Taxing Tuesday: Commentary Round-Up on the One Big Beautiful Bill

Something is getting worked out... but what, exactly, is in there?

We’ve got comments coming out on the various bits of the tax bill coming together… mainly on the recent releases from House Republicans in the Ways & Means Committee.

So let’s just grab a few!

Tax Those Endowments!

National Review, 13 May 2025: House GOP Tax Plan Includes Major Hikes to Elite University Endowments

House Republicans are proposing major tax hikes for the wealthiest U.S. universities as part of a new bill released Monday to extend President Trump’s 2017 tax cuts.

Under the proposal, private colleges and universities with at least 500 students and endowments of more than $2 million per student would pay an increased tax rate of 21 percent on net investment income – a major increase from the current 1.4 percent rate.

DAAAAANG

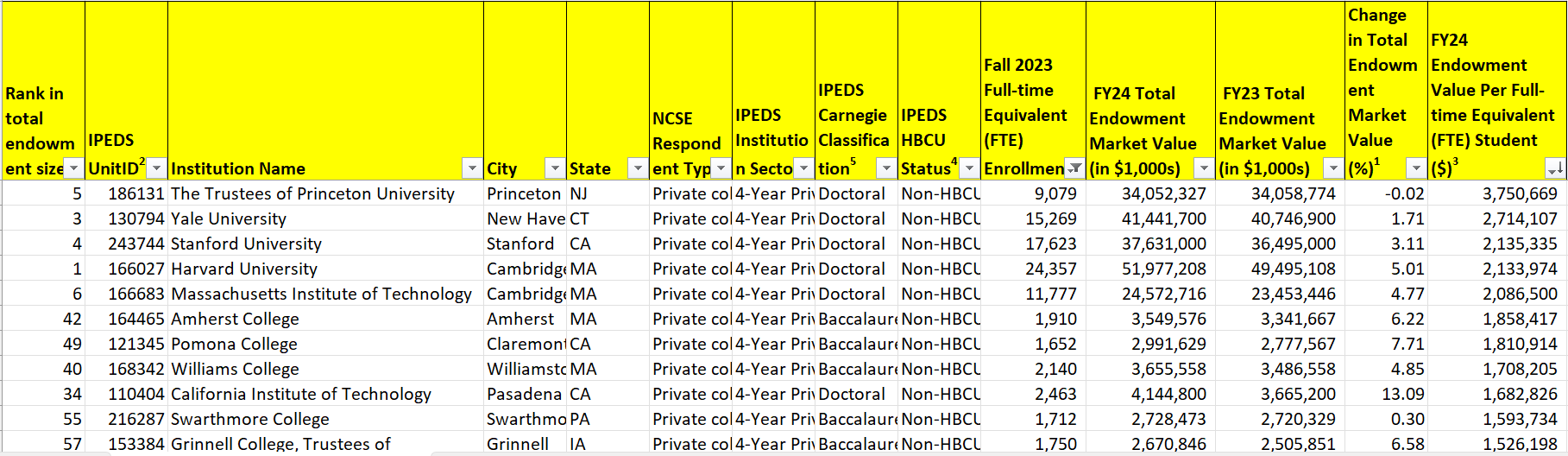

The public data available here: 2024 NACUBO-Commonfund Study of Endowments (NCSE) Results, using the above items (> 500 students), here are the top endowment ratios:

Only five (using only full-time equivalent enrollment) institutions would be affected: Princeton, Yale, Stanford, Harvard, and MIT.

The next tier down is within spitting distance.

To be sure, many universities aren’t in the above survey. I believe Notre Dame is missing.

We all know this is for spite, and will not generate much in the way of revenue. If it sticks, it may also spur those sitting on the top of the pile to spend down their endowments (hahaha, yeah, right.)

More comments:

6 May 2025, AP: As Trump battles elite colleges, House GOP looks to hike endowment tax by at least tenfold

13 May 2025, P&I: MIT, Yale face endowment tax hike while Notre Dame scores break

Details in Changes from “baseline”

I recommend the following post going over many of the changes in the bill:

There’s some modest progress: many of the most egregious green energy subsidies are rolled back, and new safeguards are added to some individual credits. And, at least for now, the worst proposed tax hikes have been avoided.

