Read the News with Meep: Vatican Credit Bets, Trump Taxes, Houston Pension Governance, and More!

Look over my shoulder...

This one is a real grab-bag of fun.

For certain definitions of “fun”. [Reminder: I check mortality trends for my own interest.]

The Vatican Bet on a Company’s Failure!

The Vatican invested in risky derivatives on Hertz using donated funds, a report says

The Vatican used charitable proceeds to buy derivatives that bet on the creditworthiness of car-rental firm Hertz, the Financial Times reported Thursday. [October 8, 2020]

According to a document seen by the FT, part of the Vatican’s $621 million portfolio was used to buy credit default swaps, which offered protection against Hertz defaulting on its debts by April 2020.

Investment took place under Cardinal Giovanni Angelo Becciu, three years before Hertz filed for bankruptcy in May.

Pope Francis criticized CDS in May 2018, calling them “unethical.”

Let me stop right there. Pope Francis has said a lot of things about capitalism and finance…. usually exposing his very deep ignorance of the subjects.

(I am a Catholic, and yes, I believe all the “crazy” stuff. I’ll say a rosary for you.)

The Pope is infallible only speaking ex cathedra, and he also has a lot of authority when it comes to Catholic teaching about all sorts of things. But money is not one of the things current Popes have known much about. Back in the Medici Pope days, sure, they knew all about war, finance, and global politics — they controlled areas directly. But all they’ve got is teeny Vatican City now, and even the laypeople don’t really listen to them.

Back to the piece:

CDS are complex instruments that can inflict huge losses on their holders if a trade goes wrong. In this case, the Vatican had a narrow escape, because Hertz filed for insolvency in May, meaning the Holy See’s investment was paid out in full.

….

Pope Francis criticized CDS in May 2018, calling them unethical, because they enabled buyers and sellers to “gamble on the failure of others, calling them a “time-ticking bomb.”According to the FT, the Vatican made the investment three years ago, under the watch of Cardinal Giovanni Angelo Becciu, a senior clergyman who resigned last month after being implicated in an investigation involving a Vatican investment in a London real estate deal.

Becciu has denied all allegations and the Holy See’s prosecutor has opened an investigation into several church officials, but Becciu has not been charged with any crime by the Vatican.

Ah, but that’s not the really juicy part of all of this.

Cardinal Pell of Australia was a person investigating Vatican money matters. Pell was then accused of sexual abuse, convicted, and then acquitted. I’m not going through the whole thing, but the Pell situation was a complete set-up.

Was Becciu behind that, to try to avoid his own investigation into financial corruption? Of course, it could all be a coincidence. That does happen.

Items on that gossip:

Speaking as a Catholic who has donated to not only my local parish, but also my archdiocese (New York), and global Catholic concerns (Catholic Relief Services), I have a simple question: why are any clergy running church finances? There’s a reason each parish is supposed to have a lay finance council. (The reason: actual experience with priests absconding with church funds). Indeed, I am far more likely to suspect churchmen over money than any other shenanigans, except possibly alcoholism.

Given the even-swampier aspects of Vatican politics, I would be surprised if the Vatican tries Becciu on any financial shenanigans. I don’t even care if they do.

Historical interlude: moral attitudes toward life insurance

As for buying CDS, I don’t think they’re immoral, nor is short-selling. I could get into why, but that can wait for another time.

I do want to talk about when people thought life insurance was immoral. Here’s a great article from Virginia Postrel about that attitude:

The product was perfectly legal. Many prominent clergymen endorsed it, including celebrity preacher Henry Ward Beecher, brother of Uncle Tom’s Cabin author Harriet Beecher Stowe. The Pennsylvania House declared in 1811 that it “would be highly beneficial to many descriptions of citizens throughout the state.” The need was clear, and the businesses that sold it were untainted by scandal, bankruptcy, or fraud. They delivered what they promised.

But in the early 19th century, Americans just wouldn’t buy life insurance.

