Keeping Up with Meep: Public Pensions, MEPs, Public Finance, and More

As the Actuarial Outpost is seemingly down for the count, I thought you might be interested in the kind of news dump I skim when looking for stories on my favored blogging subjects.

I may or may not have comments on these. When I’m using the AO as my external memory, I usually keep my remarks to myself.

All of these will be stories hitting my news search from the last week.

Public Pensions stories

P&I: Public plans miss targets, eke out single-digit returns

This doesn’t surprise me. Many/most public plans are on a fiscal year that ends June 30. S&P 500 from June 30, 2019 – June 30, 2020: 2964.33 to 3100.29. That’s a 4.6% increase, far below most plan targets. Of course, many pension plans are invested in certain asset classes that took a heavy hit – none are 100% in the S&P, equally weighted.

P&I: Strong equity returns require long investment horizon, CalPERS finds

An excerpt:

CalPERS’ more aggressive return-seeking assets including private equity did not start to provide outperformance until the 10-year period ended June 30, according to a report to the board’s investment committee.

….

It’s not until the 10-year period that the portfolio started to show that public and private equities showed stronger returns than more conservative assets. Global fixed-income net return was an annualized 5.85% for the 10 years ended June 30, while global equity net return for the same period was an annualized 9.68%. Private equity, meanwhile, earned a 10.43% net internal rate of return for the 10 years ended March 31, according to reports to the investment committee.

This is not a cause-and-effect issue, though the headline sets it up that way. It is just noting the results over a particular period, for particular portfolios which, of course, changed over the decades. Private equity, after all, mainly gets its returns via investing in some business, and then selling it off after, hopefully, the business has appreciated in value (and usually in investment horizon of 5-ish years, depending.)

The reason more “conservative” investments (like bonds) did “well” in the short run was because of their run-up in value due to decreasing interest rates. Perhaps the framing of the headline and the results are in direct support of their leverage strategy, which amplifies results — both in the downside as well as upside. That’s the point of leverage.

If you’re interested in something that may be more indicative, check out this history of returns on public equities and bonds. In all these cases, you need to consider the volume of the markets, which are not listed there.

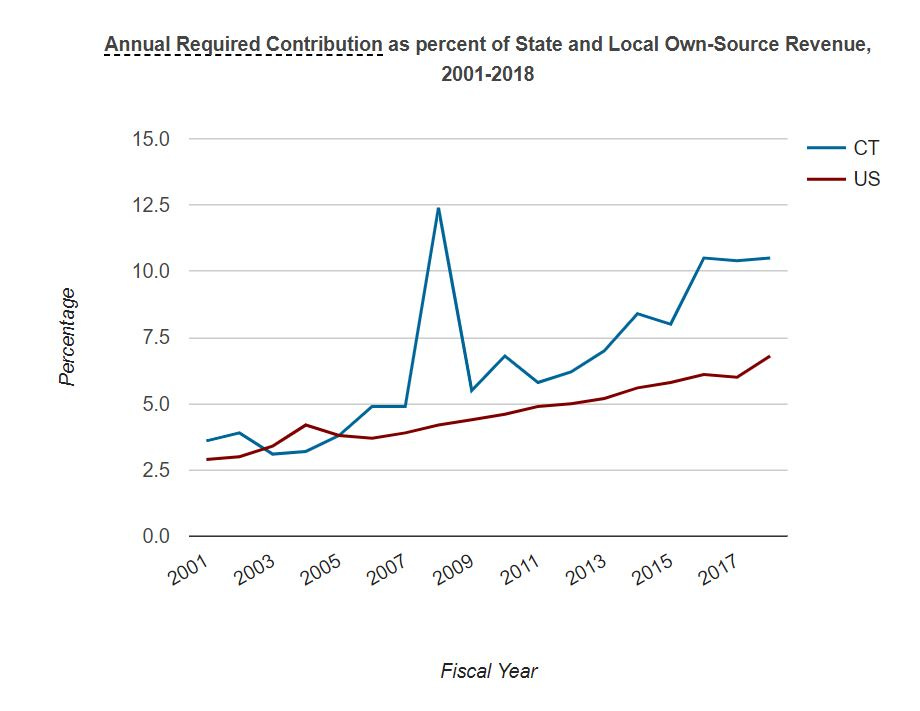

Hartford Courant: Connecticut pension fund on sustainable path, an op-ed by the CIO in CT Office of the Treasurer. I am skeptical.