The Joint Committee on Taxation (JCT) estimates the bill will reduce revenue by $3.27 trillion, coming in under their target of between $4 trillion and $4.5 trillion. This additional fiscal space should be used to improve the bill’s pro-growth provisions and not to buy votes for additional special interest subsidies. Section-by-section summary from JCT here.

I will pull out only a few items that I consider the ones individuals may pay attention to.

Pro-growth changes

Policies that permanently lower the effective tax rate on businesses, investments, and work are the biggest drivers of long-term growth. The bill makes many provisions permanent, but lets the most important business expensing changes expire. The bill could be improved by making the temporary provisions permanent.

….

The TCJA personal rates and bracket structure are permanent. Adds an additional year of inflation adjustment in 2026 for all but the 37 percent bracket, effectively taxing more of Americans’ income at lower rates.

Permanently raises estate tax exemption to $15 million per person (up from $14 million in 2025).

….

New and expanded tax preferences

The bill includes at least 20 new or expanded tax preferences, many only for four years. Each one entails fiscal costs, adds complexity, opens new avenues for tax avoidance, and delivers little in the way of long-term growth. Each of these should be dropped, scaled back, or entirely repealed.

….

Raises individual SALT cap to $30k and phases down to $10k above $400k/$200k. Cracks down on state workarounds for some passthroughs.

The $2,000 child tax credit is permanent. Temporarily increases the credit by $500, to $2,500 beginning in 2025, through 2028; after which point the base credit is indexed for inflation. Requires a Social Security number for the child and both parents, if filing jointly.

….

The larger standard deduction is permanent. Adds a temporary $2,000 ($1,000 single) increase in the standard deduction, starting in 2025, through 2028. Permanently repeals the personal and dependent exemptions.

Base-broadening and subsidy elimination

The bill makes modest reforms to existing subsidy programs and repeals many of the Inflation Reduction Act's green energy tax credits. The bill could be improved by adding more tax preferences to this list.

….

Makes permanent TCJA’s $750,000 limit on mortgage interest deduction, and other smaller itemized deduction changes.

Adds new overall limit on itemized deductions for those in the top tax bracket, capping the rate at which you can make itemized deductions at 35%. Overall limits add complexity, but this improves the previous Pease limit.

….

Social Security Number requirement for higher-ed tax credits, Lifetime Learning and American Opportunity Credits.

….

New EITC system to certify eligible children before they can be claimed, to reduce errors and fraud.

Limits Medicare eligibility to US citizens, green card holders, and other specified categories.

Anti-growth tax increases

The bill mostly avoids the most damaging tax increases that could have been included, like raising the corporate tax or increasing the top income tax rate.

….

Other

The bill covers many other issues across more than 400 pages. Not summarized here are many changes to the tax treatment of health care through HSA expansions and other changes. The following reforms also strengthen the bill.

….

Returns 1099K reporting thresholds to $20k or 200 transactions. Current law was an unworkable $600 that the IRS had repeatedly delayed.

Raises 1099-MISC reporting threshold from $600 to $2,000 (indexed).

I skipped over a lot. Go to the post to see the complete list.

In some of these cases, such as requirements for SSNs to identify certain individuals for claiming particular tax benefits, etc., I didn’t realize those weren’t already required. Hmmm.

As for EITC (earned income tax credit), I was well aware that this was involved in some of the high audit rates involving low-income people.

Every so often, somebody tries to make hay out of this, in terms of “Why is the IRS auditing all these poor people instead of rich people?!” Because there is a lot of fraud in EITC, that’s why.

Or maybe it’s just errors from confusion.

The EITC has a high rate of improper payments caused by math errors, fraud, and misunderstanding of the rules. The Government Accountability Office reports that the EITC error and fraud rate averaged 24 percent between 2016 and 2020, or about $16 billion a year.

24 percent “error” rate is high.