The problem wasn’t mere procrastination. Many people deemed the very idea immoral. “Has a man the right to make the continuance of his life the basis of a bargain? Is it not turning a very solemn thing into a mere commercial transaction?” wrote a typical critic. Religious traditionalists believed they should trust in God’s providence, not a financial contract, to care for their loved ones after death. Others, pointing to arson to collect fire insurance, worried that it might encourage murder.

One big booster was not only the formation of mutual insurers, in which the policyholders own the company, not shareholders [many of the largest life insurers are mutuals: Northwestern Mutual, MassMutual, New York Life, TIAA, and some of the biggest publicly-owned insurers used to be mutuals: MetLife, Prudential], but fraternal insurers. Fraternal insurers are based on an affinity group, and many started out of mutual aid societies.

The Knights of Columbus, which is an American Catholic men’s organization, is one such fraternal group with a life insurance component. Even though I work (well, worked) in Connecticut, I’ve yet to visit their HQ/place of founding in New Haven. K of C is the largest fraternal organization in the U.S.

As for the Pope, he should not rattle on about things he knows little about. If he’d like to understand CDS and insurance and finance better, then sure, someone can teach him about those (Heck, he should read The Wisdom of Finance – and so should you). But I think his time would be better spent in Eucharistic Adoration.

It’s not important that the Pope understands finance. Any more.

(Don’t sell indulgences!)

Coverage:

AP: Cardinal Pell accuser denies bribe as Vatican intrigue grows

A new Vatican scandal vindicates Cardinal Pell but frustrates Pope Francis

Cardinal Pell applauds pope’s actions against Cardinal Becciu

BBC: Cardinal Becciu: Vatican official forced out in rare resignation

Parolin: There is ‘no connection’ between Pell arrival, Becciu ouster

Cardinal Becciu claims ‘absolute falseness’ of allegations against him

I’ve heard that tune before. In looking up links for this story, I found items on the need to clean up Vatican finances going back about 20 years. Augean stables, anybody?

By the way, Today’s Mass reading is from the Gospel of Luke [Luke 12:39-48]:

[47] That servant who knew his master’s will

but did not make preparations nor act in accord with his will

shall be beaten severely;

[48] and the servant who was ignorant of his master’s will

but acted in a way deserving of a severe beating

shall be beaten only lightly.

Much will be required of the person entrusted with much,

and still more will be demanded of the person entrusted with more.”

The cardinals would do well to remember that. And remember why Dante placed so many cardinals and Popes in Inferno.

Trump’s tax returns

Well, it looks like the NY Times finally got around to publishing something more about Trump’s taxes after the original dump of nothing.

Trump Records Shed New Light on Chinese Business Pursuits

As he raises questions about his opponent’s standing with China, President Trump’s taxes reveal details about his own activities there, including a previously unknown bank account.

President Trump and his allies have tried to paint the Democratic nominee, Joseph R. Biden Jr., as soft on China, in part by pointing to his son’s business dealings there.

….

But Mr. Trump’s own business history is filled with overseas financial deals, and some have involved the Chinese state. He spent a decade unsuccessfully pursuing projects in China, operating an office there during his first run for president and forging a partnership with a major government-controlled company.

And? Has he been particularly soft on China?

And it turns out that China is one of only three foreign nations — the others are Britain and Ireland — where Mr. Trump maintains a bank account, according to an analysis of the president’s tax records, which were obtained by The New York Times. The foreign accounts do not show up on Mr. Trump’s public financial disclosures, where he must list personal assets, because they are held under corporate names. The identities of the financial institutions are not clear.

So, he has companies with bank accounts in other countries? Given that he has property in different countries, I don’t see how this is a surprise.

The Chinese account is controlled by Trump International Hotels Management L.L.C., which the tax records show paid $188,561 in taxes in China while pursuing licensing deals there from 2013 to 2015.

The tax records do not include details on how much money may have passed through the overseas accounts, though the Internal Revenue Service does require filers to report the portion of their income derived from other countries. The British and Irish accounts are held by companies that operate Mr. Trump’s golf courses in Scotland and Ireland, which regularly report millions of dollars in revenue from those countries. Trump International Hotels Management reported just a few thousand dollars from China.

