Pension and Finance Round-Up: 80% Funding Myth Sighting, Junky Illinois, and more

The more: update on bailout talk, universal basic income, and story link dump

As noted, the Actuarial Outpost is likely going to be gone soon (at least in a useful form), and having gotten more firm information, it looks like I will have to move my “watch” behavior to this blog for the nonce while I try to build a place for those sorts of items.

In the meantime, I will share with you the pension, public finance, and other related stories I have been reading.

80% sighting! A COVID miracle!

I’m being snide with this, but it has been so long since I’ve had a real 80% funding myth article spotted by my news search. As per my last 80% fundedness post, this is a dying breed of stories… but one has made my hope blossom forth anew.

AP: Indiana increased public pension assets despite pandemic

Indiana’s public pension funds for state and local government employees, including teachers, has apparently weathered the financial markets’ volatility during the coronavirus pandemic, new data from the state show.

…..

According to INPRS, the state’s prepaid pension programs were 90.6% funded, an increase from their 88.1% funded status at the end of the 2019 budget year, The (Northwest Indiana) Times reported. That means the fund currently has resources on hand to pay 90.6% of all the money it eventually will be required to distribute to pension program participants.Prepaid pension programs generally are considered financially healthy when they are at or above 80% funded.

I note there’s no byline, so nobody I can really blame for this one. But let me see if the myth is in the source, the Northwest Indiana Times —

Indiana grows public pension funds despite market volatility from COVID-19

Prepaid pension programs generally are considered financially healthy when they are at or above 80% funded.

It is! I will mark down author Dan Carden, and see if I can email him. [Reader, I emailed him.]

Immediately following the above is:

Records show the funded status of Illinois’ public pension programs is approximately 40.3%.

Ha. Nice. I will commend him on that, though. [Email sent, and I did commend him on the dig.]

For the record, this has not been the longest pause in 80% funding news stories that I’ve found. I checked against my records and found this one had a gap of 83 days [from July 2, 2020 to September 23, 2020].

But it’s only the second-longest gap. Last year, there was a gap of 189 days between stories — May 13, 2019 to November 18, 2019.

Illinois finance

Bloomberg at MSN: Illinois May Look More Like Junk as Pressure Rises, S&P Says

“Like” Junk? =cough=

Without federal aid, Illinois credit pressures are mounting, and the state may have to borrow more even as officials seek to cut spending and balance the budget, according to S&P Global Ratings.

…..

“With the need for additional borrowing, an elevated bill backlog, and lingering substantial structural imbalance, Illinois could exhibit further characteristics of a non-investment-grade issuer,” S&P analysts Carol Spain and Geoffrey Buswick wrote in a report published Monday. S&P rates Illinois BBB-, one level above junk, with a negative outlook.

…..

Spain and Buswick said it is likely that Illinois will have to issue bonds or again borrow through the Federal Reserve’s Municipal Liquidity Facility to meet cash requirements. Illinois is the only state that has already borrowed from the central bank through the program.But S&P warned that the state will have difficulty repaying a large borrowing within the three-year Fed facility timeline, and taking out a loan to repay a short-term borrowing would increase the state’s fixed costs. The state has strong market access supported by the MLF, according to the report.

Look, Illinois. You’re not getting any sort of (additional) bailout in 2020. You have to figure out what to do to get to the end of the year on your own.

Maybe you’ll get your Democratic-pushed bailout bonanza, but you’re going to need to get past the election and then into 2021 when the new Congress and President are sworn in.

And you may get nothing at all.

