Defund Police Pensions: Would That Really Save a Lot of Money?

The answer is no. See, I just saved you a bunch of time.

I will be getting back to the states and cities under fiscal pressure series (and with rioting/looting, they have even more pressure).

However, I want to address the “defund police” slogan [which is very poorly defined, but that’s not my problem to untangle]. In a discussion involving that “policy”, somebody asked the question: what about the pensions?

Indeed, what about police pensions?

First, I will note that police pensions are far from the worst public pension problem by category of employee. That crown goes to teachers, mainly because there are so many more teachers than any other public employee category. I will get back to that at the end of this post.

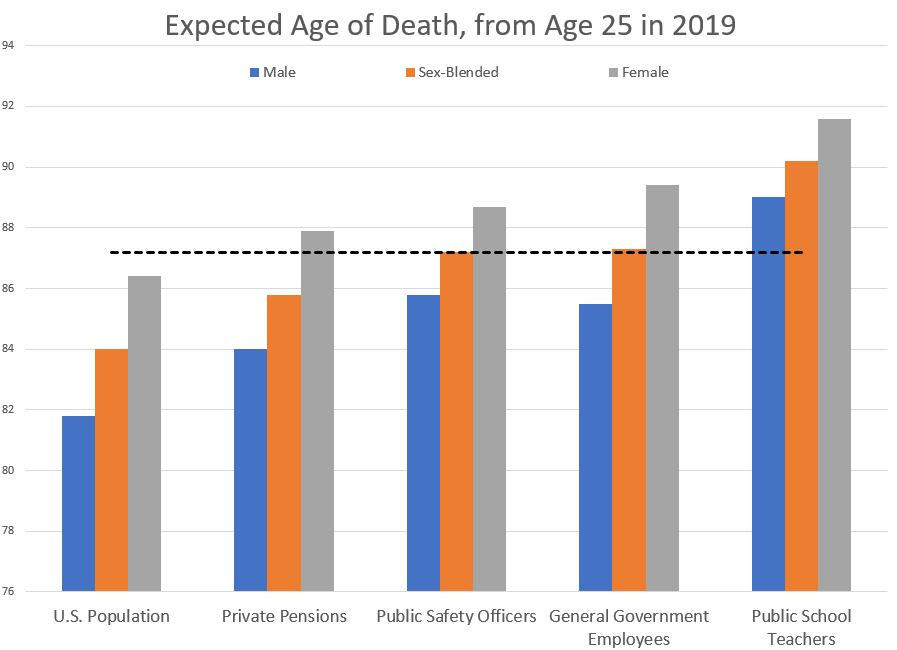

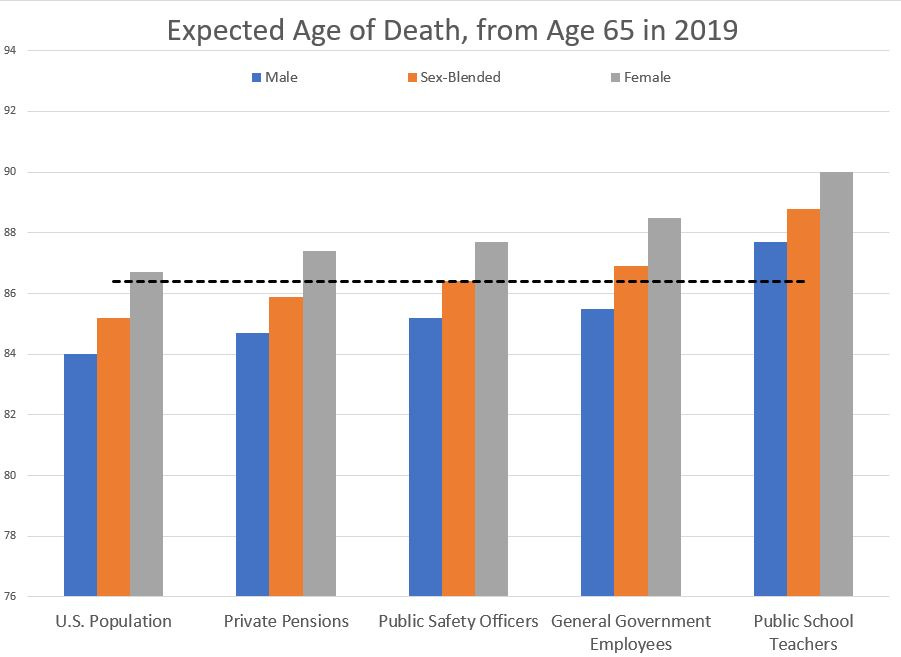

Safety officer mortality is better than general population

On a per-person basis, one would expect the police and fire pensions to be some of the most expensive: usually, their official retirement ages are a lot lower than other employee categories (given the physical demands, that’s understandable), and they really aren’t shorter-lived than the general public.

