GameStop Follies: Hedge Funds, wallstreetbets, and Public Pensions

(some of us find it funny)

Let me step away from the mortality analysis and consider something entertaining: the current GameStop (and Nokia, Blockbuster(?!), silver, and…) mania.

Quick explanation of what got people’s attention

I am not going to explain this myself — plenty of others have explained what is going on. Indeed, I’ve been gathering stories on my new site: Actuarial News as this develops, trying to grab a variety of analyses.

If you just want the links to the current brou-ha-ha, here are items tagged with GameStop.

I am cribbing from one explainer from the Hustle: GameStop’s Reddit-fueled rally, explained (and they grabbed it ).

GME was first pitched as an investment on r/WallStreetBets about 2 years ago, but the current craze built up over the past 12 months.

Members on the subreddit r/WallStreetBets believed that GameStop [ticker GME], with 5k+ brick ‘n’ mortar locations, could turn around its fortunes by going digital.

On Aug. 31, 2020, Ryan Cohen — the billionaire founder of pet company Chewy — bought up a big position in GME (he now owns 10%+ of it) with plans to modernize the company.

In the months since, a number of prominent hedge funds (Citron, Melvin Capital) revealed they were betting against (AKA short selling) GME.

Typically in short selling, you: 1) borrow a stock; 2) sell it to a buyer; and 3) if the price of the stock falls, you can buy it for a cheaper price you sold it at and return the stock to the person who lent it to you.

One risk of short selling is called a “short squeeze.” Since you have to eventually return the stock you borrowed, problems can arise if there is a limited supply of the stock.

In a “short squeeze,” the underlying stock will get bid up as short sellers try to get their hands on stock that they have to return.

Options trading — the right, but not obligation, to buy a stock at a certain price — is also driving GME up as institutions that sell these options are buying GME stock to hedge their position.

GME stock is on an upward tear as these market mechanics play out and r/WallStreetBets traders coordinate their efforts.

There are all sorts of sub-stories out there, almost all of which are making me laugh harder and harder. The wallstreetbets folks at reddit will likely absorb some losses as GameStop’s stock price comes back to a more reasonable level. As of right now (3 February 2021), the price has come down a lot from the peak, but it still looks overvalued to me. Also, the stock has bubbled up and down a lot already, so it could shoot up again.

But this ain’t their first rodeo, those bozos at r/wallstreetbets. (Indeed, many are going on to play with silver, Nokia, and other stocks/commodities.)

That subreddit is full of people with “investment ideas”, and a lot of it is day-trading, not long-term investment at all. Maybe some look at it as long-term if they hold the position at least a year (that has tax implications), but a lot of the people are day traders and play with options. Many of them brag about their losses. These folks are not to be put off by talking up the money they lose.

But what about those hedge funds?

Setting out the landscape

I did a video overview, talking about a variety of topics I plan on writing about due to this particular episode. This is not just about a bunch of self-styled investment bros mobbing hedge funds, but about elements of risk that many people ignore.

Pension fund connection to hedge fund follies

First, I have not looked into who invests with Melvin Capital or Citadel Capital, two of the major hedge fund targets for the r/wallstreetbets people. I would be interested, but I haven’t spent any time digging into that.

So the pension fund connection is not that I know any pension funds are invested with these particular hedge funds…. but that I know that public pensions have really increased their holdings in alternative assets, such as hedge funds. And I find this extremely concerning.

CNBC: Why the GameStop frenzy may hurt retirees along with hedge funds

Reddit users and other retail investors who piled into GameStop stock aimed to take down Wall Street.

Pension funds, which support ordinary Americans in retirement, may be an unintended casualty.

Some hedge funds have sustained big losses as a result of bets against GameStop stock. Melvin Capital, for example, lost more than 50% in January.

But pension plans — which invest assets on behalf of workers like teachers and police officers — may hold big positions in hedge funds. That means a financial hit for hedge funds could spill over to workers’ retirement assets.

There are loads of hedge fund strategies out there. Not all of them do highly leveraged shorts as Melvin Capital did.

But seriously, how is it appropriate for any pension fund to have assets following that strategy. I’m just thinking from an asset/liability management issue, hell, a general risk management issue.

One problem pensions have in the U.S. is that they don’t seem to think in terms of risk capital. That means having to hold capital against potential losses in your assets (and also other risks, like asset/liability mismatches). Insurers have to do this.