In response to questions from The Times, Alan Garten, a lawyer for the Trump Organization, said the company had “opened an account with a Chinese bank having offices in the United States in order to pay the local taxes” associated with efforts to do business there. He said the company had opened the account after establishing an office in China “to explore the potential for hotel deals in Asia.”

I am really not seeing how any of this is even interesting.

This story seems pretty dead if this is the best that can be extracted from the documents illegally given to the NYT. Whichever person passed on the tax documents did not do the NYT much favors. For all I know, Trump himself had the docs funneled to the NYT (in which case, the docs were not illegally shared with the NYT).

One of the bits in there, about the sale of Ivanka/Jared’s condo to a Chinese-American businesswoman, was already known years ago. Maybe that’s iffy, but the tax returns don’t add any info to that transaction.

The sad take on Trump’s taxes

I had been holding onto this link for when the NYT dumped more info, because I thought they might have something substantive. Given that sad squib above, there’s no reason for me to hold on longer.

The following from The Atlantic was the usual take: Do Trump’s Taxes Show He’s a Failure, a Cheat, or a Criminal? – Atlantic staff writer Derek Thompson quotes only one potential tax expert, so that gives you an idea of the quality of the piece. Thompson is not a tax expert himself.

Brian Galle, a tax professor at Georgetown University, told me that my three explanations aren’t mutually exclusive. “There is a relationship between your interpretations one, two, and three,” he said. “If you’re a naturally successful businessperson, there is less pressure to maintain your wealth with tax-evasive maneuvers, or to engage in full-fledged money laundering.”

Most of the outright business fraud stories out there started with a successful business (Enron, Bernie Madoff) that could not maintain “wins” indefinitely. So they turned to all sorts of shenanigans.

Trump’s tax records are a clue, not a complete answer. Their incompleteness might be the most concerning thing about them. “As a citizen, my reaction to the Times report is: The president owes a ton of money, and we don’t know who he owes it to,” Galle said. “Many of his creditors are effectively shells, and it’s opaque who the parties and interests are. Maybe there shouldn’t be a freak-out, because he owes it all to Deutsche Bank. And they’ve never been involved in money laundering, right? Oh, that’s right.”

The “that’s right” links to Deutsche Bank faces action over $20bn Russian money-laundering scheme, which is from April 2019.

Maybe Trump is involved in money laundering. But having a bunch of interacting transactions like this is not that unusual. One may question whether these complicated arrangements should exist at all, but one may have issues with modern finance in general.

Houston Pension Governance

P&I: Texas judge rules change to Houston fire plan assumptions is unconstitutional

A Texas district judge ruled Wednesday that legislation that includes lower rate of return assumptions affecting the $4.2 billion Houston Firefighters’ Relief and Retirement Fund is unconstitutional.

Harris County Judge Beau Harris ruled in favor of the pension fund in its lawsuit against the city of Houston and officials including Mayor Sylvester Turner, saying its board has “exclusive authority to select an actuary and determine sound actuarial assumptions,” according to the court filing.

The pension fund originally filed the lawsuit in July 2019 following a decision the previous month by the Texas Court of Appeals on a prior lawsuit filed by the fund making similar allegations. That decision affirmed a district court ruling that sided with the city in its use of its own actuarial assumptions to determine how much it should contribute to the fund.

While the fund’s board of trustees assumed a 7.25% rate of return for its actuarial valuation report in May 2017, the City Council subsequently passed a budget that used the Senate bill’s assumed 7% rate of return, a discrepancy that caused the fund to sue the city, Mr. Turner and other city officials.

The lower the discount rate for a pension plan, the higher the required amount to fund in any given year.

If the City Council assumed 7% return, the contribution required to fund the same cash flows would be higher than that of 7.25%. Higher contributions are good for pension fund sustainability – so why is the board complaining?

Several of us pension-watchers were a bit baffled.