Expected age at death from age 25:

From age 65:

Heck, there’s not much difference between safety officers and general public employees in terms of longevity.

So, even holding all other items the same in the benefit formula, except the age at which you retire, safety officer (police and fire) pensions should be more expensive than other pension types.

Of course, if their pension benefit formula is sweeter other than just the retirement age (such as the years of service multiplier), then that would make them even more expensive.

Cost metrics and caveats

So let’s take a look at the stats, doing some very simple math.

I grabbed some data off of the Public Plans Database, as you do, and looked at a few cost metrics. They currently have three plan types: general employees, teachers, and safety officers. I decided to take the FY 2017 data, because these items do not change a great deal from year-to-year, and some key pension plans were missing from the FY 2018 data (forget about the FY 2019 data).

Here are the metrics I’m going to test:

Required contribution as % of payroll

Required contribution per participant [includes actives, retirees, beneficiaries, etc.]

Require contribution per active employee

I will look at the data aggregated and also as a scatterplot.

Before we begin, let’s look at the number of plans we have:

So there are a lot more general employees plans than teachers and police/fire plans. Note that some of the general employees plans may include teachers & safety officers. I’m not doing a deep dive here.

Required contribution as a % of payroll

First, aggregated [this is a weighted average, weighted by payroll]: [ARC = actuarially required contribution]

