?]

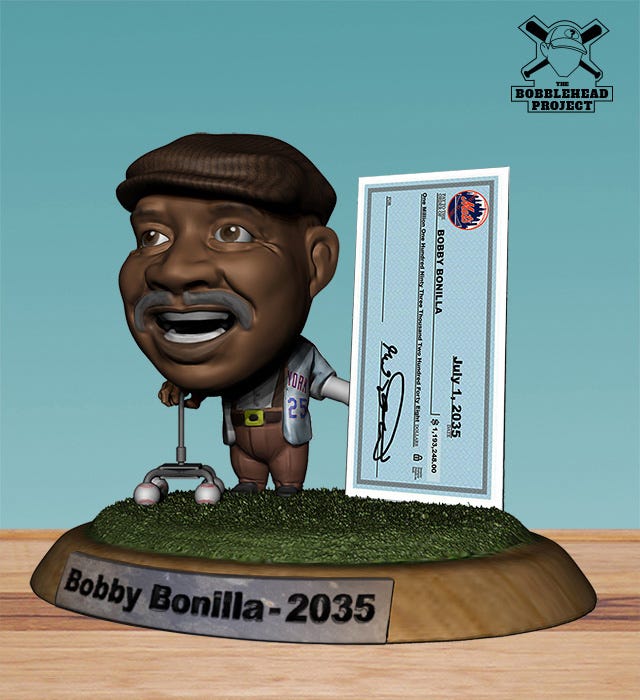

Beyond his rookie cards, Bonilla’s long-term hobby relevance is fueled by "Bobby Bonilla Day," the result of a deferred contract with the Mets that ensures he receives a $1.19 million payment every July 1st from 2011 to 2035. This financial anomaly has turned Bonilla into a pop-culture figure, with collectors often revisiting his cards during this annual event. The contract has kept his name in discussions long after his retirement, cementing his place in baseball history and keeping demand for his memorabilia market quite steady over those years.

Look, I’m not even into baseball. My sport is sumo. But I am into finance.

Perhaps Bonilla's most famous financial decision came in 2000 with the New York Mets. Rather than accepting an immediate $5.9 million payment, he negotiated a deferred payment plan. This arrangement, now celebrated as "Bobby Bonilla Day," sees the Mets paying him $1,193,248.20 annually from July 1, 2011, through 2035. When the contract concludes, Bonilla will have received a total of $29.8 million.

Why did the Mets agree to this deal?

At the time, the team’s owners believed they were making big money by investing in Bernie Madoff (yes, that Bernie Madoff). The Mets bet that they’d out-earn the interest. Things didn’t quite work out.

So is this a win for the little guy, a loss for billionaire owners, or just a brilliant money move? Either way, it’s one of sports history's best personal finance plays.

It’s why “Bobby Bonilla Day explained” becomes a trending search every summer.

It’s why social media lights up with jokes, memes and admiration.

The long-retired Bobby Bonilla gets paid more annually than many active players.

Again, the deal made sense IF AND ONLY IF you thought you could make a guaranteed 8% for every year through the deal.

I calculated the present value of the payments against what was left in his contract, and it was equivalent to 8% valuation. I did that back in 2016.

Back to the Canadian article:

That was record-breaking then, but it’s pocket change next to today’s megadeals.

Shohei Ohtani signed a 10-year, $700 million contract with the Los Angeles Dodgers in 2023. A whopping $680 million of the contract is deferred. While Ohtani gets $2 million annually until 2033, it’s in 2034 where he’ll collect $68 million per year until 2043.

Juan Soto signed another record-breaking contract in 2024 with none other than the New York Mets (some people never learn) for $765 million over 15 years. There is no deferred money. Soto gets his money up front (including a signing bonus of $75 million.

Vladimir Guerrero Jr. signed a 14-year, $500 million extension with the Toronto Blue Jays in 2025 with no deferral.

There are two financial takeaways for everyday Canadians: Deferring income can provide long-term financial security, and the importance of negotiating your salary upfront.

So not all of these are deferred annuities.