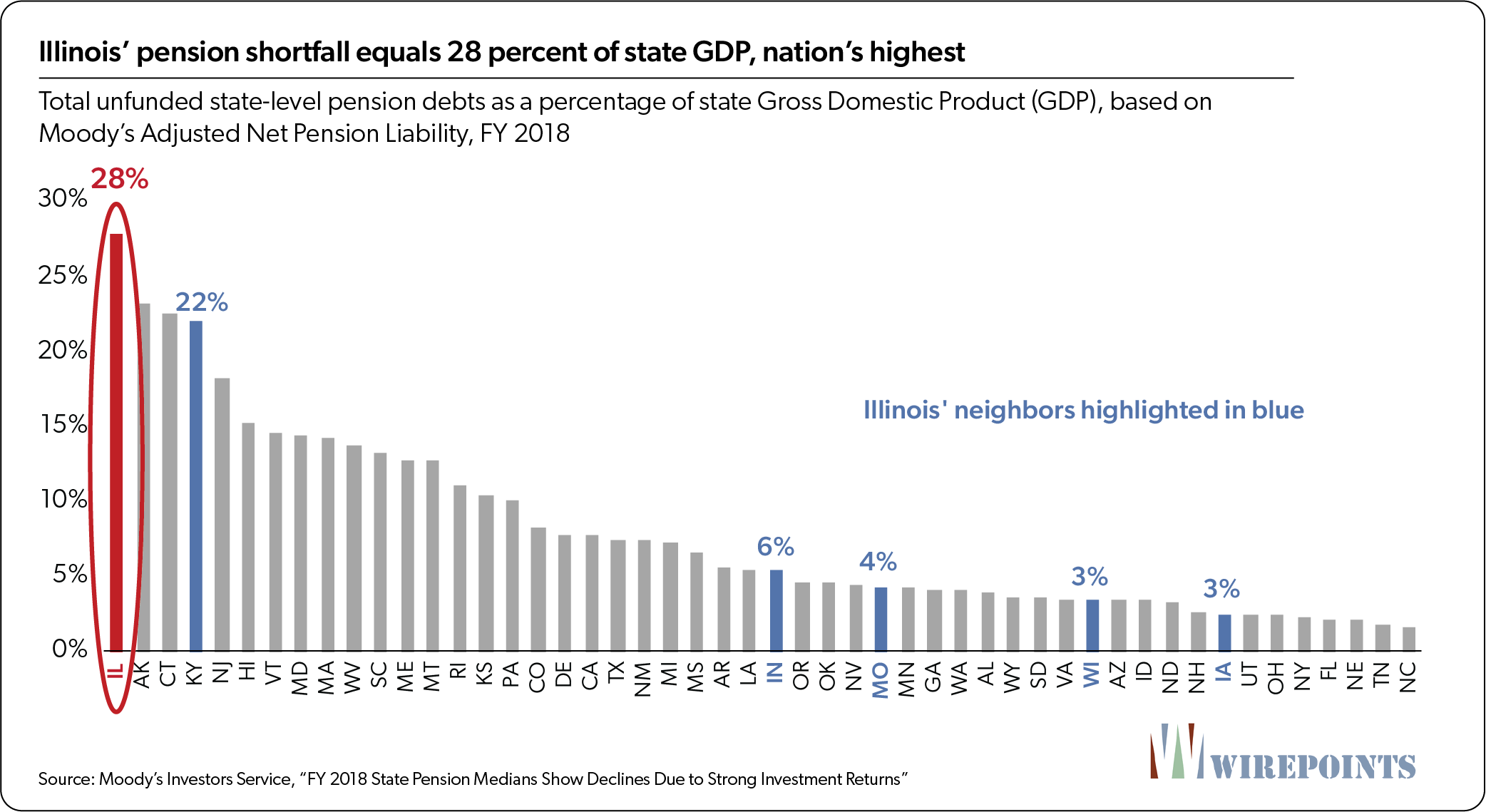

Wirepoints: Moody’s warns Illinois again, state running out of options

Moody’s Investors Service has issued its next warning to Illinois, noting pension debts are overwhelming the state’s economy and will continue to do so over the next year. Moody’s also cautioned against any ideas of improperly funding pensions as a way of providing relief for the state’s worsening budget. The agency said any “reamortization” of pension debts would be credit negative. Moody’s rates Illinois just one notch above junk with a negative outlook.