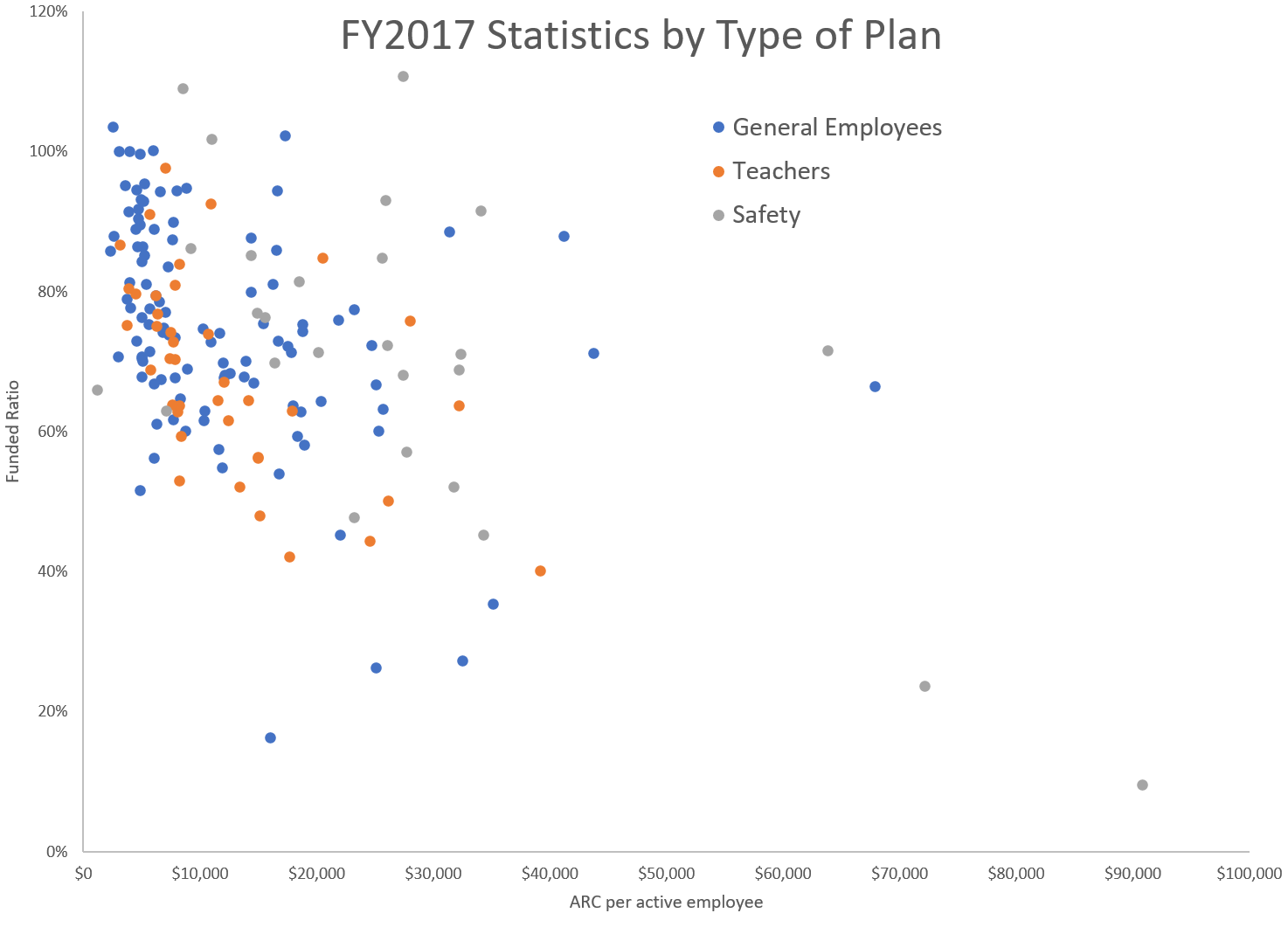

Now as a scatterplot, with the funded ratio as the other dimension:

One thing I want to point out: there is a general shape to the ARC as % of payroll — the lower the fundedness of the plan, the higher the ARC is. This is unsurprising.

Also, note that there are more grey dots “above” the mass of data: no matter how you slice it, the safety officer pensions are more expensive as % of payroll.

Required contribution per member

First, aggregated [weighted by number of plan members]:

Now as a scatterplot, with the funded ratio as the other dimension:

Remember that members include vested people no longer working for the employer, retirees, beneficiaries, and active employees.

You can see that safety pensions are more expensive.

Required contribution per active employee

First, aggregated:

Now as a scatterplot, with the funded ratio as the other dimension:

Again, we see that the less-funded the plan, the more per active member needs to be paid. Also, safety officer pensions are more costly.

The spreadsheet with the original data and plots is here at my dropbox.

Police and fire pensions are more costly than other public pensions

You don’t have to take my word for it. The pension research experts at Boston College have looked into it as well.

Issue Brief: An Introduction to Police and Fire Pensions

The brief’s key findings are:

Pension and retiree health benefits for public safety workers are more expensive than those of other local government workers, largely due to earlier retirement ages.

Perhaps surprisingly, though, their retirement benefits make up only a very small share of total local government spending.

Some evidence suggests that public safety workers could work longer, which may have implications for plans’ retirement age.

However, raising retirement ages would have little impact on government finances, particularly since it might involve higher wages to maintain a quality workforce.

It’s not really all that surprising that the cops and firefighters don’t actually cost a lot of the budget.

I will get to that in a moment. I just want to show a few figures from the full paper.

First, the normal cost of the pension benefits of safety officers versus other public employees:

The normal cost is the cost of the pensions for one year’s of work; it does not include the amortization of unfunded liabilities. The graphs I had above were the “required contributions” which is the normal cost plus the amortized cost of unfunded liabilities.

Normal cost helps get at structurally how expensive the promises are; the required contribution gets at not only that cost, but the result of deliberate underfunding.

Now, let us look at Figure 2:

Here, we’re looking at the replacement rate for full retirement at 20 years of service. The replacement rate is the percentage of your final salary that your initial pension benefit represents. Of course, many people have more than 20 years of service when they retire (even cops retiring in their 50s), but this gives you an idea of how “rich” the benefit formulas are.

So, safety officers usually retire earlier than other public employees, they live about as long in retirement as other public employees, and they have richer benefit formulas. Yes, their pensions are more expensive.

But how much of the budget is it?

Here ya go:

Two percent of state and local budgets. That’s it for police and fire pensions. [Oh, and it includes retiree health benefits, which are also richer for police and fire than other public employees].

I am not surprised because, as I keep reminding people, K-12 has orders of magnitude more employees than police and fire do.