The EITC is an easy target for dishonest filers because it is refundable, meaning that people can simply file false tax returns and wait for the U.S. Treasury Department to send them a check.

Those are quotes from Cato. What does the IRS say?

IRS estimates that around 33 percent of EITC claims are paid in error. Some of the errors are unintentional caused by the complexity of the law, but some of the claims are intentional disregard of the law.

Their estimate is higher.

This is from a page intended to dissuade tax professionals from contributing to EITC fraud.

On SALT Cap - Underwhelming Adjustment

So, a higher SALT cap, but the bolded above is overselling what the SALT cap would be. We will see what it actually is below, in a NY Post piece.

Let’s see what my representative, Mike Lawler, had to say with other NY Republican representatives:

8 May 2025: Joint Statement from New York Reps. Mike Lawler, Elise Stefanik, Andrew Garbarino, and Nick Lalota on Proposed SALT Cap Deduction

Congressman Mike Lawler (NY-17) today joined Reps. Elise Stefanik (NY-21), Andrew Garbarino (NY-02), and Nick LaLota (NY-01) issued the following joint statement in response to the House Ways and Means Committee’s proposed $30,000 cap on State and Local Tax (SALT) deductions:

"We’ve negotiated in good faith on SALT from the start, fighting for the taxpayers we represent in New York.

Yet with no notice or agreement, the Speaker and the House Ways and Means Committee unilaterally proposed a flat $30,000 SALT cap – an amount they already knew would fall short of earning our support.It’s not just insulting – it risks derailing President Trump’s One Big Beautiful Bill.

They put that statement out a week before the official release… so, now what?

12 May 2025, NY Post: House tax plan triples SALT deduction cap to $30K — but New York GOPers say it’s not enough

House Republicans are planning to triple the state and local tax (SALT) deduction cap to $30,000 in their plan to pass President Trump’s “big, beautiful” agenda bill, despite New York Republican lawmakers calling that figure woefully insufficient.

A draft circulated by the House Ways and Means Committee and seen by The Post Monday would raise the current $10,000 SALT cap to $30,000 on individuals with taxable annual income of $400,000 or fewer.

For married individuals who are filing separately and have taxable income of $200,000 or fewer, the SALT cap would only increase to $15,000.

SALT allows taxpayers to deduct the cost of their state income taxes, property taxes and other local taxes from their federal returns.

Last week, four New York Republicans bashed a proposed $30,000 SALT deduction figure as “insulting.”

….

Without further action from Congress, the $10,000 SALT cap is set to expire after 2025, alongside key tax cuts from the 2017 law.

The SALT cap disproportionately impacted blue states with higher taxes and prompted some Republicans, such as Stefanik, to vote against the measure at the time.

….

“This is awful. It’s a direct contradiction of the President’s September 17th campaign promise on Long Island to ‘get SALT back,'” Long Island Rep. Tom Suozzi (D-NY) said Monday in response to the GOP plan.

Tax Foundation put an updated map today on per capita SALT:

It should surprise nobody that New York is #1.

(We’re number 1! We’re number 1!)

So yes, the New York politicians are very motivated to remove the SALT cap entirely. The above is per capita, and not per household.

I don’t think this is finished.

Other Tax Bill Commentary

12 May 2025, Eide Bailly Tax News & Views: Tax News & Views Miles to Go On The Way to a Tax Bill Roundup

13 May 2025, Eide Bailly Tax News & Views: Tax News & Views Big Beautiful Bill and Bulb Roundup

11 May 2025, Liberty Taxed: A Blog on US Tax Policy: Tax Tracker | Your Guide to this Week’s Tax Markup

12 May 2025, MishTalk: The “One Big Beautiful Bill” Will Continue Spending at Biden’s Level

12 May 2025, Washington Examiner, Scott Hodge: A debt-financed tax bill risks fueling inflation and the national debt

12 May 2025, The Hill, David McIntosh: Extend Trump’s tax cuts, pay for it by repealing Biden’s climate handouts

13 May 2025, Tax Foundation: “Big Beautiful Bill” House GOP Tax Plan: Preliminary Details and Analysis