To be sure, most people in the investment world really don’t think in those terms.

MAYBE THEY SHOULD.

Appeal to sympathy/empathy

Back to the CNBC piece:

“Your ‘eat the rich’ mentality just took a bite out of the pension funds of working Americans,” Barbara Roper, director of investor protection at the Consumer Federation of America, said of GameStop investors who targeted Wall Street

“It’s not a victimless game, and it’s not a Wall Street billionaire who’s going to ultimately pay the price,” Roper added.

Roughly 7% of the $4.5 trillion in state and local pension plans are allocated to hedge funds, according to data published by the Center for Retirement Research at Boston College and the Center for State and Local Government Excellence. These plans (which don’t include plans in the private sector) support 14.7 million workers and 11.2 million retirees.

First of all, the r/wallstreetbets people do not care. I tried reading about two posts in that subreddit, and it doesn’t come across as a group of people who would be more sympathetic than me for this situation.

Second, the reason I say that, is that I lack sympathy for public pensions losing money by pursuing investment strategies that may be completely inappropriate for the funds. The r/wallstreetbets guys would likely say (translated into frumpy middle-aged lady speak and not the offensive terminology they prefer): we are a bunch of bozos doing crazy things, but it’s our own money… should public pensions be involved in strategies as crazy as ours?

Now shorting isn’t necessarily crazy, but it is very risky, and shorting more than 100% of the stock that exists may be legal when done in certain ways, it is even riskier.

The potential upsides can be very large… but the potential downside is infinite (in practical terms, there is a limit to the downside, which is basically all the money you have.) I will write about that in a future post.

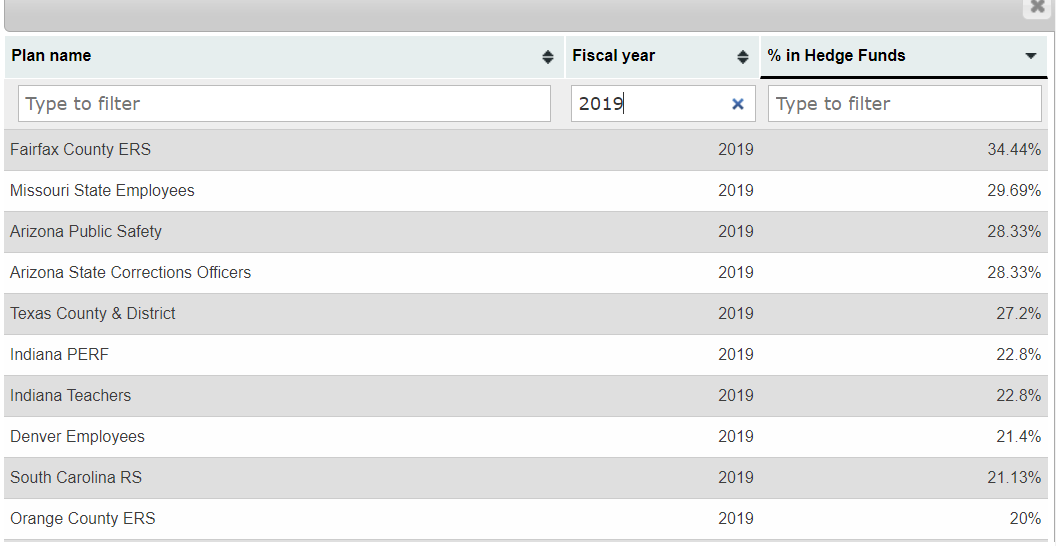

Highest pension allocations to hedge funds

Back to CNBC:

But many pensions allocate much more, some even north of 20% of their overall portfolio, according to Pensions & Investments.

The top four by overall portfolio share are: The Directors Guild of America-Producer Pension Plans (23%), Eli Lilly & Co. (28%), the Alaska Electrical Pension Fund (30%) and Eastman Kodak Co. (41%), according to P&I, which surveyed the 1,000 largest pension plans about their investments as of September 2019. (The company is publishing 2020 data next week.)

…..

Many plans aimed to increase their allocations to hedge funds and other alternative assets in 2020 to try boosting returns amid lower relative yields from safer assets like cash and bonds.

So note that the pensions that P&I listed as allocations were two multiemployer pensions and two single-employer private pensions. It seems they only cover private pensions (because it’s really easy to get that data — it’s in the IRS Form 5500, and yes, I’ve worked with that data for other things.)