Elizabeth Bauer dug into it: Pension Reform In Houston: A Fight Over Assumption-Setting Is Not What It Seems

Back in 2017, the city of Houston recognized that it had kicked the can on its pension plans one too many times, and implemented a pension reform plan which reduced the pension valuation interest rate down from the very-high 8.5% down to 7% in order to gain a truer picture of the pension liabilities, implemented moderate benefit cuts such as retirement age increases and COLA reductions (in some cases, for new hires; in other respects, for all pension participants), authorized a pension obligation bond, and committed the city to a strict schedule to pay down the remaining underfunding. This was all codified in state legislation, SB 2190. (See the City of Houston website for a slideshow on the plan as well as a number of other links to explanatory documents, and the plan’s most recent actuarial valuation.)

At the time, the city celebrated the achievement, but as actuary-blogger Mary Pat Campbell reported in a series of articles at the time, the firefighters’ union remained opposed. And, indeed, they filed suit. In March of this year, the Texas Supreme Court denied their appeal, after having previously lost a case in June of 2019. They tried again, with an alternate argument, and the second time around, at lest as far as the district court is concerned, won their case last week.

Basically, they’re trying to undo the deal made a few years back…. after a $1 billion pension obligation bond was already approved, sold, and put into the various Houston pension funds. Which the city of Houston cannot clawback.

Uh huh.

Here is the fire plan’s most recent CAFR, and on page 28 you can see they used a valuation rate of 7.25% — and the most recent risk-sharing valuation shows on numbered page 6 the use of 7%. I will also point out footnote 1 on numbered page 1 (3rd page of the PDF):

This Risk Sharing Valuation Study has been provided without waiving the Fund’s right to litigate the constitutionality of SB2190.

Mmmhmmm.

I want to point out only one thing. The board of this fund has decided to litigate the constitutionality of SB2190, trying to undo the deal that was made, as noted before. I checked out the composition of the board, and noticed this description:

The ten-member board consists of five active firefighters, one retired firefighter (elected by other retirees), the city treasurer or individual performing those functions, the Mayor or an appointed representative of the mayor and two citizen members elected by the firefighter trustees.

So, of the 10 boards members, two are ex officio from the city, five are active firefighters, one is a retired firefighter, and then there are two non-firefighter members essentially chosen by the firefighters.

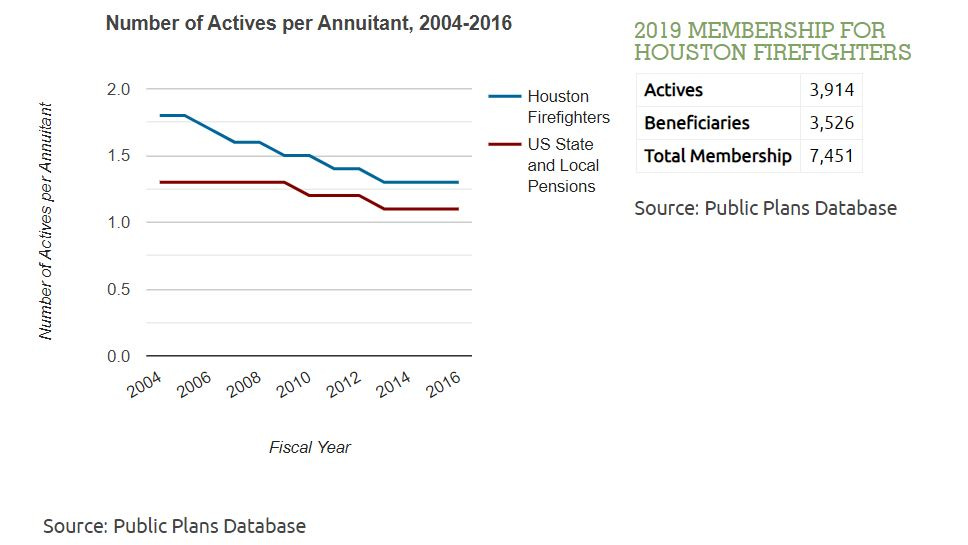

I will point out the trend in active-to-beneficiary ratio for this fund:

Back in 1937, when the fund was founded, a 5-to-1 active-to-retired representation on the pension fund board would have made sense. Given recent plan demographics, current retirees may want to dispute this governance structure.

In any case, the active and retired firefighters may think it a good use of their funds to sue over this issue which affects active firefighter benefits mostly. (Retirees…. is this in your interest?)