Let me quote the op-ed:

As State Treasurer Shawn T. Wooden has said many times, we have significant unfunded pension liabilities that stem from over seven decades of underfunding and historically unrealistic investment return assumptions.

….

The assertion that the state will have issues contributing to the plans in the future due to the economic impact caused by the coronavirus is just not accurate. In fact, this year we expect the state to make its annual employer pension contribution payment and, for the first time in 19 years, make $75 million in additional payments towards reducing our unfunded pension liabilities.On his second day in office, Treasurer Wooden started work on a plan to restructure the Teachers’ Retirement Plan to make it more sustainable for the long-term. Moving to a more realistic investment return assumption — reducing the target from 8.0% to 6.9% — was a key priority.

….

Another important component of this restructuring that is sometimes overlooked was the change to the amortization method used to calculate state contributions to a level dollar basis. The level dollar method means a level payment every year, like a mortgage.

These are good changes, and help the plan’s sustainability. But here’s the problem:

I will be coming back to this in the future.

NBC10 Boston: Court Rules Against Former Winthrop Chief in $1M Pension Case

Rescinding the pension of any public employee, even when convicted of criminal acts, can be difficult, and usually involves explicit court cases. In many (or most) cases, for it even to be allowed, the criminal acts have to be related to their job (that’s the basis of the court case here).

Illinois Public Pension Stories

Yes, this gets its own category.

Adam Schuster, Guest Columnist: COVID-19’s economic shock exposes urgency to fix Illinois’ largest problem. That problem, of course, is pensions.

The Center Square: Illinois pension debt climbs as pandemic hits funds

“This is going to be counted as an actuarial loss because it’s below that actuarial assumption,” said actuary Mary Pat Campbell, who maintains a popular blog on public pensions. “When you do the roll-forward of the unfunded liability, from 2019 to 2020, that’s going to count as a loss, as well as other things that may count as a loss.”

Yes, I did say that. He didn’t quote me saying the following, but there may be “actuarial gains” on COVID deaths (if retirees die earlier than expected, that’s a gain) but there may also be actuarial losses relating to early retirements spurred on by multiple developments (teachers retiring early if they think they’ll be put in danger from in-person teaching; police retiring earlier due to de-funding movements, etc.)

Chicago Tribune op-ed by Mark Glennon: Commentary: Yes, Illinois pension reform can come through a constitutional amendment

I should hope so. A state constitution is not a financial suicide pact.

Illinois courts have firmly interpreted the state’s constitutional pension protection clause to bar all meaningful pension reform. The only two clear paths to override the clause and our courts are bankruptcy and a state constitutional amendment. State bankruptcy would require federal legislation, which is not in the cards for now, and would be hotly contested if it were.

That leaves a state constitutional amendment as the option at hand. Illinois has no excuse for not pursuing it and getting on with the task that’s essential to ending our fiscal crisis — reforming public pensions.

…..

Reform opponents routinely claim, as Pritzker did, that the federal Constitution’s contract clause bars adjustments to pensions, which are contracts.But the United States Supreme Court and lower federal courts have long made clear that the contract clause is not an absolute. Contracts can be impaired if the impairment serves an important public purpose. Importantly, the contract modification cannot overreach, and must be narrowly tailored to honor contract rights as best as reasonably possible under the circumstances.

Illinois’ fiscal crisis provides those circumstances. That crisis was unfixable without significant pension reform even before the pandemic, and the resulting recession has devastated state and local budgets, sealing the case.

…..

Finally, consider what the state of Illinois’ own lawyers say.In July, landlords went to court over Pritzker’s emergency order suspending eviction of residential tenants. The suspension, they claimed, violated the federal contract clause because their lease contracts gave them the right to evict.

But the state answered that even if the suspension impaired the landlord’s contract rights, it’s permissible because the suspension serves “an important public purpose.”

Well, well, well.