I decided to search at the Public Plans Database, and here are the allocations I found:

The PPD is great as a source, but it is tough to get that data, and the PPD folks have to manually enter a lot of it by finding the info in PDFs which are standardized in their forms.

Some of those allocations, just… ugh.

But there is a reason all these pension funds have been looking to hedge funds — basically, they know they can’t reach their self-imposed investment goals without taking on a lot more risk than they used to.

The plague of low interest rates

Reason Foundation has been covering this very well.

From October 2020: Why Low Interest Rates Are Bad News for Public Pension Plans

The Federal Reserve recently announced its plans to keep interest rates near zero for at least the next three years. This shift from the Fed’s longtime strategy of raising rates to ward off inflation is bad news for state pension systems, many of which have been struggling to meet overly optimistic assumed rates of investment return.

….

When Treasury rates are low, public pension system plan managers may be forced to search for alternative, higher-risk assets to meet their plans’ assumed rates of investment returns. Ideally, however, these return rate assumptions would be lowered to better fit market conditions. But many public pension plans are loath to absorb the significant increases in public spending that this change would entail due to the higher pension contributions from workers and/or employers that would be required. This is especially true right now, as states across the country are facing major budget deficits due to the coronavirus pandemic and recession.

And from January 2021: How the Federal Reserve’s Actions and Low Interest Rates Impact Public and Private Retirement Savings

The extended period of low interest rates we’re in is not only creating challenges for public pension systems across the nation, but it is also negatively impacting people who are relying on their own savings to fund their retirements.

….

The decline in interest rates since the 1980s has multiple causes. One is lower inflationary expectations: during and after the high inflation of the 1970s investors demanded high rates on fixed-income investments to compensate for the potential loss of purchasing power.…..

Low Treasury interest rates also pose a challenge to defined-benefit pension systems because these systems typically depend on asset growth to meet future pension payments. As risk-free interest rates fall, managers of defined-benefit systems must either lower their assumed rate of return (thus increasing actuarially determined contributions) or take on additional risk to try meeting return expectations. Because very few public pension systems are lowering their assumed rates of return we have seen a significant increase in public pension debt in the last 20 years. Even before the COVID-19 pandemic disrupted the economy and state budgets, the total public pension debt nationwide equaled $1.2 trillion.

So, while I am just as unhappy about low interest rates as these two authors (Alix Olliver and Marc Joffe), my take is that the central banks are somewhat forced to go to very low interest rates (including negative nominal rates!)

I have been watching the Japanese interest rates for almost two decades now. Their central bank has tried to increase interest rates a few times, only to be beaten back.

My own opinion is that the general interest rate environment has been driven by demographic change more than anything else.

Also, yes, low interest rates hurt annuity income, and that it’s gotten really bad with increasing longevity as well. And rather than say “You gotta raise interest rates!”, my take is that you just have to accept that these types of promises just inherently are very expensive. Yes, that sucks if you’re a retiree, but it’s reality.

Rather than accept that reality, public pensions (and other pension funds) have been trying to reach for yield via increasing their asset risk exposures — if one wants high returns, one has to take on high risk, right?

But high risk means that you can have really bad downsides.

And the assumption, of course, is that taxpayers will be there to make it good.

Argument from the public pension side

The following was written before all these bozos decided to have fun at Melvin Capital’s expense. But it was published as they really took off.

Ben Meng: Saving America’s Public Pensions

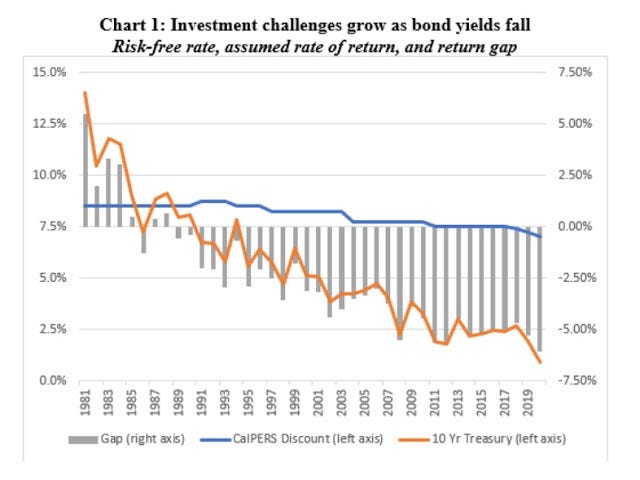

The main challenge facing the public pension industry is the high assumed rates of returns on pension assets relative to what equities or bonds are likely to deliver.Many US public pension funds expect a rate of return in the neighborhood of 7% per year. But in today’s capital-market environment, achieving that sustainably over the long term has become an increasingly daunting task.