While the most recent case was won in the most recent venue, I am wondering who, exactly, is absorbing the costs of this lawsuit strategy. Are the taxpayers making up for the legal costs? The active firefighters in their pension contributions?

I don’t know.

People on the move

You will see what I mean.

SF Chronicle: Yes, people are leaving San Francisco. After decades of growth, is the city on the decline?

Reason: Americans Are Moving Where They Want. Will It Be a Win for Choice or Polarization?

Realtor.com: September Rent Report: Urban Tech Hubs Cooling, Outlying Secondary Markets Heating Up

WSJ: Remote Work Is Reshaping San Francisco, as Tech Workers Flee and Rents Fall

Kind of difficult to get taxes from people who aren’t there.

Illinois Finance and Pension Issues

As always, I protect my readers by putting all the Illinois-related content into one bucket.

Here it goes:

Illinois Policy Institute: STAR OF MISLEADING ‘FAIR TAX’ AD SET TO DRAW $1.1M IN PENSION PAYMENTS FOR 1 YEAR OF STATE WORK

MishTalk: Illinois is the Only State to Borrow Money from the Fed

Center Square: Fitch: Illinois will be challenged to maintain investment grade credit rating

‘Plenty of ways for Illinois to hit junk pretty quickly,’ analyst says

Teachers Pension Fund Official Describes ‘Racist,’ ‘Sexist’ Culture Among Board Trustees

Fred Klonsky: THE CHICAGO TRIBUNE’S ASSAULT ON ILLINOIS TAX FAIRNESS.

The Center Square: Report: Progressive tax would make Illinois less attractive for businesses

Wirepoints: Things That Make You Say ‘Hmm’ About Illinois’ New Bond Offering

Illinois to sell $850 million of bonds as investors brace for junk status

Crain’s: Why pension bonds are creeping back into the conversation

Why? Because they can.

And they’re doing it now because they still can.

$850 million is a spit into the ocean of Illinois debt. Can you say over $100 billion in pension debt? I knew you could.

Public Pension stories

New York State Pension Expands into Real Estate, Absolute Return

Reason Foundation: Employees Retirement System of Texas Solvency Analysis and full pdf report – I didn’t realize they had had negative/infinity amortization

MarketWatch: Opinion: ‘Pathological’ behavior by pension fund trustees leads to billions blown on real estate

WSJ: Texas Pension Commits $400 Million for Private-Equity Co-Investments

Kentucky: State’s generosity in pension benefits now coming home to roost during pandemic

New Mexico retirement board takes step toward divesting of private prison companies

New York: Sisters admit to stealing $22,000 of dead mother’s pension payments

Kentucky Retirement Systems plan nationwide search for chief investment officer

Other Pension and Finance stories

Burypensions: Worst Funded ‘Nonendagered’ Multiemployer Plans

Burypensions: Lone In-Review MPRA Filing

No Withholding: Trump’s tax returns offer a lesson about the state and local tax deduction

NY Post: MTA faces ‘generations’ of ‘suffocating’ debt without bailout, report finds – and here’s the report: Financial Outlook for the Metropolitan Transportation Authority

ai-CIO: OECD Report Outlines Challenges Facing ESG Investing

Elizabeth Bauer: Joe Biden’s Social Security Plan Reduces Elder Poverty But Doesn’t Fix Trust Fund Insolvency, New Report Says

Liz Farmer: Covid-19 Has Cost States $31 Billion In Tax Revenue— And That’s Just The Beginning

Ike Brannon: Private Pensions Are For Retirees, Says The Department Of Labor

Marc Fitch at the Yankee Institute: AFSCME Council 4 in the red due to retirement liabilities, according to federal filings

Elizabeth Bauer: Trump, Pelosi, And McConnell Are All Failing Multiemployer Pensions – And The Rest Of Us

WSJ: Coronavirus Pandemic Hastens the Demise of at-Risk Municipal Money Funds

The Guardian: UK state pension age increases to 66 – and is set to rise further

IBT: Pension Funds Around The World Moving To Abandon Investments In Fossil Fuels

Enjoy!