Mark Glennon and his colleagues at Wirepoints have put together a package of posts on Illinois pension reform, up to three parts currently:

Part 1: Solving Illinois’ Pension Problem | Part 1: Illinois is the Nation’s Extreme Outlier

Part 2: Solving Illinois’ Pension Problem | Part 2: Illinois Pensions – Overpromised & Overgenerous

Part 3: Solving Illinois’ Pension Problem | Part 3: Why Pension Reform is Legal

Elizabeth Bauer: ‘COVID-19 Was A Dress Rehearsal’ – Illinois Pension Reformers Are Not Giving Up

Like Bauer, I’m very happy that the pension reformers aren’t stepping back during COVID, and using the financial strain governments are feeling from new crises as an argument to deal with the self-inflicted pension crises.

Elizabeth Bauer: Chicago Is Considering Issuing A Pension Bond – And Taking A Gamble

As my long-time readers know, I hate Pension Obligation Bonds. They’re tools of the devil. And isn’t it interesting that the worst-funded pension sponsors are generally the ones issuing these bonds.

(Well, not really interesting. Completely expected, especially in a low interest rate environment.)

Multiemployer pensions

Benefits Pro: The crisis of multiemployer pension plans: Where do we go from here?

I haven’t done an MEP update, but this is something that will be dire within 5 years if Congress does nothing. Prior post related: March 5, 2020 Multiemployer Pensions: Prior Bailout Plan’s Shortcomings and State of Play. Yes, I had something about the MEP provisions in the MoneyPalooza Monstrosity, but that bill is not passing this year.

P&I: Multiemployer plans get tiny reprieve in latest PBGC report

The Pension Benefit Guaranty Corp.‘s single-employer program will remain in the black over the next decade, while the multiemployer program could gain another year or two before insolvency, according the agency’s latest projections report released Monday.

….

Last year’s report projected that the multiemployer program would become insolvent by September 2024, while the latest report projects a very high likelihood of insolvency by September 2025 and near certainty by September 2026. PBGC officials attribute the slight improvement to enactment of the Bipartisan American Miners Act of 2019, which relieved financial pressure on the PBGC for the insolvent United Mine Workers of America 1974 Pension Plan.

The near certainty is due to the Central States Teamsters plan having run out of money by then.

John Bury looked at the PBGC report: PBGC Projections – 2019

And highlighted this item from the report:

No scenario shows the Multiemployer Program remaining solvent beyond FY 2027 under current law. (page 10)

This is because no scenario includes magical money fairies showering down unlimited riches on troubled MEPs.

P&I: Ohio Teamsters local applies for MPRA benefit reduction

A reminder – the concept of MPRA benefit reductions is that troubled MEPs can cut benefits, as long as they would run out of cash otherwise, the cut benefits are higher than the very low MEP PBGC guarantees, the cuts are applied fairly across plan members (doesn’t mean they’d all get cut the same), and they can show the fund would survive after the cuts.

There have been plans with benefit cuts, and the Central States Teamsters plan had submitted benefit cuts to the Treasury Department under this program, and that plan was rejected, because the Treasury said the cuts were inadequate to lead to a sustainable plan. So the Central States folks said “I guess we’ll just have to run out of money and take down the PBGC with us.” Well, not in those words, but we knew what they meant.

Public Finance

Asbury Park Press: NJ budget: Taxes, more debt, ballooning pensions and more undesirable choices on the table

As it becomes clear that no federal bailout of state and local governments is happening this year, you’re going to be hearing a lot of grim public finance stories.

NYPost: Democratic leaders are ignoring the single biggest threat to their states. Okay, fine, this one is about public pensions, too. Most of the grim public finance stories are ultimately about pensions, as pretty much every place with the dire “IF WE DON’T GET FEDERAL BAILOUT WE WILL DIEEEEEE” stories are places with pretty hefty public pensions that they can’t support pay-as-they-go even in good times.

NJ Spotlight: New Details on NJ Borrowing Plan as Fight Looms Over Tax Estimates. The governor wants to borrow $4 billion, on a 10-year term. To pay for regular operational spending.

Leftover items

Plan Sponsor: PBGC to Pay Pension Benefits for McClatchy Workers and Retirees. This has been known for months since McClatchy filed Chapter 11. This is what happens to single employer DB pension plans when the sponsor goes bankrupt.

Ridgefield Press: Ridgefield Civil War vet left a pension his widow enjoyed twice — an interesting historical story involving a pension… and it’s really not that unusual.

Now, the above isn’t a full week of articles… I just stopped at what looks like “enough”.

Originally, when I got into public pension watches, I thought I might not have enough material to watch.

I’ve never lacked for material.

Enjoy!