In fact, this is not a new problem. As Chart 1 illustrates, the gap between the risk-free and assumed rate of return has been widening for the past four decades. In the1980s, the risk-free rate (as approximated by the yield for ten-year US Treasury bonds) was often far higher than the assumed rate of return, making it relatively easy for pension funds to hit their targets. Today, however, the risk-free rate is more than six percentage points below targeted return.

Meng’s argument is that the target returns aren’t achievable risk-free, so…

Closing the gap will require innovation, new skills, and a greater appetite for risk. But investors today face a unique challenge in the form of the “triple low”: a low real interest rate, low inflation, and low economic growth. These conditions imply that future returns will likely lag well behind historical norms.

Moreover, public pension funds also face a more idiosyncratic set of challenges,which I have dubbed the “triple high”: high expected returns, high current liabilities, and high underfunded gaps. These conditions are limiting pension funds’ investment flexibility at the same time that the triple low is tightening constraints on expected returns.

Yes, so perhaps one needs to adjust your expectations, not take on more asset risk.

Moreover, pensions are asset owners, as opposed to asset managers. While asset managers are under pressure to prevent their clients from abandoning them during times of market stress, public pension funds are spared from such concerns, and thus can ride out the storms.

Because asset ownership reinforces one’s ability to pursue long-term investments, private equity – with its long tie-up periods – is an ideal asset class for public pensions. But building a suitable private-equity portfolio is no small matter. Knowing which private-equity managers to pick requires deep, specialized knowledge; and getting allocations from the best managers is often difficult. Moreover, private equity is not cheap. The top managers demand high fees, and their strategies often lack the transparency of public markets.

Oh… just.

I will be reminding y’all of the actual results of these types of approaches at the end of this post.

Leveraging for Growth

Beyond investing in “better” assets, public pensions can also try to close the gap between expected and target returns with “more” assets. By using moderate borrowing (leverage), pension funds can increase the volume of total assets under management and thereby boost overall returns.

Leverage amplifies, as I said in the video. Yup, it boosts returns – it gives one a multiple of what you would get without leverage.

Which means it makes losses worse.

Meng knows this:

To be sure, leverage presents its own risks, such as duration mismatches between liabilities and the assets acquired, and unexpected increases in borrowing rates. But in a world of low inflation and gradual recovery, most major central banks have made clear their intention to keep borrowing rates lower for longer. Ultimately, leverage will always be a double-edged sword that can enhance returns but also amplify losses during market setbacks. As such, it should be used judiciously and with proper risk management provisions in place.

Judiciously. Sure.

The conclusion:

Above all, for pension plans to achieve their investment aims, they must be willing to innovate, to consider alternative assets and approaches to boosting returns, and to endure rough passages with an eye on the horizon, rather than on the obstacles immediately in front of them.

So.

One of the obstacles immediately in front of some pension funds is that they’ve got more cash going out to benefits, than coming in in contributions and investment income.

In such a case, leverage can kill very rapidly.

Leo Kolivakis responded to Meng’s remarks: CalPERS’ Former CIO on Saving America’s Public Pensions

The comment Ben wrote above is spot on, he touches on a lot of points:

The pension rate-of-return fantasy which has plagued US public pensions for over a decade. Ten years ago, I wrote a comment on what if 8% turns out to be 0% and that’s pretty much where we are now with long bond yields around the world in negative territory and zero bound.

Ben discusses how closing the gap will require innovation, new skills, and a greater appetite for risk, but with rates at record low levels and meager growth, future returns will not be anywhere near what they have been over the last 20 years.

He also discusses how lowering the discount rate (projected return assumption) isn’t easy because it would impact many stakeholders who would need to contribute more.

Moreover, he discusses liquidity management and how US public pensions are underfunded — and many are chronically underfunded with 50% or less of assets to match future liabilities — so it’s not easy to increase risk. As I’ve stated many times, pension deficits are path dependent (actually Jim Leech, OTPP’s former CEO, taught me that), so your starting point matters.