The warning reflects the continued worsening of Illinois’ financials, which were already in a tailspin long before COVID-19 arrived. Moody’s said, “Even if the US economy rebounds soon, Illinois’ liability-to-GDP ratio is the highest among states and is likely to rise further.”

This is Moody’s statement: Revenue pressure from pandemic to worsen Illinois’ massive and growing pension liability without fiscal adjustments

An excerpt:

To address near-term tax revenue loss from the pandemic, Illinois may choose to defer its financial obligations. Relying heavily on strategies like deficit borrowing or “re-amortizing” its pension contribution schedule would however be credit negative for the state, since such tactics only add to a long-term cycle of borrowing, or deferring payment, to address the consequences of those past actions.

“Contributing insufficient amounts annually to meet long-term benefit obligations is a short-term fiscal management tactic Illinois has used for years, and helps explain both the magnitude of the state’s pension problem and its credit standing,” [Moody’s analyst Ted] Hampton notes. “Underfunding pensions again could lead to further credit deterioration, depending on the degree of underfunding, the state’s other financial strategies and the performance of its pension investments.”

I’m betting on them being irresponsible, because why would they change now?

The Center Square: S&P warns delayed spending cuts could push Illinois into ‘non-investment grade’ territory

Yvette Shields: Coronavirus squeeze puts debt on the table for Chicago

BGA: New Data Enhances BGA [Illinois] Public Salary Database

Elizabeth Bauer at Forbes: Pension Failures, Governance Failures – Illinois Once Again Is The Poster Child

Wirepoints: The Ultimate ‘Fair Tax’ Treachery Is The Ballot Itself – Updated – Wirepoints

NPR Illinois: Lawsuit Filed Over Graduated Income Tax Ballot Measure

Jim Dey: Changes to tax amendment’s language may open door wider than thought

Fred Klonsky: WHAT’S GOING ON WITH STATE AND CITY TEACHER PENSION FUNDS? – I also noted the ouster of Dick Ingram with no further comments. I would like to know what that was about. At least with Calpers, I know why people got booted. And now I hear someone at the Chicago Teacher’s Pension Fund has left…. hmmm.

The Federalist: Pritzker Is Keeping Illinois Locked Down Not For Health But For A Federal Bailout – ha ha ha…. see above and below. Illinois is not getting bailed out. Maybe some spending change, but nothing to get them out of their debt hole with is hundreds of billions of dollars.

State of a bailout

Senate Democrats like Chuck Schumer (D., N.Y.) have been blasting the latest GOP stimulus proposals for not earmarking enough aid to state and local governments. But a new report suggests Washington has already overdone it when it comes to shovelling federal funds to state pols.

Republicans seem to understand this and are so far making at least some effort to resist another taxpayer fleecing. White House Chief of Staff Mark Meadows told reporters on Wednesday that “the biggest stumbling block is if we use this pandemic as a bailout mechanism for poorly run states… I think that would be a very difficult hurdle to overcome.”

A report this week from the Wall Street research firm Strategas finds that, thanks in part to federal checks already received, state governments in general are already more than generously funded. The Strategas team writes of the Washington stimulus negotiations:

If a deal is to be reached, it will be because there is a recognition that $1 trillion for states is not needed at this time. Data from the Bureau of Economic Analysis backs this point up. State and local governments closed Q2 with a $129bn surplus. It is rare for states to hold a surplus in BEA data and it was in the quarter with shutdowns and a delay of Tax Day. Obviously, the change in fiscal circumstances was driven by the large infusion of cash delivered from the federal government in the CARES Act.

But even stripping out federal aid showed that tax revenues fell just $16bn in Q2, or 3%.

If a particular state government is still experiencing fiscal disaster, it’s not due to Covid.

Mmmmmm.