As in… only Ohtani is doing a deferred deal, but it’s not a retirement deal.

(and the author tried to hook in totally irrelevant stuff that no longer is helpful in today’s economic environment.)

Guaranteed interest rates are valuable in retirement

I found another similar “power of compound interest” article, but the problem is, few people can find a guaranteed 8% compound interest over 35 years.

In my 2023 post on Bobby Bonilla Day, I looked over the deferred contracts, and I think Bruce Sutter got the best interest rate of the ones I could find:

Though not listed, I believe the best actual guaranteed interest rate was that of Bruce Sutter, which he got in a deal with the Atlanta Braves. The interest rate was 12.3% over a 35/36-year period. Guaranteed.

This is the last year [2022] the Braves pay Bruce Sutter for his 1988 contract.

Bruce Sutter may be the closest to Bobby Bonilla in terms of the number of deferred payments that he's received. In 1984, Sutter signed a six-year contract that paid him $4.8 million. His Braves tenure was highlighted by injuries. Sutter annually receives $1.12 million from the Atlanta Braves and will continue to receive payments until 2022. The payments began in 1991, which means that Sutter has been receiving deferred payments for 30 years. In addition, the Braves will also have to pay Sutter one final check for $9.1 million when the deferred payments stop. It's pretty impressive that Sutter is receiving more than $10 million a whopping 35 years after he announced his retirement.

As I pointed out in my 2021 post on Bobby Bonilla Day, what makes the guarantee particularly valuable isn’t that Bonilla is getting over $1 million per year, it’s that the guaranteed interest rate is well over a “risk free” rate in the year he settled.

So what is the appropriate comparison?

Well, I don’t have any 35-year interest rates, but I do have 30-year interest rates. Those are “guaranteed” (about as guaranteed as you’re going to get), and that might be an appropriate comparison.

The appropriate date on which to make the comparison of this annuity deal was July 1, 2000. The present value at 8% was $5.9 million. But if the valuation rate appropriate to value the deal was 5.90%, the present value was $8.7 million.

Using a proper valuation rate, Bobby Bonilla’s agent negotiated almost 50% higher than what the original contract was worth.

The payment they should be comparing against is $811,016, which is the payment Bobby Bonilla would have gotten if the annuity had been valued at 5.90% instead of 8%. That would have been a payment 32% lower than what he’s actually getting.

So huzzah for Bobby Bonilla and his agent!

He really got a valuable deal.

A Pause for Ohtani

For both Bobby Bonilla and the Mets, the deal was seen as win-win.

(The Mets were incorrect on their side — part of the reason they thought 8% was cheap was they were investing with Bernie Madoff, and thought they could make a guaranteed 12% return… and they were wrong about that.)

Shohei Ohtani made a deferred deal, with eye-popping numbers, and the structure is being done to avoid league “tax” (as well as regular taxes).

On Monday, we learned what those deferrals entail. Per The Athletic's Fabian Ardaya, Ohtani is deferring all but $2 million per year of his $70 million average annual salary until the contract's conclusion in 2034. That means he won't see $680 million of the salary for more than a decade.

Per the report, the deferred portion of the contract will be paid to Ohtani without interest from 2034 to 2043. The deferrals were reportedly Ohtani's idea. The Dodgers officially announced the signing on Monday, but not the terms.

The payment deferrals will free the Dodgers to spend more around Ohtani as they seek to build a perennial championship contender with the two-way superstar. Per the report, the contract with the deferrals will count for roughly $46 million annually for competitive balance tax (CBT) purposes. The CBT — like the NBA's luxury tax — is a financial penalty for teams that spend above an agreed upon ceiling in any given season. It wasn't immediately clear how that $46 million figure was reached.

STUMP - Meep on public finance, pensions, mortality and more is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Honestly, if I'd been the Braves, I would have had Phil Niekro teach Sutter the knuckleball so they could at least put him out there every fifth day until he was 45.

Honestly, if I'd been the Braves, I would have had Phil Niekro teach Sutter the knuckleball so they could at least put him out there every fifth day until he was 45.