Ben’s solution is more private equity, moderate leverage and using the “intrinsic advantages” of asset owners with a long investment horizon to capitalize on opportunities across public and private markets and wait to harvest returns at the right time.

Lastly, he talks about prioritizing risk management and the need to innovate and endure difficult passages.

I added the emphasis, of course.

Meep retorts

But here are my points:

- All calls to “innovate” are, essentially, bullshit. This is one of those terms used when people don’t have anything concrete to tell you.

- Yes, it sucks to have to tell stakeholders that the promises made are a lot more expensive than originally expected so… if you want those promises fulfilled, you have to pay more. Sometimes, that is just reality. Suck it up.

- There is nothing magic about private equity. I have known various private equity players, and the ones I know that have been successful had specialized knowledge in the sector in which they employed their money. I know private equity folks in insurance – and their private equity investments are all insurance-related. They understand the business, and they understand values and opportunities. Also, they are on a particular scale.

- When you have as much money as Calpers, you’re really not going to be able to find enough successful private equity investments at the amount of money you want to allocate to the asset class. This is one of the problems institutional investors run into — at a certain point, you’re at a certain scale that you really can’t outperform the market.

Connecting GameStop shenanigans to public pensions investing

Now, private equity is not a day-trading venture, but this is about the “RISK! RISK! RISK!” thrust in public pensions investing in order to try to make up for a difficult risk-free investment landscape (i.e. interest rates are low.)

In many/most investments, when there is a catastrophic loss, it happens all at once. Different types of asset classes have different patterns of loss, especially in terms of potential total losses. For vanilla investments like public equity and bonds, the most you can lose is the money you put into your intial investment. For strategies like shorting and puts, you can theoretically lose an infinite amount of money.

Which do you think has the higher risk profile?

And does any of that sound appropriate for public pensions?

If you read the r/wallstreetbets posts, you’ll see people who are obviously acting like guys on a bender in a Las Vegas casino … “ALL MY CHIPS ON 21!!” — making bets that would give huge gains in relatively short periods, but also bets that can lead to equally huge losses. It reminds me of loads of literary figures, but it really is a type and I have learned not to lend any of these types of people money (in general, I do not lend anybody money, but you catch my drift.)

Meng is arguing that one can increase risk… but be “innovative” and “judicious”, which are words to indicate that you’re not going to be buying billboards in Times Square saying GME goes BRRRR.

Yes, I know that public pension asset managers are not going to be this crass (well, I hope not). But the history has not been that great for many public pension funds have decided it’s time to ride the high risk train.

A sampling of public pension investments gone wrong:

July 2015: Reddit-Public Pension Connection: Alternative Assets and Risk

September 2014: Public Pensions and Alternative Assets: Dallas Shows How It Can End

September 2014: Public Pensions Watch: Don’t Go Chasing Waterfalls….or Alternative Asset Classes, pt 1 of many

September 2014: Public Pensions Watch: More Reactions to Calpers Pulling Out of Hedge Funds

October 2020: A Fisking of Yet Another Public Pension “Explainer” and a Closer Look at Texas ERS

June 2020: Public Pensions, Leverage, and Private Equity: Calpers Goes Bold

That last post relates to the strategy Ben Meng had for Calpers, before he was run out of the CIO position.

Assuming you’re holding onto valuable options… that may not be there

Of course, those investing for public pensions, while trying to escape having to tell taxpayers and public employees they have to put in more money, assume they have an option in their pockets: the taxpayer put (or even the bondholder put). They think that, well, if the investment strategy loses, they can default on bonds (you can do that only once) or they can stick taxpayers with the bill (you can try that but the taxpayers may have left… or they may just say no.)

Sometimes these implicit puts are relatively small, when a pension plan is fairly well-funded and there isn’t a lot of asset risk.

But many pension funds are making big, risky bets that are hoping those puts have an equally large value.

And they may not.

Amusement: a video

Let me leave you with at least a little amusement: a sea shanty about the wallstreetbets crew.

Enjoy! I’d be eating Popeyes spicy tenders right now, if I weren’t snowed in. [and no, I’m not in on the wsb action, nor do I deal with bitcoin or any of that stuff. Just ETFs & broad index mutual funds, baybee. Living large!]

Okay, I did actually dig out, but my back hurts, and Popeyes is in Danbury. I love ya, Popeyes, but I don’t love you that much.