People keep thinking that police are a huge expenditure, just from their assumptions, and never really look at the numbers.

How much does the NYPD cost NYC?

Heck, people were talking about the supposedly eye-popping amount of $6 billion for the NYPD in the NYC budget.

Do you know how big the NYC budget is?

From: April 2020 Executive Budget, Fiscal Year 2021, the budget is $89.3 billion, down from $97.4 billion for FY 2020. They were assuming a drop in revenue, even.

Looking at the full expense budget (police are 71E), I see the appropriation is actually $5.6 billion for FY2020, or $5.3 billion for the executive budget.

Either way, while the $6 billion number does look big (and was rounded up to look bigger), it’s less than 10% of the city budget. Defunding the cops is not necessarily going to give you a hell of a lot more to spend on other things.

Now, in most towns, the cops might be one of the biggest expenses, because the state takes care of all the social services, or whatever. One of the issues Illinois has with police & fire pensions was that teachers and general employees were all in state-level pension funds, and they had a bunch of itty-bitty pension funds for each town. They did a semi-consolidation of those funds, but I don’t think it’s worth much.

Police spending growing too fast?

David Sirota argues that spending on police has grown too fast:

Nationally, the numbers are stark: between 1977 and 2017, America’s population grew by about 50 percent, while state and local spending on police grew by a whopping 173 percent in inflation-adjusted dollars, according to data from the Urban Institute. In other words, the rate of police spending growth was triple the rate of population growth.

Well, more than triple.

But wait, let’s check out Sirota’s source.

From 1977 to 2017, state and local government spending on police increased from $42 billion to $115 billion (in 2017 inflation-adjusted dollars). However, as a percentage of direct general expenditures, police spending has remained consistently at just under 4 percent for the past 40 years.

Mmmm. 4% of the total direct general expenditures, eh?

Doesn’t sound to me like increased spending on cops is driving the overall government spending problem. It doesn’t sound to me like the growth is out of line, other than all government spending is out of line.

By the way, the 174% increase in real spending over 40 years? That’s a 2.55% per year real growth rate.

Remember, that’s above inflation. So. Is that growth rate too large for police spending? That’s a value judgment. But it doesn’t sound so big when I quote it like that, does it?

From the same study by the Urban Institute, would you like to guess what the spending rate increase for K-12 education was?

In 1977, state and local governments spent $289 billion on elementary and secondary education (in 2017 inflation-adjusted dollars). In 2017, they spent $660 billion.

However, between 1977 and 2017 other state and local spending (mostly Medicaid and thus public welfare) grew faster than elementary and secondary education. In 1977, 26 percent of direct general expenditures went to elementary and secondary education compared with 21 percent in 2017.

It did have lower growth than police spending — 2.08% real rate of growth per year. So while police spending tracked with other spending, K-12 education did not. But then, there are fewer kids now, as a percent of the population.

Still, K-12 education spending is about 5 times that of police. It used to be the largest category of spending, but public welfare (primarily Medicaid) expenditures have exceeded it.

Perspective on numbers

Anyway, it does one good to look at the numbers from time to time.

I have no argument as to what the numbers “should” be. I’ve read various proposals [and I have my own opinions about traffic tickets being a profit center, for example], and most aren’t explicitly trying to say “defunding the police” (whatever that means) will save money. It’s kind of there implictly, like when people throw around the $6 BILLION DOLLARS! figure for the NYPD.

It does help to know what the numbers actually are, and what they relate to, if you’re going to argue the point.

Because a lot of people are under the misimpression a lot more is spent on cops and prisons than are spent on schools, and that’s simply not true.

I know people don’t like looking at financial statements [I don’t much care for it myself], but if you’re going to argue budget, suck it up and learn the numbers. Part of the reason so many governmental entities have no issue with posting all their financials is that they know it won’t cause much of a brou-ha-ha as so few journalists can actually make anything of those documents. The journalists will take whatever press release from whomever, and take the story without being able to ask good questions of those numbers.

The type of people who read blogs like this do understand numbers, but it is tough to get the message out when it’s whoever has the loudest mouth on TV and can say the most outrageous things.

In any case, no, police aren’t usually a big part of state and local budgets [especially in big cities].

Defunding police [and police pensions] will not save a bunch of money. So don’t use that as an argument to support the idea.