Kansas Policy Institute: Federal bailouts of state budgets hasten fiscal disaster

Illinois Policy: LAHOOD FILES TAXPAYER PROTECTION ACT TO STOP BLANK-CHECK BAILOUTS OF MISMANAGED STATES, FIX ILLINOIS’ PENSION CRISIS – it’s not going anywhere, but glad somebody put it out there

Elizabeth Bauer: State And Local Bailout-Aid With Pension Reform Strings Attached? LaHood’s Plan Is Promising But Risky

Ronald Fisher at Governing: How State and Local Governments Are Crucial to the Economy

U.S. blue states build debt stockpiles as virus aid is stymied

WSJ: Congress’s Covid Income Redistribution – “We calculated the per-capita annualized increase in transfer payments, and many Democratic-run states received nearly double what GOP-run states did: New Jersey ($14,033), Illinois ($9,223), New York ($9,030), California ($8,673), Washington ($8,511), Oregon ($8,258) and Connecticut ($7,879) versus Texas ($6,450), Indiana ($6,085), Tennessee ($5,430), Florida ($5,399), Georgia ($5,353) Arizona ($5,326) and Utah ($5,184).”

The Fiscal Times op-ed: States Can Get by Without Additional Federal Aid

Reminder — I am not a fan of the Bailout with Strings Attached concept. The strings won’t stay attached.

My preference is what I call “Choices have consequences”. No bailout, no state bankruptcy.

Stockton Universal Basic Income project mentioned… why?

WSJ: Cities Experiment With Remedy for Poverty: Cash, No Strings Attached

Last year, Stockton, Calif., embarked on a civic experiment. For 18 months the city would send $500 a month to 125 randomly selected households in low-income neighborhoods. Researchers would compare the effect on participants’ health and economic situation to that of residents who didn’t get payments.

The $3.8 million experiment is the brainchild of Stockton’s 30-year-old mayor, Michael Tubbs, made possible by the Economic Security Project — a group co-founded by Facebook co-founder Chris Hughes that funds guaranteed-income projects — and other donors. Stockton is at the forefront of a rethinking of the American safety net among some academics and public officials, particularly as the coronavirus pandemic has revealed the financial fragility of many households. They say the best way to combat poverty is to give cash to poor households, trusting them to make their own best decisions.

……

Critics point to several potential drawbacks.First, if only people below a certain income receive the transfers, and aren’t required to work, they may hesitate to take a job, or a higher-paying one, since they would then forgo the payment. The result could be less work and less economic dynamism.

Second, a national guaranteed income would carry a steep price tag. Giving $10,000 a year to individuals earning less than $20,000 or married households earning less than $40,000 with a long phaseout period would cost roughly $1.2 trillion, according to University of Maryland economist Melissa Kearney and Magne Mogstad, an economist at the University of Chicago.

…and there the article ends. Huh? Why is this “news” at all?

Hmmm, that bit was preceded by this Bloomberg piece: A Radical Free-Money Experiment Became Vital When Covid-19 Hit

The idea of the government giving people money directly has been cycling in and out of favor in America for more than 200 years. It’s the essence of Social Security and the annual dividend paid to Alaska residents, and it was gaining adherents again in 2016 when Stockton elected Tubbs as its first Black mayor. He was 26, born on the city’s south side to a teenage mother and an incarcerated father, and educated at Stanford. A cousin’s murder had drawn him back home. He’d served a term on the city council before winning 71% of the mayoral vote. One of his priorities was finding ways to alleviate Stockton’s deep poverty and economic inequality, which saw White families earn twice as much as Black families on average.

…..

[had to cut from original STUMP post for substack limits](They expect to release their analysis of the pre-pandemic months early next year and the results of the entire experiment in 2022.)

Okay, we’re not going to see the results from any of this til next year at the earliest. I suppose the WSJ piece occurred because of the Bloomberg piece. There’s nothing particularly newsworthy (in terms of events), but it does go over a couple of cases, arguments, etc. Not a bad piece but it’s all supposition about long-term effects and potential wider policies.

I have my own interest in the results.

Prior posts on UBI:

May 2019: Universal Basic Income: This Time, Something Something!

September 2019: Selling Universal Basic Income: Life is a Game!

March 2019: Everything Old is New Again: Universal Basic Income

February 2019: The Stupid Idea That Will Not Die: Universal Basic Income Might Come to Chicago

February 2018: Friday Foolery: Stockton Tries Universal Basic Income… Maybe

August 2018: Chicago Stupidity: Universal Basic Income, Pension Obligation Bonds, and Divestment

Leftover stories

Manhattan Institute: Taking Control: How the State Can Guide New York City’s Post-Pandemic Fiscal Recovery

Elizabeth Bauer: Why Are New Jersey’s State Finances Worst In The Nation?

Daines urges Senate to pass bill preventing pedophiles from receiving pension – this is about federal pensions

Townhall Finance: Fiscal Insanity From New Jersey

Wiley Online Library: Public pension reform and the 49th parallel: Lessons from Canada for the U.S.

Cuomo to Local Governments: No Long-Term Borrowing – this is mostly to NYC

Texas Public Policy Foundation: Local Government Debt

Kentucky: State’s generosity in pension benefits now coming home to roost during pandemic

Barnet Sherman: Muni Bond Market Disclosure: Thoughts From Standard-Setters And Stakeholders

New York Second Slowest State to Recover COVID-Lost Jobs – number 1 is Hawaii

John Bury: $4.7 Billion Pension Payment Plan Passes – this is for New Jersey

Brookings: How much is COVID-19 hurting state and local revenues?

Yankee Institute: After securing raises for [CT] state employees, unions run ads to tax the rich – yes! SALT cap zero! (no, that’s not what they’re advocating)

FiscalData.Treasury.gov: New-to-me data sets from the Treasury Department – This one will be interesting: Annual federal government debt going back to FY1789. I may look at Debt-to-the-penny, too, but that goes back to only 1993

Worth: This Proposed Rule Change Could Threaten Retirement Plans Using ESG Investments

Center for Retirement Research at Boston College: 2020 Public Plan Investment Update and COVID-19 Market Volatility – relates to my post on How to Lose Money Quickly: Trading in a Volatile Market

Ed Ring at Fox & Hounds: Why Can’t Sacramento’s Financial Reporting Match Private Sector Standards?

Pension Pulse: New Jersey Hits The Pension Brick Wall

WSJ: Moody’s Downgrades New York State, New York City Credit Ratings – they both went down one notch to Aa1; in contrast, Illinois’s rating is Bbb1, one notch above junk (excuse me, “high yield”) rating.

Elizabeth Bauer: Never Mind Biden’s 401(k) Plan – Are Pension Plan Tax Breaks Fair?

Reason: As Policing Changes, So Should Their Retirement Plans

P&I: Getting governance right key for public pension plans – this relates to Calpers specifically. I’m keeping an eye on Calpers, but haven’t heard anything lately.

DiNapoli: Westchester Sisters Admit to Stealing $22,000 of Deceased Mother’s Pension Payments – the NY state comptroller has been adamant about chasing down pension fraud like this. Not sure about other states.

Washington Examiner: Biden’s dramatic change to retirement accounts could reduce their availability, industry warns

OpentheBooks.com: Why New York City Is In Trouble – 114,041 Public Employees With $100,000+ Paychecks Cost Taxpayers $14.6 Billion

Reason: Florida’s Public Pension Investment Return Assumptions Are Too Risky and Driving Debt

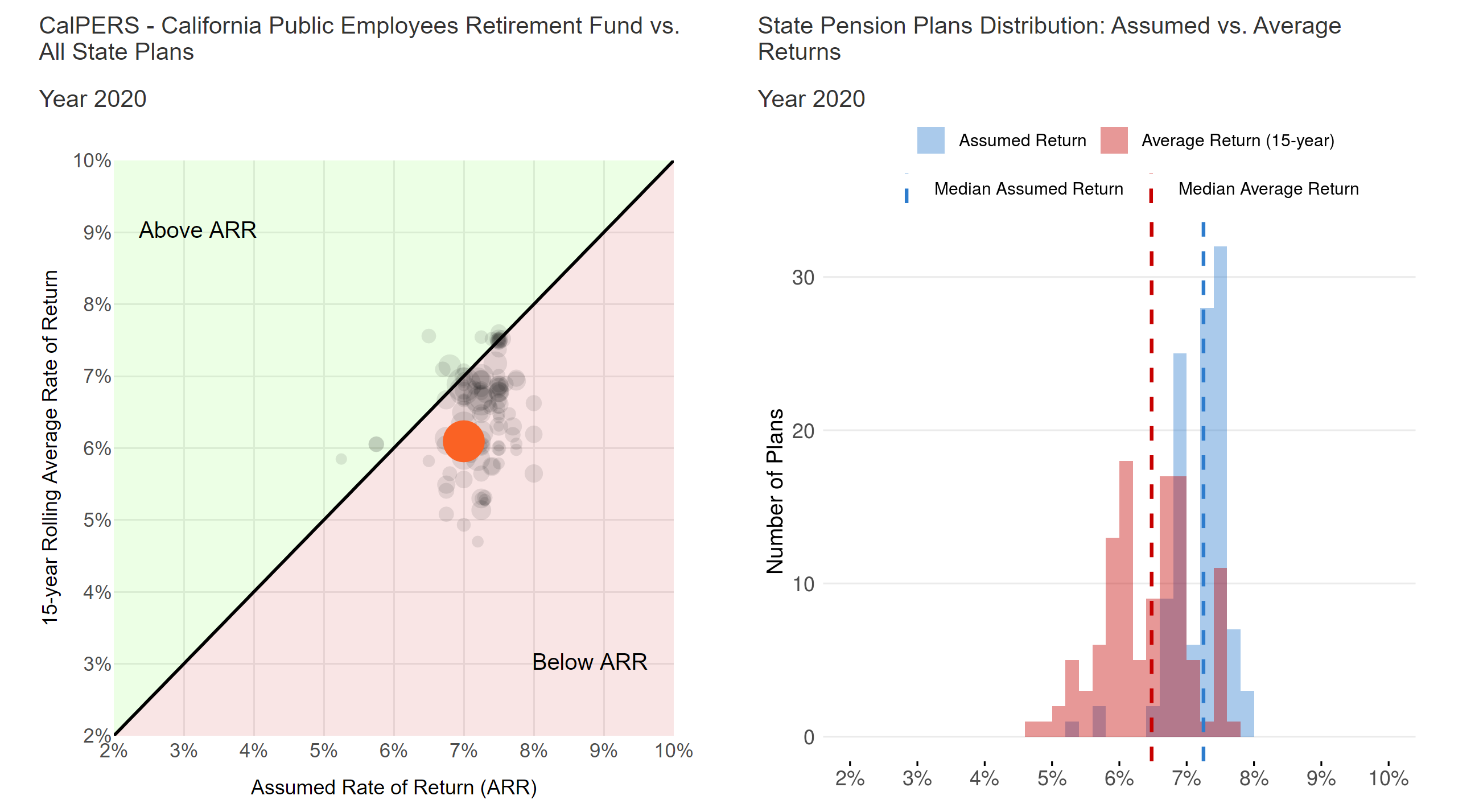

Reason: Public Pension Investment Performance Has Historically Fallen Short of Return Assumptions

This last one has good charts. These are the ones I particularly like:

On the left, Calpers is represented by a big red dot (as it’s the largest public pension fund in the U.S.) and the other dots are other U.S. plans. It compares the plan’s 15-year performance (so this will straddle the Great Recession of 2008-2009…. but not the early 2000s recession in 2001) against the assumed return. If the dot falls in the red zone, the investments didn’t hit that target…. and, more importantly, the farther away the result is from that 45-degree line, the worse the disparity.

On the right, you can see the two distributions of the 15-year average return against the assumed return. I will note that the histogram of the assumed return is heaped around 7.5%. My other observation (as I have not tried to replicate their distributions…. yet) is that many (most?) of the plans have changed their assumed rate of return over the past 15 years, so I don’t know if they took the weighted average of assumed returns, or just the most recent.

Enjoy!